- Pelosi-Mnuchin stimulus-bill talks continue

- Fed officials likely to maintain drumbeat for more fiscal stimulus

- U.S. JOLTS job openings expected to show slowing improvement in U.S. labor market

- U.S. trade deficit expected to expand to 12-year high in the last trade report before the electionÂ

- 3-year T-note auction to yield near 0.19%

Pelosi-Mnuchin stimulus-bill talks continue — House Speaker Pelosi and Treasury Secretary Mnuchin today will hold another phone call to discuss a stimulus bill. Pelosi-Mnuchin on Monday held a 1-hour call, although there was no word of any progress. The two sides are exchanging written proposals, which is a potentially encouraging sign.

President Trump stirred some optimism that he might be willing to raise its offer after he tweeted from his hospital room on Saturday that the U.S. “wants and needs stimulus, work together and get it done.” The House last week passed a $2.2 trillion stimulus bill, while the White House is currently at $1.6 trillion.

House members last Friday left Washington for a recess that is scheduled to last until after the November 3 election. However, House members can be called back to Washington at any time if a vote is necessary on a stimulus bill. The Senate was originally scheduled to be in session this week, but Mr. McConnell over the weekend said that Senate members will not be called back into session until Oct 19 because three Republican Senators have been diagnosed with Covid (Lee, Tillis, Johnston).

Fed officials likely to maintain drumbeat for more fiscal stimulus — Fed Chair Powell today will address the annual meeting of the National Association for Business Economics. Meanwhile, three other Fed officials (Harker, Bostic, and Kaplan) will deliver remarks today at various events.

Mr. Powell and his fellow Fed officials today will likely keep up their drumbeat for more fiscal stimulus. The speed of the economic recovery is slowing, and yet the Fed is near the limit of what it can do with monetary policy.

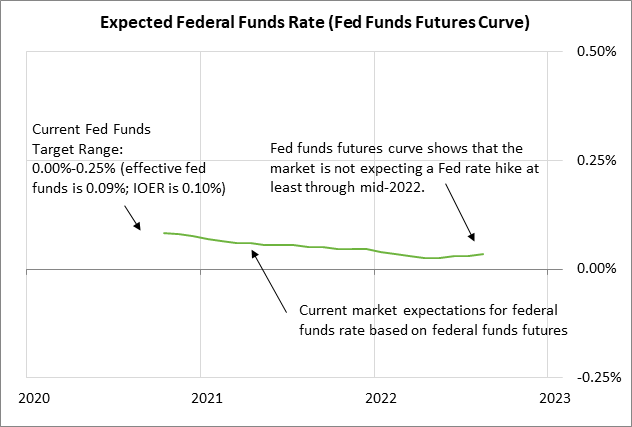

The markets are still expecting no rate hike at least through mid-2022, which is as far out as the federal funds futures contracts are trading. However, the federal funds curve has moved slightly higher by about 2 bp in the past week due to the stronger odds for VP Biden winning the presidency, which the markets believe could lead to a big increase in fiscal stimulus if Democrats also win full control of Congress.

U.S. JOLTS job openings expected to show slowing improvement in U.S. labor market — The consensus is for today’s Aug JOLTS job openings to fall by -118,000 to 6.500 million, reversing part of July’s +617,000 increase to 6.618 million. Job openings as of July recovered 80% of the plunge seen this past spring during the pandemic shutdowns. However, job openings would have to rise by another +394,000 to reach the pre-pandemic level of 7.004 million seen in February.

The markets are concerned about a slower recovery in the labor market after last Friday’s payroll report of +661,000, which was weaker than expectations of +859,000 and was the smallest increase seen since the payroll recovery began in May. Payroll jobs are still down by a net 10.7 million from the pre-pandemic record seen in February. On the brighter side, last Friday’s Sep unemployment rate fell by -0.5 points to 7.9%, which showed a stronger labor market than expectations for a -0.2 point decline to 8.2%.

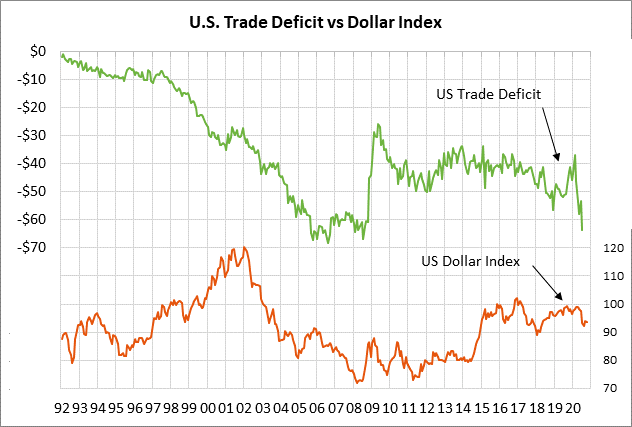

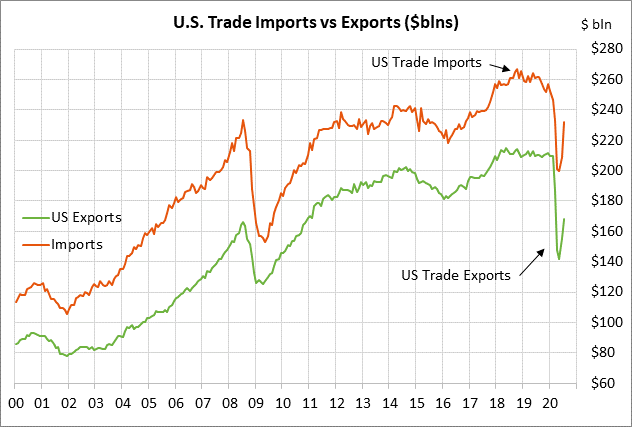

U.S. trade deficit expected to expand to 12-year high in the last trade report before the election — The consensus is for today’s Aug trade deficit to expand to -$66.2 billion from July’s -$63.6 billion, which would be a new 12-year high. The U.S. trade deficit has soared since the pandemic began, mainly because exports have fallen faster than imports. In July, exports were down -20.1% y/y versus the smaller -11.4% y/y decline in imports.

Today’s trade report will be the last before the November 3 election. Today’s expected trade deficit of -$66.2 billion would be substantially wider than the trade deficit of -$42.9 billion that Donald Trump inherited when he became President in January 2017. Slashing the trade deficit was a signature issue for Mr. Trump even though no progress has been made since the pre-pandemic deficit of -$43 billion seen in January essentially matched the deficit seen when Mr. Trump took office. The reality is that tariffs do nothing to fundamentally improve a country’s trade deficit. As taught in Economics 101, a trade deficit is usually due to a country’s need to import capital when savings fall short of investment, which is clearly the case in the United States.

3-year T-note auction to yield near 0.19% — The Treasury today will sell $52 billion of 3-year T-notes. Today’s $52 billion 3-year auction size is up by $2 billion from last month’s $50 billion size and by $14 billion (+37%) from the $38 billion size that prevailed in 2019 and early 2020 before the federal budget deficit exploded due to pandemic expenses. The Treasury will continue this week’s $110 billion coupon package by selling $35 billion of reopened 10-year T-notes on Wednesday and $23 billion of reopened 30-year T-bonds on Thursday.

Today’s 3-year T-note issue was trading at 0.19% in when-issued trading late yesterday afternoon. The 3-year T-note yield on Monday rose by +2.4 bp to 0.19% and is near the top of its recent range due to increased speculation about a Democratic sweep of Washington at the November 3 election and a big fiscal-stimulus boost for the economy.

The 12-auction averages for the 3-year are as follows: 2.44 bid cover ratio, $35 million in non-competitive bids, 3.5 bp tail to the median yield, 18.9 bp tail to the low yield, and 69% taken at the high yield. The 3-year is tied with the 2-year as the least popular coupon security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of only 51.4% of the last twelve 3-year T-note auctions, which is far below the median of 63.6% for all recent coupon auctions.