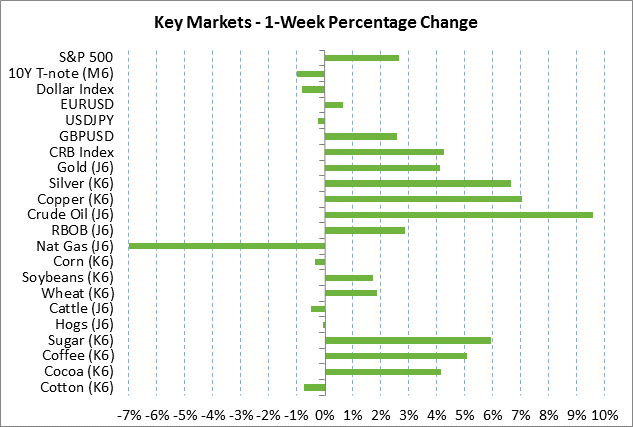

- Weekly market focus

- Strong U.S. payroll report accelerates expectations for Fed’s next rate hike

- China’s policy is under scrutiny as the 2-week Congress meeting begins

- U.S. consumer credit expected to remain generally strong

Weekly market focus — The markets this week will focus on (1) whether crude oil prices can extend their 3-week recovery to last Friday’s 2-month high, (2) whether the Chinese stock market and the yuan can hold their ground amidst the 2-week Chinese National People’s Congress meeting, which started this past weekend, (3) whether the 3-week recovery in the U.S. stock market can continue, (4) expectations that the ECB at its meeting this Thursday will cut its deposit rate by another -10 bp to -0.40% and possibly announce an expanded QE program, (5) the U.S. Treasury’s sale this week of $56 billion of 3-year, 10-year and 30-year securities, (6) comments today by Fed Vice Chair Fischer and Fed Governor Brainard, and (7) this week’s light U.S. economic schedule that includes today’s Jan consumer credit report (expected $16.5 billion) and Friday’s Feb import price index (expected -0.8% m/m and -6.6% y/y).

Strong U.S. payroll report accelerates expectations for Fed’s next rate hike — Last Friday’s U.S. Feb payroll report of +242,000 was substantially stronger than expectations of +195,000 and, in addition, Jan was revised upwards to +172,000 from +151,000. That led to a solid Jan-Feb average of +207,000. The report dampened the recent talk of a U.S. recession. As long as payroll growth is strong and consumers are confident about their job safety, then U.S. consumer confidence and spending should be able to continue to support the economy. Feb average hourly wages dipped to +2.2% y/y from +2.5% in Jan, which was a bit disappointing. However, there is room for an improvement in wages as the year wears on if the labor market remains tight with the unemployment rate near the 8-year low of 4.9% posted in Jan-Feb.

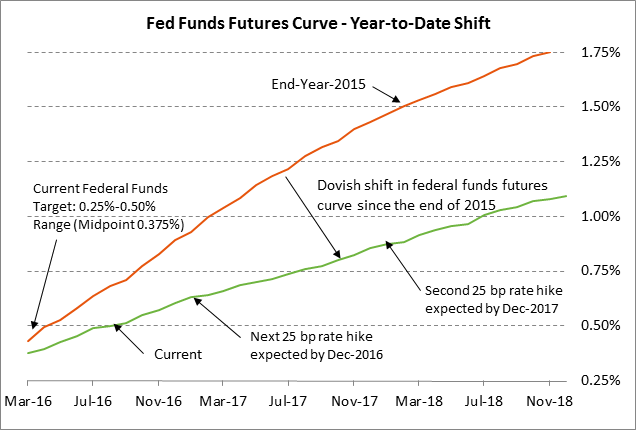

Friday’s strong payroll report caused the federal funds futures curve to tighten by +3 bp for the Dec 2016 contract, +6 bp for the Dec 2017 contract, and +7 bp for the Dec 2018 contract. The federal funds futures market is now fully discounting the Fed’s next rate hike by late this year in December. The market is discounting the chances for a Fed rate hike at 8% for next week’s FOMC meeting, 20% for the April meeting, 46% for the June meeting, +50% for the July meeting, 70% for the Sep meeting, 78% for the Nov meeting, and 100% for the Dec meeting. The FOMC at its meeting next week will update its forecasts for the economy and for the federal funds rate. In addition, Fed Chair Yellen will hold a press conference next week.

China’s policy is under scrutiny as the 2-week Congress meeting begins — The Chinese markets come into this week on a little stronger footing since the Chinese yuan last Thursday/Friday rallied by a combined +0.7%. That provided support for the Shanghai Composite stock index, which rallied by +3.9% last week.

The Chinese markets last week expected the Chinese government to announce some positive measures this week in conjunction with the 2-week National People’s Congress that began this past weekend. The Congress is the annual gathering of China’s legislature to consider near-term policies as well as the 5-year plan. The markets are looking ahead to comments scheduled for this coming Saturday (March 12) by PBOC Governor Zhou Xiaochuan, in which he will perhaps better explain the country’s currency policy and provide some indications about whether the PROC has any flexibility to further reduce interest rates.

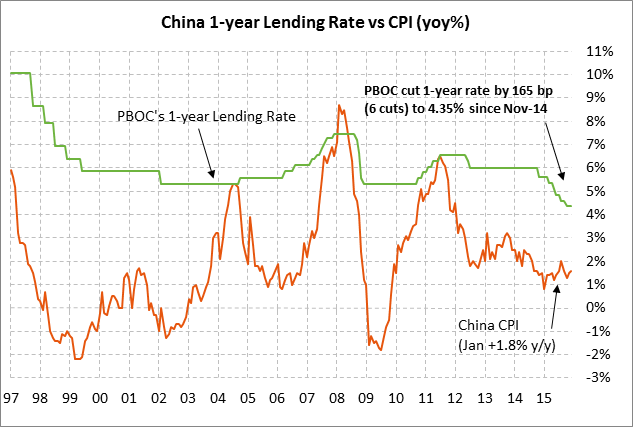

The Chinese government on Saturday released some key targets that were in line with market expectations: (1) GDP growth of 6.5-7.0% for 2016, down from last year’s target of +7.0%, (2) CPI growth of about 3%, (3) the creation of at least 10 million urban jobs, (4) a rise in the government budget deficit to a record 3.0% of GDP from +2.4% in 2015 as a fiscal stimulus measure, (5) M2 growth of 13%, a bit higher than last year’s target of +12%, and (6) the use of “a full range of monetary policy tools.” The reference to monetary policy tools refers to further cuts in the bank reserve requirement ratio (RRR) and the PBOC’s benchmark 1-year lending rate.

The PBOC has room on the downside to further cut its 1-year lending rate since the current level of 4.35% is well above the Jan CPI rate of +1.8%. The PBOC has already cut the 1-year lending rate by 165 bp to the current level of 4.35% from the 6.00% level seen in late 2014, with the last 25 bp rate cut occurring in Oct 2015. The PBOC last week cut its reserve requirement ratio (RRR) by 50 bp to 17.0%, bringing the overall cut since late 2014 to 300 bp. The PBOC last week cut its RRR ratio to free up another $100 billion of bank lending, avoiding another interest rate cut that could have sparked new weakness in the yuan ahead of the National Congress.

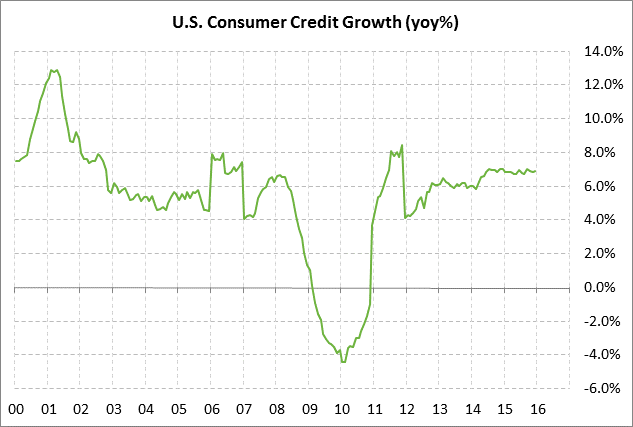

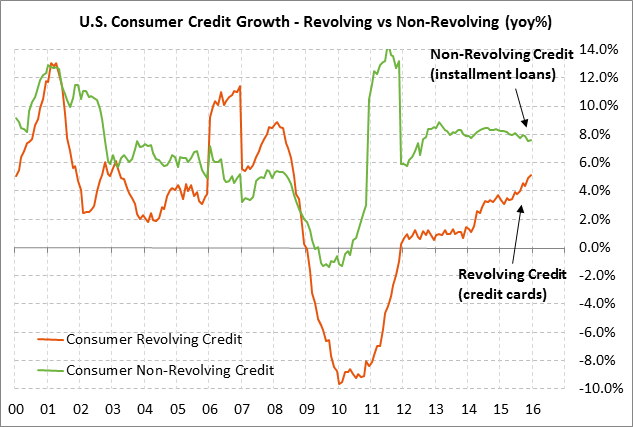

U.S. consumer credit expected to remain generally strong — The market is expecting today’s Jan consumer credit report to show an increase of +$16.5 billion, falling back from the +$21.267 billion surge seen in December. Today’s expected report of +$16.5 billion would be mildly below the 12-month average of +19.1 billion. U.S. consumer credit growth in December remained strong at +6.9% y/y, just below the recent 4-year high of +7.0%.

The strength in consumer credit continues to be driven mainly by student and auto loans as seen by the fact that installment loans showed a strong increase of +7.6% y/y in December. However, credit card growth has been rising over the last year and revolving credit in December reached a 7-1/2 year high of +5.1% y/y. That suggests that consumers are feeling confident enough about their household finances to boost their credit card usage, although it also means that some consumers are perhaps getting themselves over-extended again on debt.

The strength in consumer credit continues to be driven mainly by student and auto loans as seen by the fact that installment loans showed a strong increase of +7.6% y/y in December. However, credit card growth has been rising over the last year and revolving credit in December reached a 7-1/2 year high of +5.1% y/y. That suggests that consumers are feeling confident enough about their household finances to boost their credit card usage, although it also means that some consumers are perhaps getting themselves over-extended again on debt.