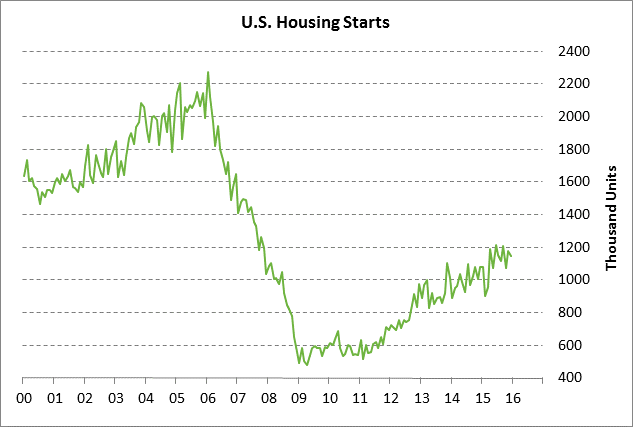

- Housing starts expected to remain generally strong

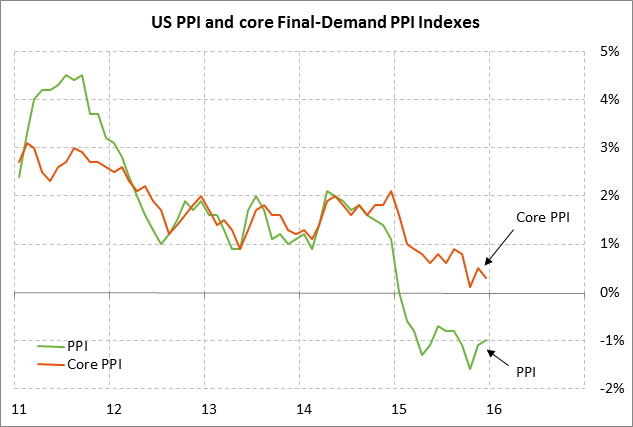

- PPI expected to strength slightly

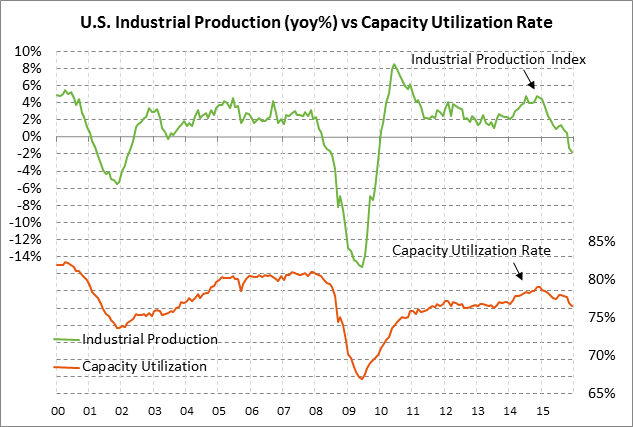

- Jan industrial production expected to rebound

- FOMC minutes may shed some light on the extent of the Fed’s concern about overseas turmoil and financial market volatility

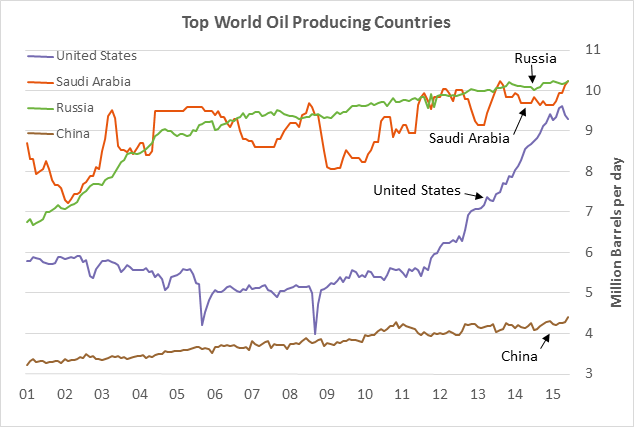

- Crude oil prices sink after Russian-Saudi agreement to freeze production

Housing starts expected to remain generally strong — The market is expecting today’s Jan housing starts report to show a modest increase of +1.8% to 1.170 million, recovering some of December’s -2.5% decline to 1.149 million. Meanwhile, the consensus is for Jan building permits to show a -0.3% decline to 1.200 million, adding to December’s -6.1% decline to 1.204 million. U.S. housing starts posted an 8-1/4 year high of 1.211 million units in June 2015 but have since been bouncing around below that high. In December. housing starts were down by -5.1% from June’s 8-1/4 year high but remained at a generally high level.

U.S. home builders continue to build new homes at a relatively strong pace due to strong demand, tight supplies, and high new home prices. New home sales in December rose +10.8% to 544,000 units, which was just slightly below the 7-3/4 year high of 545,000 units posted in Feb 2015. The supply of new homes on the market remains relatively tight at 5.2 months, which is below the long-term average of 6.1 months. The price of a new home in December of $288,900 was only -6% below the record high of $307,600 posted in Sep 2015. Yesterday’s U.S. NAHB housing market index fell by -3 points to 58, which was down by -0.8 points from the 10-year high of 65 posted in Oct 2015. The NAHB index shows that U.S. home builders confidence is still generally high but that the turmoil seen so far this year may be taking a toll on home builder confidence and that they may slightly cut back their near-term construction plans.

PPI expected to strength slightly — The market is expecting today’s Jan final-demand PPI to strengthen mildly to -0.6% y/y from Dec’s -1.0% and for the core PPI to edge higher to +0.4% y/y from Dec’s +0.3%. Despite today’s expected rise, the PPI will still be at a depressed level well below the Fed’s +2.0% inflation target. Indeed, the overall inflation outlook remains stable to weak with the PCE deflator, the Fed’s preferred inflation measure, at only +0.6% y/y and the core PCE deflator at only +1.4%, +0.1 point above the 4-1/2 year low of +1.3% y/y posted during the first 10 months of 2015. Moreover, the core PCE deflator on a 3-month annualized basis fell to a 10-month low of +1.0% in December. With the continued weak inflation figures, the Fed is having an increasingly hard time arguing that inflation will move back up to its +2.0% target over the medium-term.

Jan industrial production expected to rebound — The market is expecting today’s Jan industrial production report to show a +0.3% increase, reversing most of December’s -0.4% decline. The headline industrial production report was depressed due to the warm weather in December that cut utility output, but industrial production in January is expected to bounce back after more normal weather in January.

Looking at just the manufacturing sector and excluding the effects of weather on utility production, the market is expecting today’s Jan manufacturing production report to show a +0.2% increase, more than reversing December’s -0.1% decline. The U.S. manufacturing sector barely has its head above water with manufacturing production in December falling to a 1-3/4 year low of +0.8% y/y. Meanwhile, the ISM manufacturing index has been below the expansion-contraction level of 50.0 for the last four reporting months of Oct-Jan, indicating the extent of pessimism among manufacturing executives. The U.S. manufacturing sector continues to be hurt by lackluster U.S. growth, weak overseas growth, and the strong dollar that is depressing overseas demand for U.S. manufactured goods.

FOMC minutes may shed some light on the extent of the Fed’s concern about overseas turmoil and financial market volatility — The market will be assessing today’s minutes from the Jan 26-27 FOMC meeting to see how worried FOMC members were about January’s overseas turmoil and the financial market volatility. The stock market sank after the FOMC’s post-meeting statement was released on Jan 27 on some disappointment that the Fed did not move to a more dovish post-meeting posture. The key sentence in the post-meeting statement was that “The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.” The FOMC at least dropped its previous language that the risks are balanced, meaning that the FOMC is now considering whether the risks are tilted to the downside. The market is discounting a near zero chance of a rate hike at the next FOMC meeting on March 15-16 and is not fully discounting the Fed’s next rate hike until Dec 2017.

Crude oil prices sink after Russian-Saudi agreement to freeze production — The crude oil market was underwhelmed by yesterday’s agreement between Russia and Saudi Arabia to freeze production at current levels. The markets had been hoping for an agreement to actually cut production, which is what will be necessary to offset the soon-to-be-flood of Iranian oil and to allow a drawdown of the current epic glut of world oil inventories. The markets were also skeptical of the announcement since the Russian-Saudi production freeze was made contingent on an agreement by all other major oil producers to freeze production. There is virtually no chance that Iran will agree to a production freeze, although Iran might be given some dispensation to allow it raise production on a limited basis. Still, the Russian-Saudi move for a production freeze was supportive for oil prices since it could be a stepping stone to an actual production cut later in the year if oil prices do not stabilize.