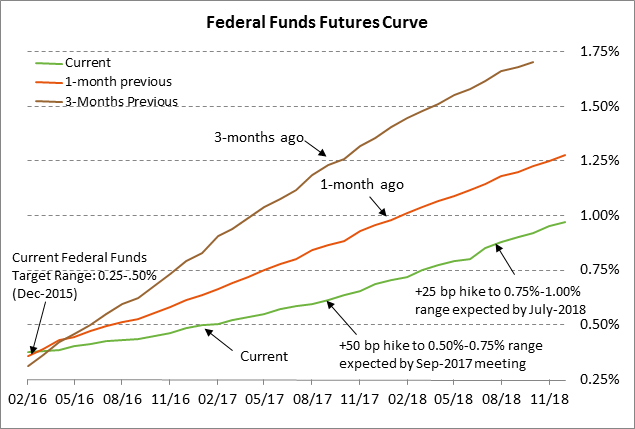

- FOMC minutes support deferred Fed rate hike expectations

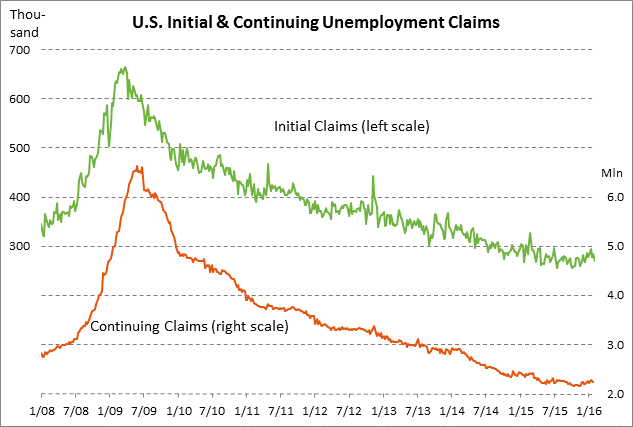

- Unemployment claims are within shooting distance of decade-plus lows

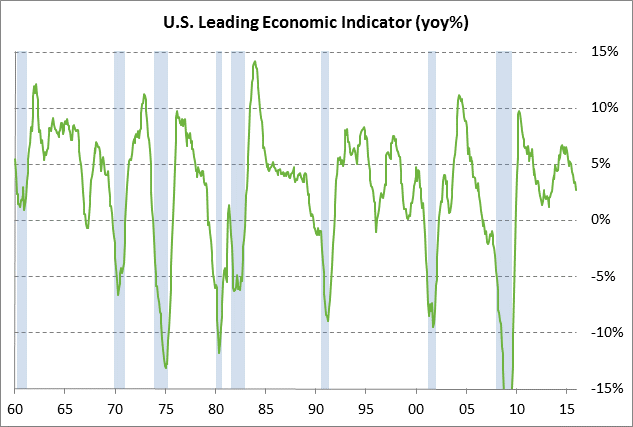

- Leading indicators expected to show the first back-to-back decline in more than 5 years

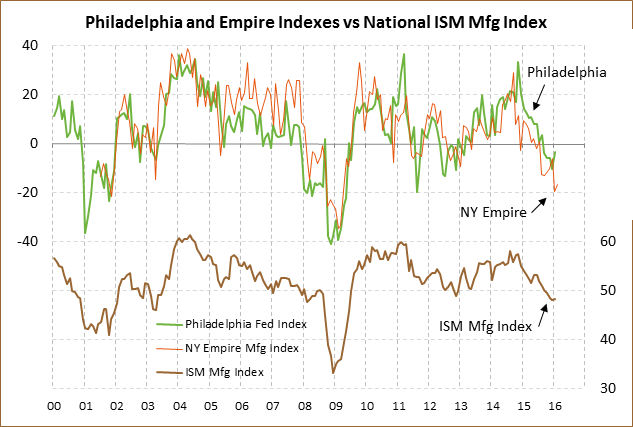

- Philadelphia Fed index expected to remain in negative territory for the sixth consecutive month

- 30-year TIPS auction to yield near 1.16%

- EIA report

FOMC minutes support deferred Fed rate hike expectations — Yesterday’s release of the minutes from the Jan 26-27 FOMC meeting showed that FOMC officials were worried about overseas turmoil, the U.S. stock market correction and widening credit spreads, and low U.S. inflation figures. Those various problems continued in the three weeks since the FOMC meeting, meaning officials are probably even more concerned now. Fed Chair Yellen at her testimony before Congress acknowledged various headwinds but said that the Fed remained on track to gradually raise interest rates. However, the federal funds futures market does not fully expect the FOMC to implement its next rate hike until late 2018, which is more than a year away. The fed funds futures market is discounting a zero chance for a rate hike at the next FOMC meeting on March 15-16.

The markets will be carefully watching the Fed’s new macroeconomic forecasts that will be released at the March 15-16 meeting to see whether the FOMC downgrades its GDP and inflation forecasts. The markets will also be watching the extent to which FOMC members lower their federal funds forecast to something closer to reality. The Fed dots released after the December FOMC meeting indicated a median FOMC member expectation for four rate hikes in 2016. The market now believes there will not even be one rate hike in 2016 let alone four rate hikes.

Unemployment claims are within shooting distance of decade-plus lows — The initial and unemployment claims series have fallen over the past several weeks and are not providing any evidence that businesses are laying off people due to the turmoil seen so far this year. Both series are within shooting distance of recent decade-plus lows. The initial claims series is only +14,000 above the 42-year low of 255,000 posted in July 2015 and the continuing claims series is only +93,000 above the 15-year low of 2.146 million posted in Oct 2015. The markets are expecting modest gains in today’s report. The market is expecting today’s initial claims report to show a +6,000 gain to 275,00, reversing part of last week’s -16,000 decline. Meanwhile, the market is expecting today’s continuing claims report to show a +11,000 gain to 2.250 million, reversing about half of last week’s -21,000 decline to 2.239 million.

Leading indicators expected to show the first back-to-back decline in more than 5 years — The markets are expecting today’s Jan leading indicators report to show a decline of -0.2%, matching December’s -0.2%. That would be the first back-to-back monthly decline since Aug-Sep 2011, i.e., in 5-1/4 years. The decelerating LEI does not bode well for the U.S. economic outlook. On a year-on-year basis, the LEI in December eased to a 2-1/2 year low of +2.7% y/y.

U.S. GDP fell to +0.7% in Q4 due to weak business investment, government spending, net exports, and inventories. Nevertheless, the market is still relatively sanguine about near-term GDP forecast with a consensus expectation for U.S. GDP to recover to +2.2% in Q1 and then average about +2.1% in the last three quarters of 2016. On a calendar year basis, the consensus is for GDP in 2016 to be little changed from 2015 at +2.2%.

Philadelphia Fed index expected to remain in negative territory for the sixth consecutive month — The market is expecting today’s Feb Philadelphia Fed business outlook index to show a small +0.5 increase to -3.0, adding to January’s +6.7 point increase to -3.5. Business confidence is clearly negative in the Philadelphia area since today’s report is expected to be the sixth consecutive month that the index has been below zero. The Feb Empire index earlier this week rose by +2.73 points to -16.64 but remained in negative territory for the 7th consecutive month.

U.S. business confidence remains weak across the board. The ISM manufacturing index has been below the expansion-contraction level of 50.0 for the last four reporting months of Oct-Jan, indicating the extent of pessimism among manufacturing executives. The U.S. manufacturing sector continues to be hurt by lackluster U.S. growth, weak overseas growth, and the strong dollar that is depressing overseas demand for U.S. manufactured goods. Confidence in the non-manufacturing sectors of the U.S. economy has also been slipping. The ISM non-manufacturing index has fallen by a net -3.8 points in the past five months to post a new 2-1/2 year low of 55.8 in December.

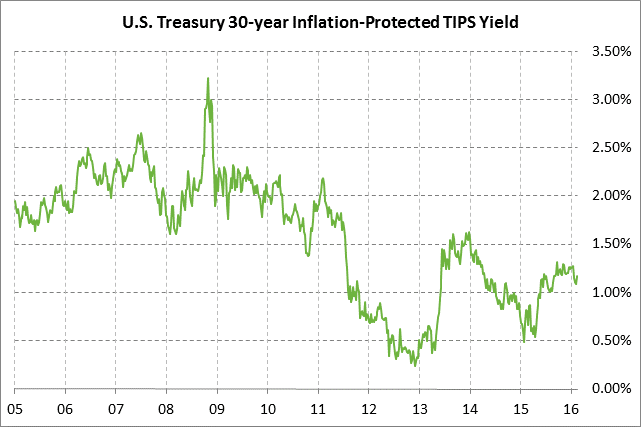

30-year TIPS auction to yield near 1.16% — The Treasury today will sell $7 billion of new 30-year TIPS. The Treasury in recent years has sold a new 30-year TIPS in February and has then conducted reopenings of that issue in June and October. The $7 billion size of today’s 30-year TIPS is down from the $9 billion size seen in recent years as the Treasury carries out its plan to reduce coupon auctions and increase T-bill auctions. Today’s 30-year TIPS was trading at 1.16% late yesterday afternoon. The 12-auction averages for the 30-year TIPS are as follows: 2.54 bid cover ratio, $17 million in non-competitive bids, 7.3 bp tail to the median yield, 15.5 bp tail to the low yield, and 43% taken at the high yield. The 30-year TIPS is mildly above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 56.2% of the last twelve 30-year TIPS auctions, which is mildly above the average of 55.1% for all recent Treasury coupon auctions.

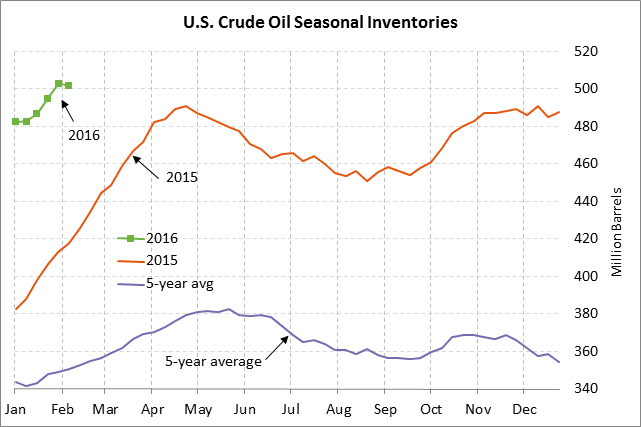

EIA report — The market consensus for today’s weekly EIA report is for a +3.5 mln bbl rise in crude oil inventories, a +400,000 bbl rise in gasoline inventories, a -1.5 mln bbl decline in distillate inventories, and a -0.5 point decline in the refinery utilization rate to 85.6%.