- Weekly market focus

- Weekend Chinese news is mildly negative

- Fed rate hike expectations turn more hawkish

Weekly market focus — The markets this week will focus on (1) the Tue/Wed FOMC meeting where the Fed is expected to leave interest rates unchanged but where Fed Chair Yellen in her post-meeting press conference may provide some useful insights into the Fed’s policy bias looking forward, (2) central bank meetings this week in Japan and the UK, which are not expected to produce any policy changes, (3) oil prices, which posted a 2-1/2 month high last Friday but where oil producers are having trouble organizing a meeting about even freezing production, (4) U.S. politics as five states on Tuesday head to the polls to vote in the presidential primaries, and (5) this week’s heavy U.S. economic schedule.

This week’s heavy U.S. economic schedule is expected to be biased to the stronger side. Strong reports this week are expected to include: (1) Tuesday’s March Empire manufacturing index (expected +5.14 to -11.50), (2) Tuesday’s March NAHB housing market index (expected +1 to 59), (3) Wednesday’s Feb housing starts report (expected +4.6% after Jan’s -3.8%), (4) Thursday’s March Philadelphia Fed business outlook index (expected +1.1 to -1.7), (5) Thursday’s Feb leading indicators report (expected +0.2% after Jan’s -0.2%), and (6) Friday’s University of Michigan preliminary-March U.S. consumer sentiment index (expected +0.5 after Feb’s -0.3%).

Weak reports this week are expected to include: (1) Tuesday’s Feb retail sales report (expected -0.1% and -0.2% ex-autos), (2) Wednesday’s Feb industrial production report (expected -0.3% after Jan’s +0.9%), and (3) Thursday’s Jan JOLTS job openings report (expected -57,000 after Dec’s +261,000).

This week’s U.S. inflation data is expected to be mixed. Tuesday’s Feb PPI report is expected to increase to +0.1% y/y from -0.2% in Jan and the Feb core PPI is expected to increase to +1.2% y/y from +0.6% in Jan. Meanwhile, the Wednesday’s Feb CPI is expected to fall to +0.9% y/y from Jan’s +1.4% while the core CPI is expected to be unchanged from Jan at +2.2% y/y.

The Treasury on Thursday will sell $11 billion of 10-year TIPS. There are only five of the S&P 500 companies that report earnings this week: Oracle on Tuesday, FedEx on Wednesday, Adobe on Thursday, and Tiffany and Cintas on Friday. The market consensus is that Q1 SPX earnings growth will show a decline of -6.5% y/y, which would be the third consecutive month of negative earnings growth, according to Thomson Reuters I/B/E/S. The market is then expecting a fourth consecutive month of SPX earnings growth in Q2 with a decline of -1.7%. The market is then expecting SPX growth to return to positive territory in Q3 with a +5.2% rise and improve to +10.7% in Q4.

Weekend Chinese news is mildly negative — The markets come into this week on a somewhat weak note after mildly bearish news out of China over the weekend. Chinese central bank Governor Xhou Xiaochuan said on Saturday that “excessive” stimulus would not be necessary to achieve the government’s GDP target of +6.5% over the next five years, suggesting that the PBOC is not leaning toward any new stimulus measures at this point. The Chinese stock market has been more stable in the past 6 weeks, consolidating after the sharp sell-off seen in January. In addition, the Chinese yuan has been strengthening in the past month and edged to a new 2-1/2 month high last Friday, helping to keep the Chinese stock market stable.

The Chinese economic data released over the weekend was mildly weaker than expected. Friday’s Feb new yuan loan report showed an increase of +727 billion yuan, weaker than expectations of +1.2 billion yuan and far below Jan’s surge of +2.5 billion yuan. Saturday’s Jan-Feb industrial production report of +5.4% y/y was weaker than expectations of +5.6% and was down from Dec’s report of +6.1%. Saturday’s Jan-Feb retail sales report of +10.2% y/y was below expectations of +11.0% and was down from Dec’s report of +10.7%.

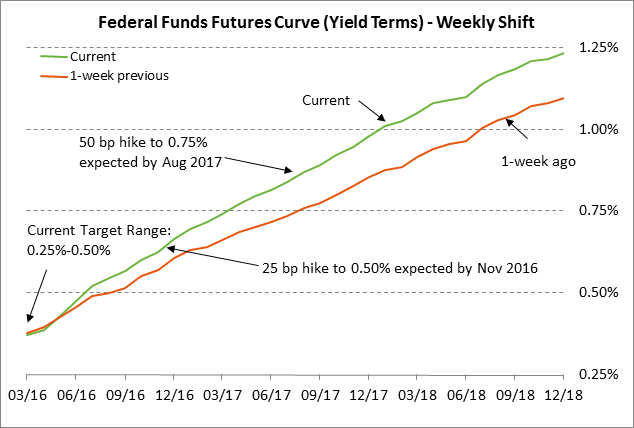

Fed rate hike expectations turn more hawkish — Market expectations for the timing of the Fed’s next rate hike have turned substantially more hawkish in the past several weeks mainly because of the more stable situation in China and the upward rebound in crude oil prices and the U.S. stock market. Just in the past week, the federal funds futures curve has tightened up by +6 bp for the end of 2016, +10 bp for the end of 2017, and +14 bp for the end of 2018. The markets are now fully discounting the Fed’s next 25 bp rate hike by November 2016 and the following 25 bp rate hike by August 2017.

The markets are discounting only a 4% chance for a Fed rate hike this week. The markets have settled down after the turbulence seen in January and February but the Fed will want to make sure that the U.S. economy is not stumbling before it implements its next rate hike, particularly since the U.S. economy came into 2016 on a weak note with GDP growth in Q4-2015 of only +1.0%. The FOMC at its 2-day meeting this week on Tue/Wed will release updated macroeconomic forecasts and Fed Chair Yellen will hold a press conference following the meeting.

While the chances are close to zero for a rate hike this week, the chances for a rate hike thereafter rise fairly quickly as the year wears on. The market is discounting the chances for a +25 bp rate hike at +22% by the April FOMC meeting, 58% by the June meeting, 68% by the July meeting, 90% by the Sep meeting, and 100% by the Nov meeting.