- Weekly market focus

- Global stocks on Monday receive boost from sharp yuan rally and continued recovery in crude oil prices

- This week’s U.S. economic calendar is expected to be biased toward stronger side

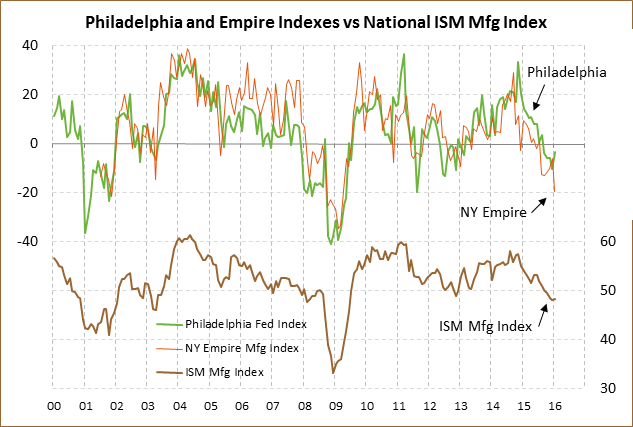

- Feb Empire index expected to recover moderately but remain below zero

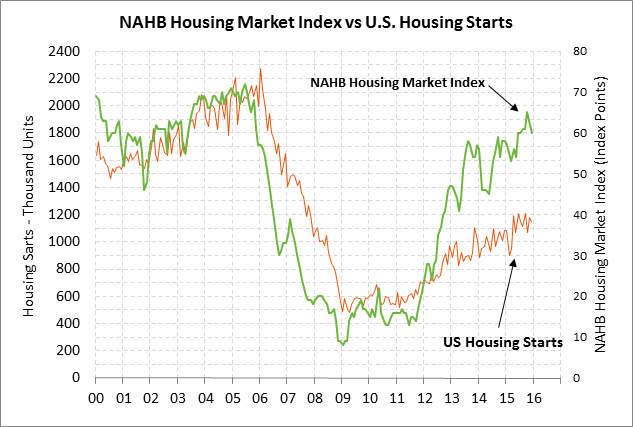

- Feb NAHB index expected to remain at strong level

- Q4 earnings season starting to wind down

Weekly market focus — The markets this week will focus on China, bank stocks, crude oil, and Fed policy. The Jan 26-27 FOMC minutes will be released on Wednesday and the Treasury will sell 30-year TIPS on Thursday.

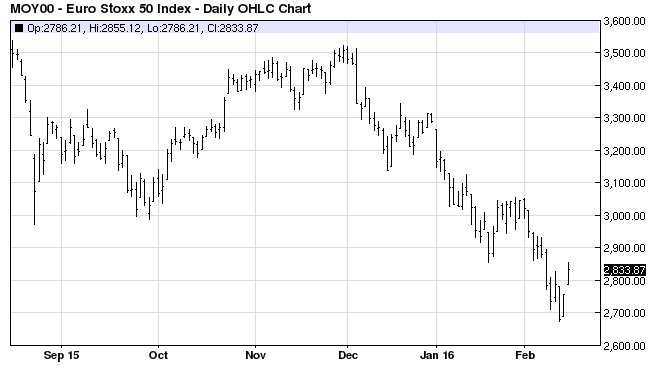

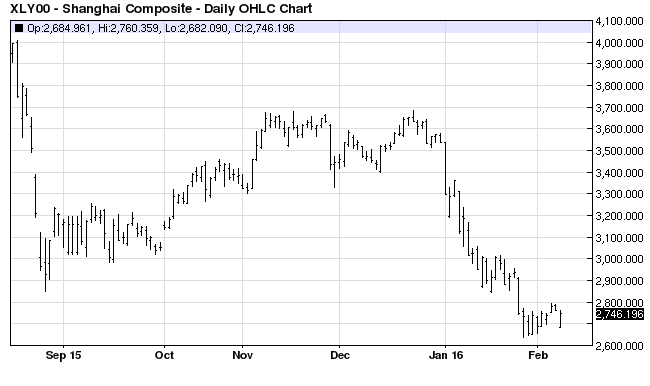

Global stocks on Monday receive boost from sharp yuan rally and continued recovery in crude oil prices — During Monday’s U.S. holiday, global stocks performed well and raised hopes for higher U.S. stocks this week. The Euro Stoxx 50 index on Monday rallied sharply by +2.82%, adding to last Friday’s +2.83% gain for a total 2-day gain of +5.65%. Japan’s Nikkei index on Monday closed sharply higher by +7.16%, reversing part of last week’s plunge of -11.10%. Meanwhile, the Shanghai index on Monday closed lower by only -0.63%, which was better than expected as Chinese stocks reopened after last week’s holiday.

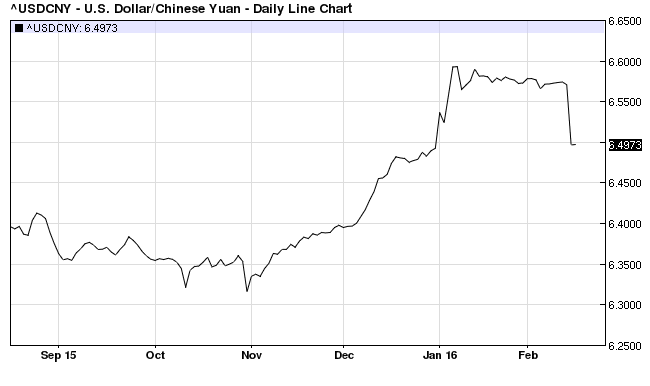

Monday’s favorable stock market performance was prompted by short-covering, a sharp rally in the yuan, and continued support from last Friday’s +10.98% rally in April Brent crude oil futures and Monday’s slightly higher Brent close of +0.09%. Crude oil prices rallied sharply last Friday after news that the Saudi Arabian and Russian oil ministers will meet today to discuss possible cooperation on a production cut. The yuan on Monday rallied very sharply by +1.19% against the dollar on Saturday’s comment by Chinese central bank chief Zhou’s comments in a Caixin interview that China’s balance of payments is good, that capital flows are normal, and that the yuan is stable against a basket of currencies.

The Japanese stock market was able to shake off Sunday’s news that Japan’s Q4 GDP fell -1.4% (q/q annualized), which was weaker than expectations of -0.8% and gave back more than Q3’s revised +1.3% gain (preliminary +1.0%). Japan on Monday night received the negative news that Japan’s final-Dec industrial production was revised lower to -1.7% m/m from -1.4%. The Chinese stock market on Monday was able to shake off the Sunday night news that China’s Jan exports fell -11.2% y/y, weaker than expectations of -1.8% y/y. Chinese Jan imports fell by an even larger -18.8% y/y versus expectations of -3.6%. The Chinese markets on Monday night saw a positive report from China’s Economic Information Daily that China is expected to soon release a package of monetary, fiscal, tax, and M&A policies to stimulate the Chinese economy in 2016.

This week’s U.S. economic calendar is expected to be biased toward stronger side — This week’s U.S. economic calendar is fairly busy and is expected to be biased toward the stronger side. Strong U.S. economic reports this week are expected to include (1) today’s Feb Empire manufacturing index (expected +8.87 to -10.50), (2) Wednesday’s Jan housing starts report (expected +2.3% after Dec’s -2.5%), (3) Wednesday’s Jan industrial production (expected +0.4% after Dec’s -0.4%), and (4) Thursday’s Feb Philadelphia Fed index (expected +0.5 to -3.0 after Jan’s +6.7 to -3.5).

Weak or neutral reports this week include (1) today’s Feb NAHB index (expected unchanged at 60 after Jan’s unchanged report), and (2) Thursday’s Jan leading indicators (expected -0.2% after Dec’s -0.2%). On the inflation front, the PPI and CPI reports are expected to be steady to higher. Wednesday’s Jan PPI is expected to strengthen to -0.6% y/y from Dec’s -1.0% and the Jan core PPI is expected to strengthen to +0.4% from Dec’s +0.3% y/y. Friday’s Jan CPI is expected to strengthen to +1.3% y/y from Dec’s +0.7%, but the Jan core CPI is expected to be unchanged from Dec at +2.1% y/y.

Feb Empire index expected to recover moderately but remain below zero — The markets will be watching today’s Empire index for the first U.S. manufacturing information for February. The market is expecting today’s Feb Empire manufacturing index to show a +8.87 gain to -10.50, reversing part of January’s -13.16 point decline to -19.37. Despite today’s expected gain, the index is expected to remain in negative territory for the seventh consecutive month, indicating that NY-area manufacturing executives remain pessimistic about conditions in their district. On a national level, the ISM index in 2015 fell for six straight months from July through December by a total of -5.1 points to a 6-1/2 year low of 28.0 in Dec, but then rebounded slightly higher by +0.2 points to 48.2 in January.

Feb NAHB index expected to remain at strong level — The market is expecting today’s Feb NAHB housing market index to be unchanged at 60 for the third consecutive month. The NAHB index posted a 10-year high of 65 in October but then fell by a total of -5 points in Nov-Dec to 60. Despite that dip, the index shows that U.S. home builders are still generally confident about the market for building new homes. New home sales rose by a total of +19% over the last three reporting months to 544,000 in December, which was just slightly below the 7-3/4 year high of 545,000 posted in Feb 2015.

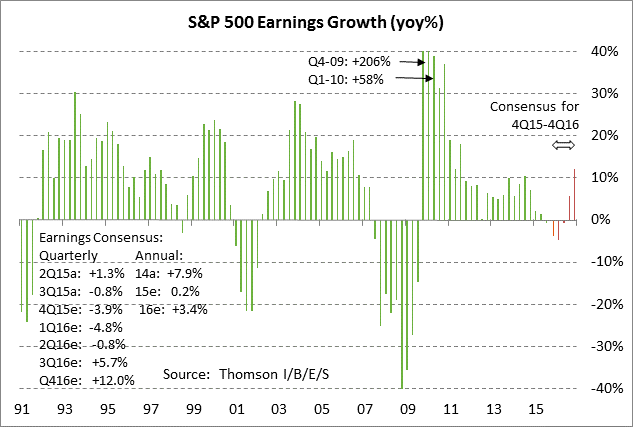

Q4 earnings season starting to wind down — The Q4 earnings season is winding down but there are still 53 of the S&P 500 companies that report earnings this week. The market consensus is for Q4 earnings to drop -3.9% y/y, according to Thomson I/B/E/S. The market is then expecting earnings to remain negative at -4.8% in Q1 and -0.8% in Q2, finally improving to +5.7% in Q3 and +12.0% in Q4. On a calendar year basis, the consensus is for earnings to improve to +3.4% in 2016 from +0.2% in 2015. Of the 381 reporting SPX companies, 68% have reported above-consensus earnings, better than the long-term average of 63% but below the 4-quarter average of 69%.