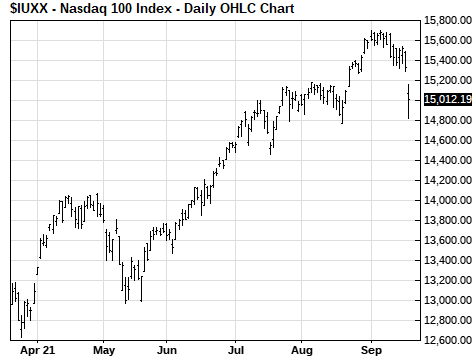

- U.S. stocks plunge on China risks, debt ceiling, and QE taperingÂ

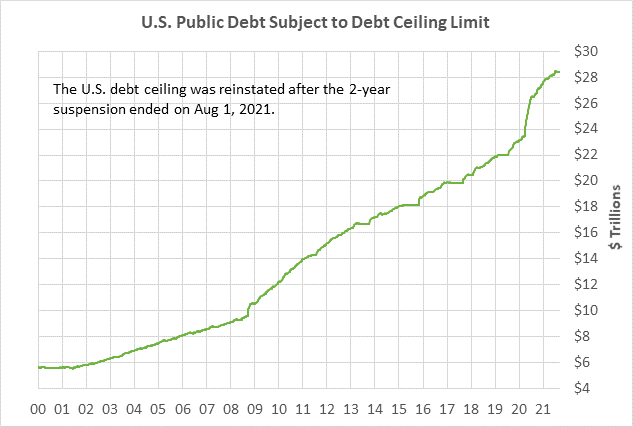

- House combines CR and debt ceiling hike for a showdown with Republicans

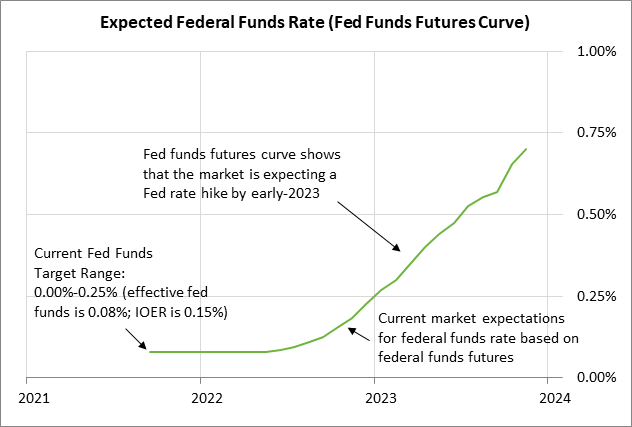

- FOMC expected to wait until November for formal QE tapering announcement

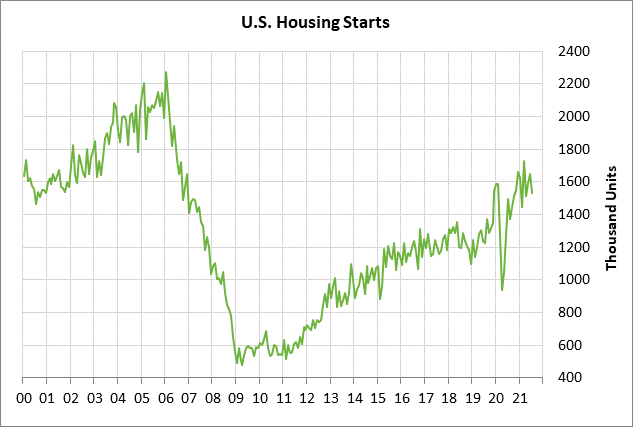

- U.S. housing starts expected to recover slightly

U.S. stocks plunge on China risks, debt ceiling, and QE tapering — U.S. stocks on Monday fell sharply on bearish factors such as (1) contagion from the Evergrande debt crisis in China and a general wave of risk-off selling, (2) concern that Washington will not act to raise the debt ceiling until there is a crisis, and (3) concern that the FOMC at its 2-day meeting that begins today will indicate that QE tapering is coming soon.

The mainland Chinese markets were closed on Monday, but the Hong Kong Hang Seng index plunged by -3.30%, led by weakness in property stocks. The markets were already worried that Evergrande, formerly China’s largest property developer, will miss interest payments on two of its bonds due this Thursday. There have been warnings that Evergrande will not be able to pay interest to banks due early this week.

Evergrande has a massive $300 billion of liabilities. So far, the Chinese government has not provided any direct support to Evergrande although the PBOC has been injecting extra liquidity into the banking system. The markets are hoping that the Chinese government, at a minimum, will help orchestrate a debt restructuring that minimizes the fall-out for the general economy, investors, and financial institutions.

Chinese and Hong Kong property developers also took a hit on Monday due to a Reuters report late Friday that Chinese officials told Hong Kong developers that the government is no longer willing to tolerate what it calls monopoly behavior. That raised concern that the property sector is next in line for the Chinese government’s regulatory crackdown.

House combines CR and debt ceiling hike for a showdown with Republicans — Democratic leaders yesterday announced that they will attach a debt ceiling hike to the continuing resolution that is necessary to keep the government running past October 1. The CR would reportedly last until December, while the debt ceiling hike (or suspension) would last until after the November 2022 mid-term elections.

Market concern about the debt ceiling increased on Monday after Treasury Secretary Yellen in a WSJ op-ed said that the Treasury would default “sometime in October” on its financial obligations without a debt ceiling hike. The Bipartisan Policy Center recently estimated that the Treasury’s X-Date would fall somewhere between mid-October and mid-November.

The combination of the CR and the debt ceiling shows that Democrats plan to force a showdown with Republicans over the debt ceiling. Democrats could raise the debt ceiling without the Republicans through the reconciliation process, sidestepping a Senate filibuster. However, Democrats believe that Republicans should help pass a debt ceiling since both parties are responsible for the massive amount of government debt incurred in recent decades.

Senate Minority Leader McConnell has said that Republicans will refuse to provide any help in passing a debt ceiling hike because they oppose the Democrat’s $3.5 trillion spending plan. There is nothing to suggest that Senate Republicans will budge an inch no matter how bad the crisis gets because Democrats have an escape hatch with reconciliation.

Indeed, there was a glimmer of hope yesterday for a peaceful resolution of the debt ceiling when House Majority Whip James Clyburn said on CNN that he “is not fine” with a Democrat-only vote to raise the debt ceiling, “But if that’s what it takes, that’s what it will take.”

That suggested that Democratic leaders may first approve a combined CR/debt ceiling hike in the House. Then, after Senate Majority Leader Schumer fails to get the 60 votes in the Senate necessary for cloture on a CR/debt ceiling hike, he will blame Republicans for their filibuster and then proceed to Plan B of passing a debt ceiling hike through reconciliation. However, that plan is very risky because there is no guarantee that the $3.5 trillion reconciliation bill will be ready before the Treasury’s X-day, or whether it will have the support of all 50 Democratic Senators necessary for it to pass. In the meantime, the markets are suffering.

FOMC expected to wait until November for formal QE tapering announcement — The consensus is that the FOMC will wait until November to formally announce QE tapering. However, the FOMC at its 2-day meeting that begins today is expected to add warning language to its post-meeting statement that constitutes the advance warning about QE tapering that the Fed has promised.

A survey of 52 economists by Bloomberg released last Friday found that two-thirds of the respondents expect the Fed to formally announce its QE tapering at its next meeting on November 2-3, with the tapering beginning in either December or January. The Fed is not expected to formally announce QE tapering as soon as this week due to (1) the weak Aug payroll report of +235,000, (2) uncertainty about the pandemic’s resurgence, (3) the possibility of a debt ceiling crisis, and (4) the possibility of major fall-out from the Evergrande debt crisis in China.

U.S. housing starts expected to recover slightly — The consensus is for today’s Aug housing starts report to rise by +1.0% m/m to 1.550 million, recovering part of July’s -7.0% drop to 1.534 million. Housing starts posted a 15-year high of 1.725 million in March but have since fallen by a total of -12.5%. New home sales are down by -29% from January’s 15-year high of 993,000 due to low inventory and high prices.