- Schumer says Senate won’t pass a pandemic aid bill until mid-March

- Powell expected to downplay QE tapering

- U.S. consumer confidence is in dismal shape

- U.S. home prices expected to show another strong increase

- 5-year T-note auction to yield near 0.40%

Schumer says Senate won’t pass a pandemic aid bill until mid-March — The U.S. stock market weakened on Monday after Senate Majority Leader Schumer said he expects to get a pandemic aid bill passed by mid-March. The markets had been hoping for quicker action.

There has already been significant Republican resistance to President Biden’s $1.9 trillion pandemic aid bill. President Biden is trying for a bipartisan pandemic aid bill, but the chances are growing that Democrats will have to use the more complicated and time-consuming budget reconciliation process to pass the aid bill, which would by-pass a Republican filibuster.

The Senate currently has its hands full confirming cabinet officials and trying to pass an organizing resolution so that committees can be revamped. Mr. Trump’s trial is then due to begin in the week of February 8. By early or mid-February, the House may have passed a pandemic aid bill, forwarding it to the Senate for its consideration later in February after the Trump trial is over. The Trump trial is not expected to take more than 2-3 weeks. The betting odds at PredictIt.org, for whatever they are worth, are at only 13% that Mr. Trump will be convicted within the first 100 days of President Biden’s term.

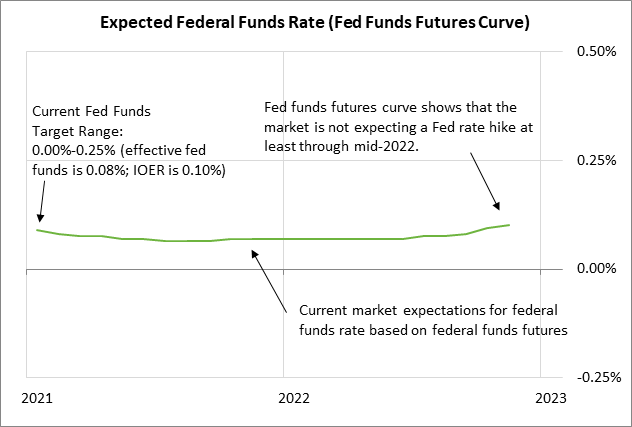

Powell expected to downplay QE tapering — The market is unanimously expecting the FOMC at its 2-day meeting that begins today to leave its main policy variables unchanged with the funds rate target at 0.00/0.25% and the QE program at $120 billion per month. The FOMC at this meeting will not update its macroeconomic forecasts or its forecast for the funds rate target.

This main issue for this week’s meeting will be the extent to which Fed Chair Powell, in his post-meeting press conference, tries to dampen market speculation about QE tapering. Several Fed officials earlier this month started talking about the timing of QE tapering, which sent T-note yields substantially higher. However, other Fed officials and Mr. Powell himself then stepped in to try to douse the QE tapering talk.

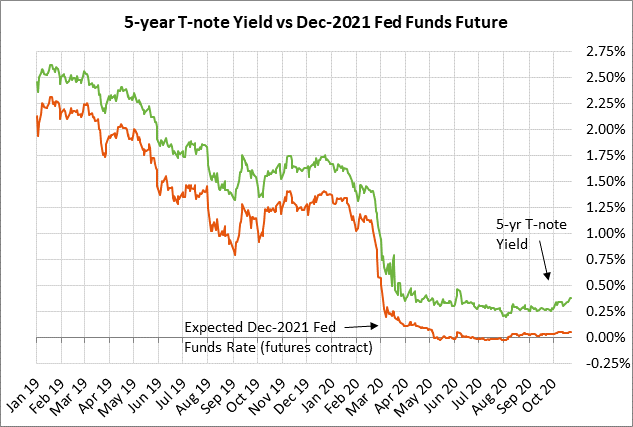

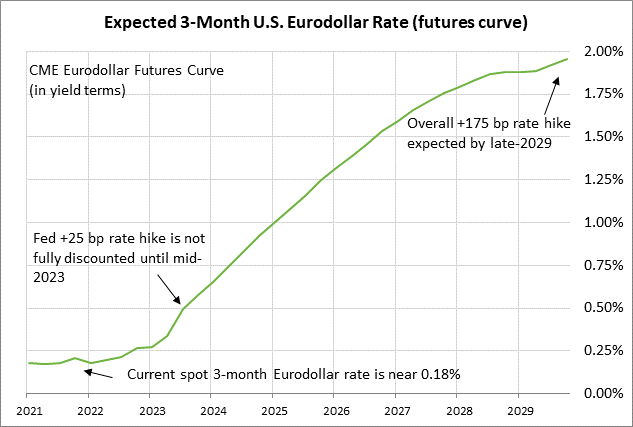

The market is expecting the Fed to leave its funds rate target unchanged at least through late-2022, according to the federal funds futures market. According to the Eurodollar futures market, which trades farther out into the future than fed funds futures, the market is expecting the Fed’s first +25 bp rate hike by mid-2023 and is expecting an overall +175 bp rate hike to almost 2.00% by late 2029.

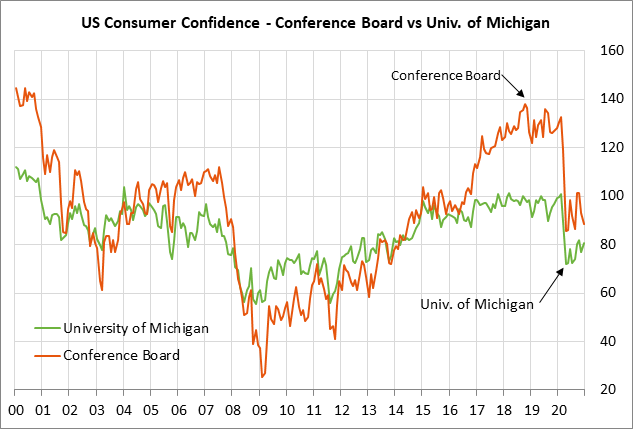

U.S. consumer confidence is in dismal shape — The consensus is for today’s Jan Conference Board U.S. consumer confidence index to show a small +0.4 point increase to 89.0, recovering a small part of December’s -4.3 point decline to 88.6.

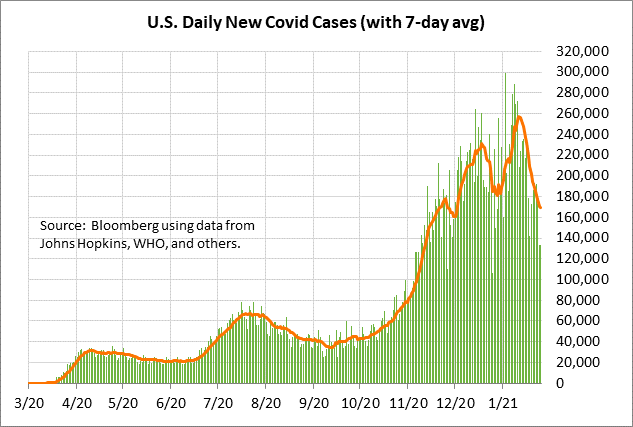

The consumer confidence index remains in dismal shape at only 2.9 points above April’s 6-1/2 year low. The recent surge in the pandemic has hurt U.S. consumer confidence due to the renewed lockdowns and weakness in the U.S. labor market. The only good news is that the 7-day average of daily new U.S. Covid cases has fallen to a 7-week low of 169,000, which has raised hopes that the pandemic peak has perhaps passed.

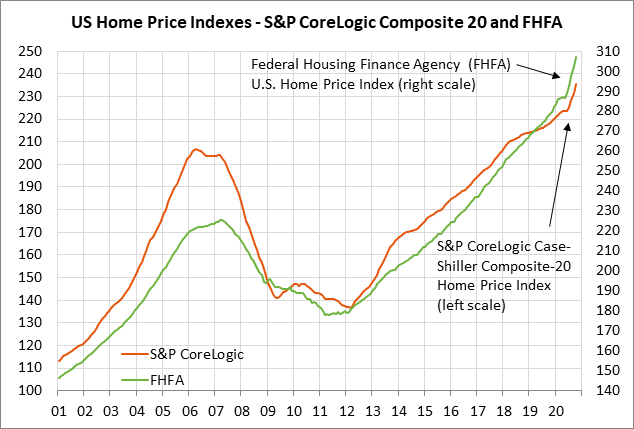

U.S. home prices expected to show another strong increase — The consensus is for today’s U.S. home price reports to show sharp increases, reflecting the strong demand for homes combined with the very tight supply. U.S. home sales are currently just mildly below October’s 15-year high of 6.86 million units. Meanwhile, the supply of existing homes available for sale hit a record low of 1.8 months in December, which is far below the 4-decade average of 6.3 months.

The consensus is for today’s Nov FHFA house price index to show a strong +0.8% m/m increase, adding to October’s +1.5% increase. Today’s Nov S&P CoreLogic composite-20 home price index is expected to show increases of +1.0% m/m and +8.7% y/y, following October’s report of +1.6% m/m and +8.0% y/y.

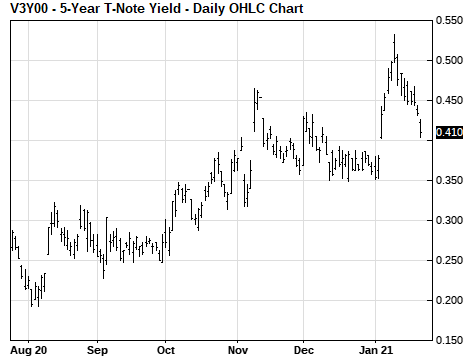

5-year T-note auction to yield near 0.40% — The Treasury today will sell $61 billion of 5-year T-notes. The size of today’s 5-year T-note auction is up by $2 billion from December’s $59 billion auction and by $20 billion from the $41 billion size that prevailed in 2019 before pandemic expenses sent the U.S. budget deficit soaring in 2020.

The Treasury will then continue this week’s $211 billion T-note package by selling $28 billion of 2-year floating-rate notes on Wednesday and $62 billion of 7-year T-notes on Thursday.

The benchmark 5-year T-note yield on Monday fell sharply by -3 bp to a new 3-week low of 0.40%. The 5-year T-note yield as recently as mid-January rose to a 10-month high of 0.53% due to the talk of QE tapering but has since fallen back after Fed Chair Powell and other Fed officials tried to douse the QE tapering talk. T-note yields have also fallen back as the global pandemic surge continues and dampens the global economy.

The 12-auction averages for the 5-year are as follows: 2.47 bid cover ratio, $19 million in non-competitive bids, 4.6 bp tail to the median yield, 31.4 bp tail to the low yield, and 61% taken at the high yield. The 5-year is the third least popular security among foreign investors and central banks behind the 2-year and 3-year T-notes. Indirect bidders, a proxy for foreign buyers, have taken an average of only 59.6% of the last twelve 5-year T-note auctions, which is well below the median of 63.1% for all recent Treasury coupon auctions.