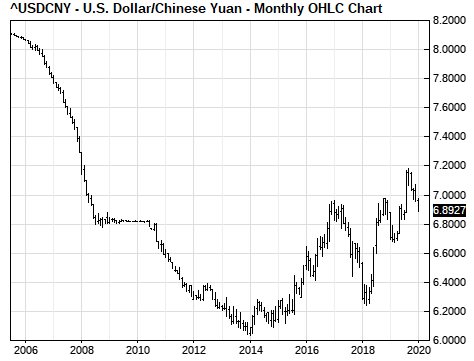

- Chinese yuan rallies to 5-1/4 month high as U.S. drops China’s “currency manipulator” label

- Chinese officials arrive in Washington for Wednesday’s trade-deal signing

- Senate’s impeachment trial likely to start next week

- Core CPI expected to remain stable

Chinese yuan rallies to 5-1/4 month high as U.S. drops China’s “currency manipulator” label — The markets on Monday were pleased by the news that the Trump administration dropped its “currency manipulator” label ahead of Wednesday’s signing of the phase-one trade deal. The phase-one trade deal includes a currency agreement, which apparently gives the Trump administration the assurances it wants that China will not engage in competitive devaluations to boost its exporters.

President Trump slapped the currency manipulator label on China last August in order to boost the trade pressure on China even though China technically did not meet the Treasury’s own definition of a currency manipulator. President Trump’s decision to now drop the currency manipulator label marks another step forward in de-escalating US/Chinese trade tensions.

The fact that the Chinese yuan on Monday rallied to a new 5-1/4 month high of 6.8884 yuan/USD was another factor suggesting that China’s currency manipulator label is no longer appropriate in any case. The yuan has now rallied by a total of +3.1% from last September’s 11-3/4 year low of 7.1073 yuan/USD.

The sharp rally in the yuan has been driven mainly by the improved prospects for the Chinese economy that emerged as the trade talks culminated in the phase-one trade deal announcement on December 13. Even though a substantial amount of the U.S. tariffs on China will remain in place, the phase-one trade deal has nevertheless sparked hopes that 2020 will be a year of relative peace on the trade front, thus allowing the Chinese economy to stabilize.

The Chinese yuan has also been boosted by the flood of global passive index capital that is flowing into the Chinese stock and bond markets as index companies such as S&P and MSCI boost the weights of Chinese stocks and bonds in their indexes.

The +3.1% rally in the Chinese yuan seen since last September is a negative factor for Chinese exporters, whose products have become more expensive and less competitive on the world markets. However, the strong yuan is a positive factor for the Chinese stock and bond markets since the stronger yuan boosts investor confidence in the Chinese markets and reduces any tendencies towards capital flight.

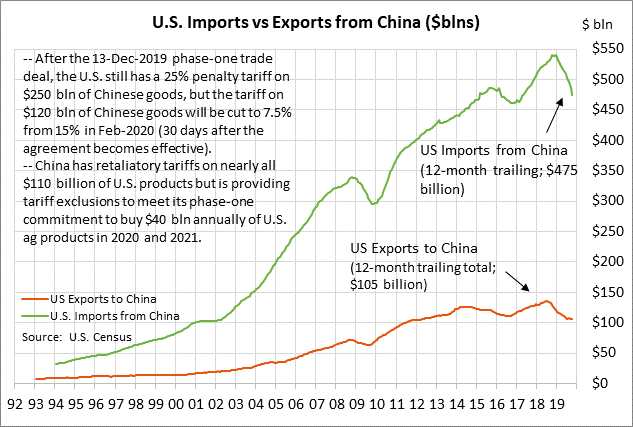

Chinese officials arrive in Washington for Wednesday’s trade-deal signing — Chinese Vice Premier Liu and other top Chinese officials arrived in Washington on Monday, according to Bloomberg. Their early arrival will give them some time today to meet with their U.S. counterparts ahead of Wednesday’s ceremony at the White House to sign the phase-one trade deal.

The markets have yet to see the full text of the 86-page agreement and it remains to be seen whether China made realistic and enforceable commitments to buy U.S. goods. Also, the markets this week will be on guard for any comments from President Trump on his approach to phase-two trade talks and whether he issues any new threats of tariffs or penalties to raise his bargaining pressure. Last week he said that phase-two talks will begin immediately but that an agreement might have to wait until after the election. That sparked market hopes that Mr. Trump will take a more relaxed approach to phase-two talks and may not raise the pressure on China in an attempt to force a phase-two trade deal before November’s election.

Senate’s impeachment trial likely to start next week — The House this week, likely on Wednesday or Thursday, is expected to vote on a resolution that formally transmits the articles of impeachment to the Senate and names the House managers who will prosecute the case in the Senate. Senator John Cornyn (R-Tx) on Monday said that he suspects the Senate trial will begin next Tuesday. That would give the Senate some time this week to handle other business. The markets in particular would like to see the USMCA agreement get as far as possible, at least getting approved by the necessary Senate committees.

The Senate’s trial of President Trump is expected to last 2-3 weeks and possibly longer depending on whether witnesses are called and whether new evidence is allowed. While the trial is going on, the Senate is not expected to conduct any other business, meaning the USMCA is likely to be put on the back burner until at least February.

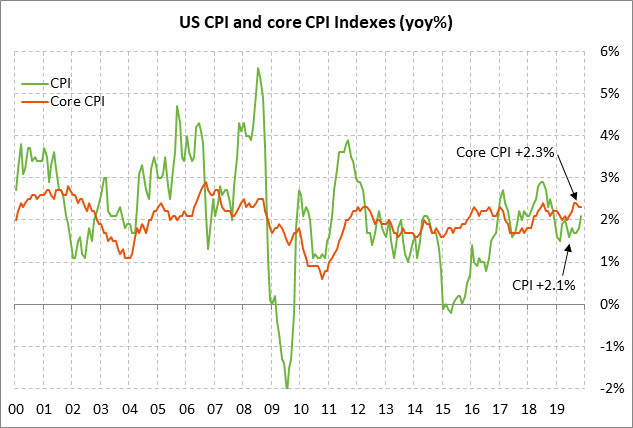

Core CPI expected to remain stable — The consensus is for today’s Dec CPI to rise to +2.4% y/y from Nov’s +2.1%, but for the Dec core CPI to be unchanged from Nov’s +2.3% y/y. The rise in the headline CPI is expected to be driven by the +10.7% rally seen in crude oil prices in December that was sparked by the unexpected move by OPEC+ to cut its production by 1.7 million bpd in Q1-2020, up from the 2019 production cut of 1.2 million bpd. However, the core CPI today is expected to be unchanged at +2.3% y/y, illustrating little change in the outlook for core inflation.

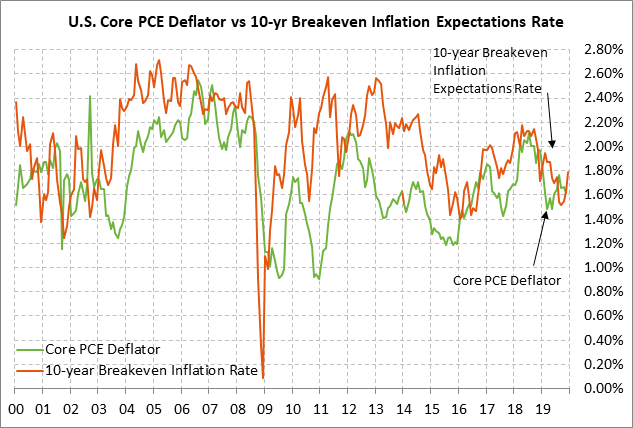

Market expectations for inflation have risen in the past several months and the 10-year breakeven inflation expectations rate is currently at 1.78%. The current breakeven rate of 1.78% is up sharply from Oct’s 3-1/4 year low of 1.47% but is still well below the Fed’s +2.0% inflation target. Moreover, the Nov core PCE deflator (the Fed’s preferred inflation measure) remained low at +1.6% y/y in November, illustrating that there is no pressure on the Fed at present to raise interest rates based on the inflation outlook.