- Lack of a debt ceiling strategy continues to cause considerable market uncertainty

- U.S. non-manufacturing ISM index expected to show back-to-back decline but remain strong

- U.S. trade deficit expected to remain extremely wide

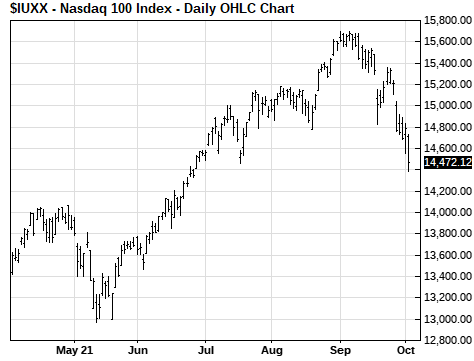

Lack of a debt ceiling strategy continues to cause considerable market uncertainty — The markets continue to be very worried about the debt ceiling since Washington politicians are engaging in some dangerous brinkmanship. There is now less than two weeks left until Treasury Secretary Yellen’s drop-dead date of October 18 for either a debt ceiling increase or suspension. The S&P 500 index on Monday closed sharply lower by -1.30% and the Nasdaq 100 index fell by -2.16%.

Democrats are trying to lay blame for the debt ceiling impasse on Republicans, who are filibustering the passage of the standalone debt ceiling suspension bill in the Senate that has already been passed by the House. Senate Minority Leader McConnell is implacably opposed to doing anything to help pass a debt ceiling increase because of his opposition to Democrat’s plans for a $3.5 trillion spending bill.

Also, Mr. McConnell is trying to force Democrats to use the reconciliation process to raise the debt ceiling, which will eat up legislative time in the Senate and will also force Democrats into a debt ceiling increase rather than a suspension, which Republicans can then use in campaign ads during the 2022 mid-term elections. The Senate parliamentarian has ruled that only a debt ceiling increase would be allowed with the reconciliation process, not a suspension.

On a more positive note, the Senate parliamentarian has ruled that Democrats can use a separate reconciliation process to raise the debt ceiling. That means that Democrats can separately proceed with their $3.5 trillion spending plan. Democrats are more likely to use reconciliation to raise the debt ceiling now that it is clear it won’t affect their ability to pass their spending bill.

The only way that Democrats could pass a debt ceiling increase or suspension without the reconciliation process would be if Senate Democrats were to vote to strip the filibuster rights from the Republicans for the debt ceiling bill. However, the White House and some moderate Democrats are opposed to any weakening of filibuster rights, making that idea a non-starter. Still, if Mr. Schumer could convince Senate moderates such as Manchin and Sinema to go along with the idea of stripping the filibuster, then Democrats would have an easy way to quickly suspend the debt ceiling.

The more likely scenario is that Democrats will have to slog through the reconciliation process, which will require at least two weeks, according to some budget experts. Even if Democrats begin reconciliation immediately, there is no guarantee it will get done by Treasury Secretary Yellen’s drop-dead date of October 18.

Yet, Senate Majority Leader Schumer on Monday again stated his opposition to using the reconciliation process to raise the debt ceiling, saying it was too time-consuming and risky. The markets are hoping that Democrats aren’t planning to try to force Republicans into dropping their filibuster by refusing to use the reconciliation process and possibly causing a stock market melt-down. Republicans don’t seem likely to succumb to that strategy. At the moment, however, the Democrats haven’t offered any other plan.

Meanwhile, the $550 billion infrastructure bill and the Democrat’s $3.5 trillion reconciliation bill are on the backburner as intra-Democratic negotiations continue. Democratic leaders are hoping to push the bills through Congress by the end of October. The stock market would like to see those bills pass since the fiscal stimulus would boost the economy, although the stock market is clearly not happy about the corporate tax hike in the reconciliation bill.

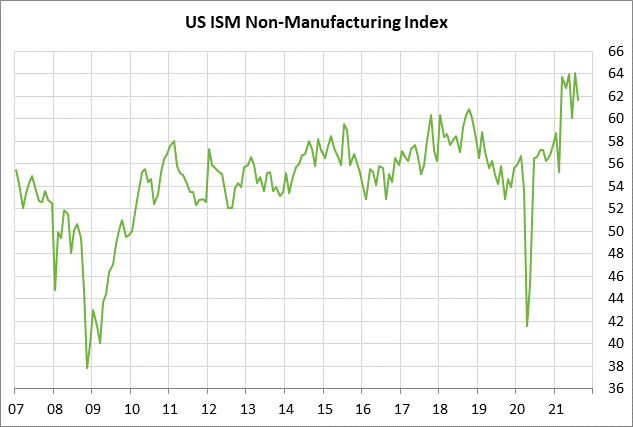

U.S. non-manufacturing ISM index expected to show back-to-back decline but remain strong — The consensus is for today’s Sep ISM non-manufacturing index to show a -1.8 point decline to 59.9, adding to Aug’s decline of -2.4 to 61.7.

If today’s report comes in as expected, that would be the first back-to-back decline in the ISM non-manufacturing index since spring 2020 when the pandemic shutdowns devastated the economy. Still, today’s expected report of 59.9 would be a strong level that shows strong confidence among business executives in the non-manufacturing sectors of the economy.

Business confidence continues to be undercut by the surge in the pandemic in August and September and by the various constraints on economic growth, including supply chain disruptions and labor market shortages. However, confidence may start to improve going into October as the Covid infection levels decline.

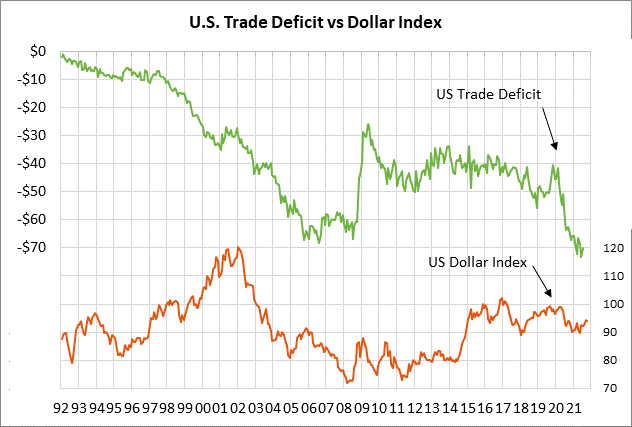

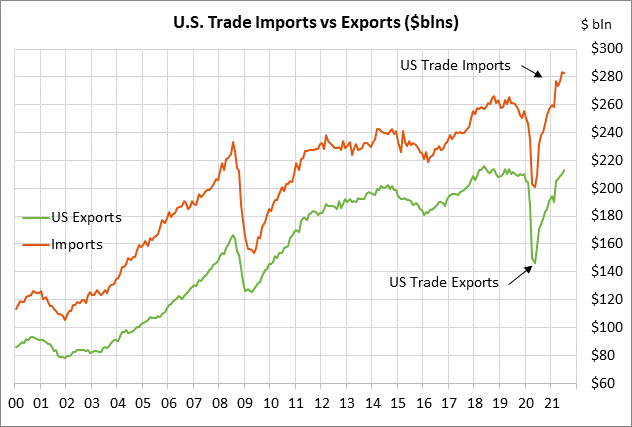

U.S. trade deficit expected to remain extremely wide — The consensus is for today’s Aug trade deficit to expand mildly to -$70.7 billion from July’s -$70.1 billion. The U.S. trade deficit remains extremely wide, just mildly below the record high of -$73.2 billion posted in June.

The wide trade deficit continues to be driven by the fact that imports are still much stronger than imports. Imports have surged over the past year due to the massive amount of U.S. government stimulus and the very strong U.S. economy. Exports, by contrast, have been weak and have barely caught up to pre-pandemic levels due to continued weak overseas economic growth.