House passes budget resolution but creates legislative deluge for late September

U.S. durable goods orders expected to weaken

5-year T-note auction to yield near 0.80%

House passes budget resolution but creates legislative deluge for late September — The House yesterday approved the $3.5 trillion budget resolution. That means the various Congressional committees now have the instructions to write the final legislation for the reconciliation bill that will be considered by the House and Senate this fall.

In order to get the nine-member group of moderate Democratic House members to approve the budget resolution, House Speaker Pelosi had to promise that the House will vote on the $550 billion infrastructure bill by September 27. Ms. Pelosi also had to promise that the House leadership would work closely with moderate Democratic Senators such as Manchin and Sinema to produce a reconciliation bill that can actually pass the Senate. Moderate Democratic House members do not want to be stuck taking a politically tough vote on a budget reconciliation bill that has no chance of passing the Senate.

After voting yesterday, the House resumed its recess and will not return to full session until September 20. Only a week after returning to Washington, the House will then have to vote on the $550 billion infrastructure bill. If the House approves the Senate’s infrastructure bill without any changes, then it will go to President Biden for his signature. However, if the House makes any changes to the infrastructure bill, which seems likely, then it will have to go back to the Senate for a new vote or to a House-Senate conference committee to iron out a compromise version.

Ms. Pelosi’s promise of a vote on the infrastructure bill by September 27 could upend her strategy of holding the infrastructure bill hostage until Senate Democrats pass the $3.5 trillion reconciliation bill, which might not come until November or December. However, Ms. Pelosi is highly experienced in getting bills through Congress, and she likely has a new plan for keeping intense pressure on Senate Democrats to pass the reconciliation bill.

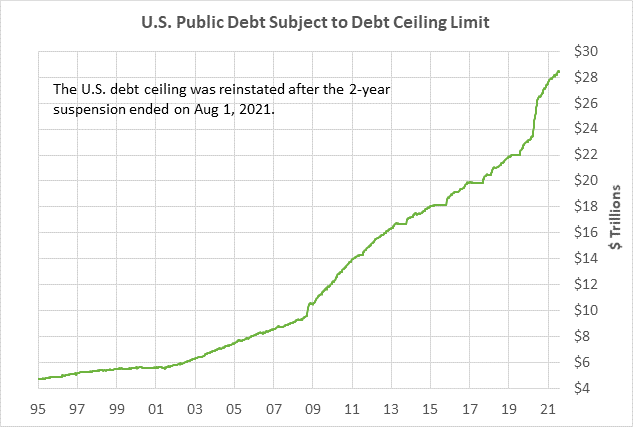

In addition to the September 27 infrastructure vote, Ms. Pelosi must get a continuing spending resolution for the new fiscal year approved by September 30 or there will be a partial government shutdown on October 1.

Also, Democratic Congressional leaders may add a debt ceiling hike to the continuing resolution to try to force Republicans to allow both bills to pass. Democrats have no real leverage to get a debt ceiling hike past a Senate Republican filibuster except to meet Republican demands for concessions, or set up the threat of a dual crisis with the threat of a government shutdown and a Treasury default.

The stock market in recent weeks has not shown much reaction to the Congressional deliberations over the infrastructure bill and the budget resolution. However, the markets may become more sensitive once Congress gets down to brass tacks on those bills this autumn.

The markets will also be paying close attention to whether there will be another federal government shutdown on October 1 and whether there will be the threat of a Treasury default when the Treasury runs out of cash in October or November.

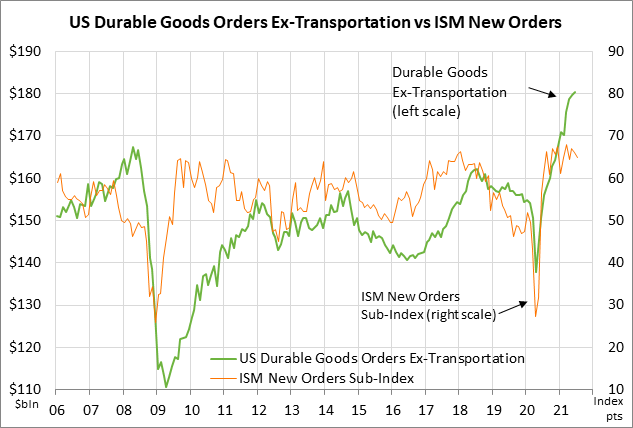

U.S. durable goods orders expected to weaken — The consensus is for today’s July durable goods orders report to weaken a bit as businesses take a more cautious outlook due to the deceleration of the U.S. economy and the pandemic’s resurgence.

Today’s July durable goods orders report is expected at -0.3% m/m and +0.5% m/m ex-transportation versus June’s report of +0.9% m/m and +0.5% m/m ex-transportation. However, capital spending is expected to remain positive, with today’s July core capital goods new orders report (i.e., ex defense and aircraft) expected to show an increase of 0.5% m/m after June’s report of +0.7%.

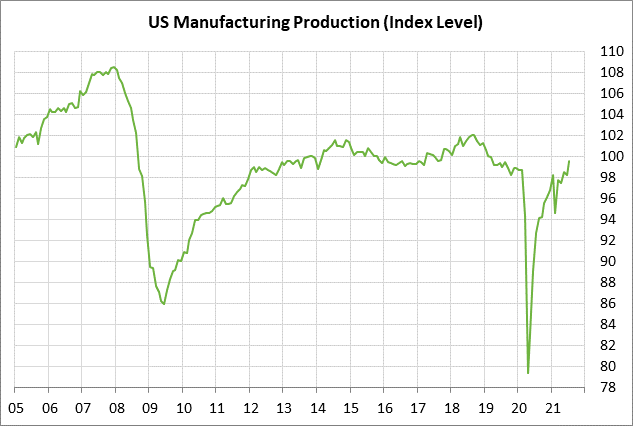

U.S. manufacturing confidence remains strong, although down from the euphoric levels seen earlier this year when vaccinations first became available and the pandemic infection levels dropped sharply. The latest ISM manufacturing index reading was strong at 59.5 in July, although that was down from the 37-year high of 64.7 posted earlier this year in March.

U.S. manufacturing executives remain generally optimistic about the outlook, despite near-term problems such as the pandemic resurgence, the chip shortage, supply chain disruptions, shipping problems, and a labor shortage in some sectors.

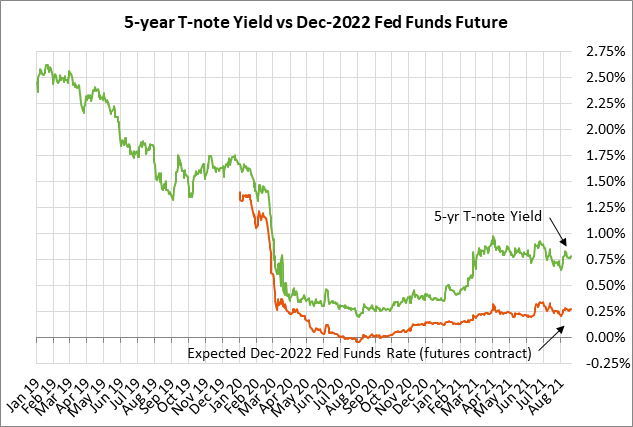

5-year T-note auction to yield near 0.80% — The Treasury today will sell $26 billion of floating-rate notes and $61 billion of 5-year T-notes. The Treasury will then conclude this week’s $209 billion T-note package by selling $62 billion of 7-year T-notes on Thursday.

The benchmark 5-year T-note yield yesterday closed at 0.80%, which is near the middle of range seen since March. The 5-year T-note yield remains far below the pre-pandemic level of 1.75% since the Fed is not expected to begin raising interest rates until early 2023.

The 12-auction averages for the 5-year are as follows: 2.40 bid cover ratio, $25 million in non-competitive bids, 4.8 bp tail to the median yield, 21.7 bp tail to the low yield, and 46% taken at the high yield. The 5-year T-note is the fourth-least popular security among foreign investors and central banks behind the 3-year, 2-year, and 7-year. Indirect bidders, a proxy for foreign buyers, have taken an average of 59.8% of the last twelve 5-year T-note auctions, which is mildly below the median of 62.2% for all recent Treasury coupon auctions.