- Bipartisan infrastructure bill runs into obstacles

- FOMC’s consideration of QE tapering may be slowed by the Delta variant

- July U.S. consumer confidence expected to fade

- U.S. home prices expected to extend the surge

- 5-year T-note auction to yield near 0.72%

Bipartisan infrastructure bill runs into obstacles — The bipartisan group of Senators was unable to reach an agreement on an infrastructure bill ahead of Monday’s target. Republicans rejected a proposal from Democrats to resolve all the outstanding issues. Each party blamed the other for moving the goal posts on areas they said had already been agreed upon. The claim of bad-faith negotiations and the remaining distance between the parties did not bode well for the negotiations, although both sides appear to want an agreement.

As a result of the snag in the negotiations, Senate Majority Leader Schumer has not yet called a new cloture vote to bring the infrastructure bill to the floor. Mr. Schumer last week promised to call another cloture vote if a final agreement was reached and there are at least 10 Republicans in favor to avoid a filibuster.

The bipartisan group of Senators was scheduled to hold another meeting Monday evening to see if there is a path forward for the negotiations. The Senate is due to leave on its recess next Friday (Aug 6) and will not return until after Labor Day. Democrats need to know by next week whether there will be a bipartisan infrastructure deal. If there isn’t, then the infrastructure bill will be folded into the $3.5 trillion budget resolution, which Mr. Schumer wants to pass by next Friday before leaving for the August recess.

FOMC’s consideration of QE tapering may be slowed by the Delta variant — The FOMC at its 2-day meeting that begins today is expected to continue the QE tapering discussion that began at its last meeting on June 15-16. However, the FOMC this week is likely to continue to stress that the conditions have not yet been met for QE tapering.

The FOMC this week may even sound a bit more dovish than its June meeting since U.S. Covid infections have more than quadrupled since the June meeting. The Delta variant is a worrisome development for the Fed since there is no way to tell when the current spike in new infections may end. The Fed is not likely to proceed with QE tapering until the Delta variant has been contained and infections are back down to a relatively low level.

Prior to the Delta variant, the markets were generally expecting the Fed to give an early warning of QE tapering at either the August Jackson Hole conference or the September 21-22 FOMC meeting. However, the Delta variant may push that schedule back by at least 1-2 months, depending on the course of the pandemic.

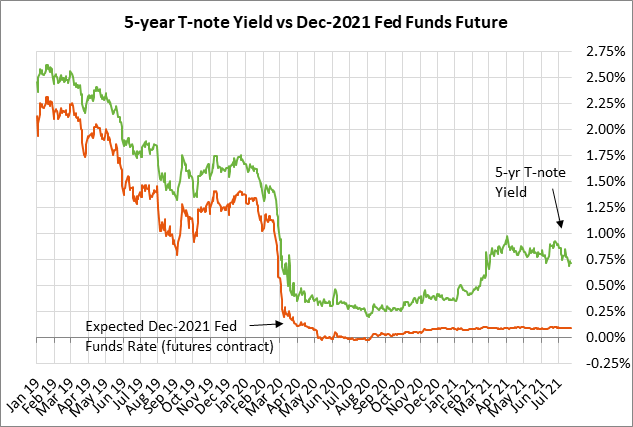

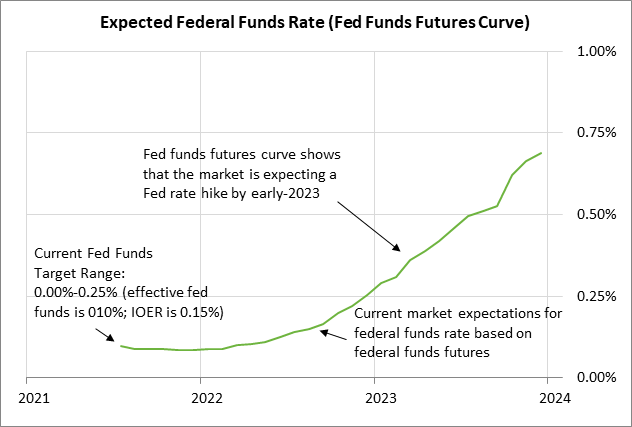

The markets in the past several weeks have significantly scaled back expectations for Fed tightening. The market is not expecting the Fed’s first +25 bp rate hike until 2023, which is about 1-1/2 years away. On a yield basis, the Dec 2023 federal funds futures contract in the past three weeks has eased by 14 bp to 0.66%, which means the market is discounting just 56 bp of tightening through the end of 2023 from the current effective federal funds rate of 0.10%.

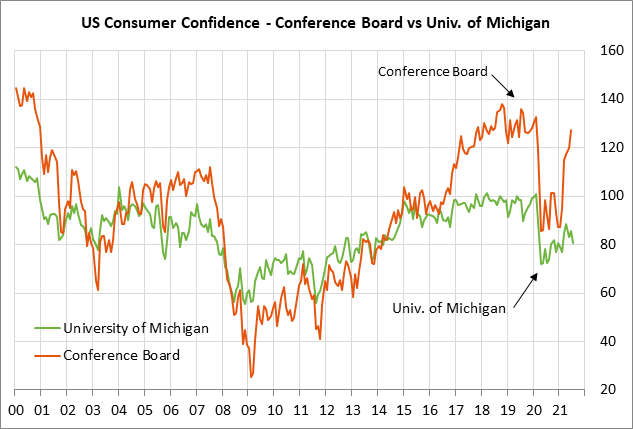

July U.S. consumer confidence expected to fade — The consensus is for today’s Conference Board U.S. July consumer confidence index to fall by -3.0 points to 124.3, reversing part of June’s +7.3 point increase to a 1-1/3 year high of 127.3. Expectations for a decline in today’s report stem in part from the already-reported news that the University of Michigan’s U.S. consumer sentiment index in early July fell by -4.7 points to 80.8.

U.S. consumer confidence is being undercut by the surge in Covid infections and concern about slower economic growth. Consumer confidence is also being undercut by sharply higher gasoline prices, which is taking a bigger bite out of household budgets.

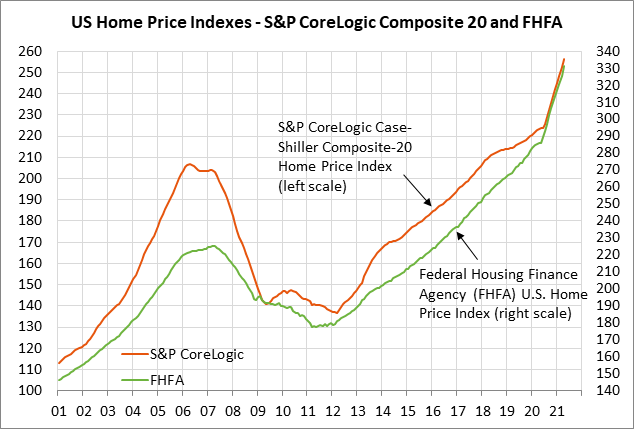

U.S. home prices expected to extend the surge — The consensus is for another huge increase in U.S. home prices in May. The May FHFA house price index is expected to show an increase of +1.6% m/m, adding to April’s increase of +1.8% m/m. Meanwhile, the May S&P CoreLogic composite-20 home price index is expected to show increases of +1.5% m/m and +16.3% y/y, which would be similar to April’s surge of +1.6% m/m and +14.9% y/y.

U.S. home prices continue to surge on the combination of strong demand and tight supplies. The FHFA index in April was +17% higher than the pre-pandemic level seen in January 2020. However, the surge in home prices at some point will cause potential homebuyers to start pulling back to wait for the housing market to stabilize as more homes come onto the market.

5-year T-note auction to yield near 0.72% — The Treasury today will sell $61 billion of 5-year T-notes. The Treasury will then sell $28 billion of 2-year floating-rate notes on Wednesday and $62 bln of 7-year T-notes on Thursday.

The 5-year T-note yield on Monday closed at 0.72%, which is only 9 bp above last week’s 5-month low of 0.63%. Treasury yields have fallen back in the past several weeks as the surge in U.S. Covid infections sparks concern about slower U.S. economic growth and reduced inflation pressures. The surge in Covid infections is also likely to force the Fed to delay its QE tapering.

The 12-auction averages for the 5-year are as follows: 2.40 bid cover ratio, $25 million in non-competitive bids, 4.8 bp tail to the median yield, 21.9 bp tail to the low yield, and 46% taken at the high yield. The 5-year is mildly below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 59.8% of the last twelve 5-year T-note auctions, which is mildly below the median of 61.2% for all recent Treasury coupon auctions.