- U.S. retail sales expected to show another lackluster month

- U.S. consumer sentiment remains generally strong so far despite financial market turmoil

- U.S. import prices expected to show another sharp decline

- U.S. business inventories are high and continue to be a threat to U.S. GDP growth

- Weekly market focus

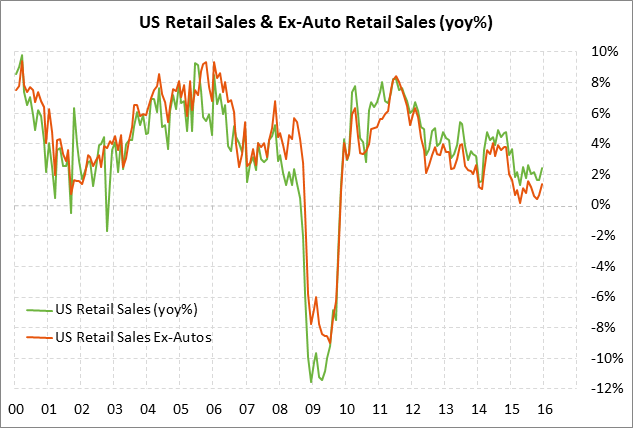

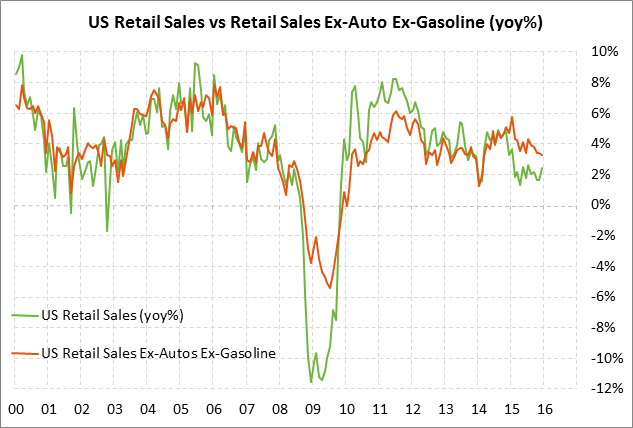

U.S. retail sales expected to show another lackluster month — The market is expecting today’s Jan retail sales report to show a small headline increase of +0.1% m/m and to be unchanged ex-autos. That would be slightly better than the Dec report of -0.1% for both the headline and ex-autos figures. Excluding both autos and the effect of low gasoline prices in pushing down the dollar value of retail sales, the market is expecting today’s retail sales ex-autos and ex-gasoline to show a little more respectable increase of +0.3% following December’s unchanged report. In Q4, retail sales showed weak reports of unchanged in Oct, +0.4% in Nov, and -0.1% in Dec.

The markets are clearly worried about consumer spending, which is basically the only thing holding up the U.S. economy. In the breakdown of the recent Q4 GDP report of +0.7%, personal spending contributed +1.46 points to GDP while business investment and government spending made negligible contributions of +0.03 and +0.12 points, respectively. Meanwhile, net exports and inventory investment subtracted -0.47 points and -0.45 points from GDP, respectively.

Fed Chair Yellen in her testimony to a House committee on Wednesday said that the Fed believes that “ongoing employment gains and faster wage increases should support the growth of real incomes and therefore consumer spending.” However, if consumer spending remains weak despite higher incomes, then the U.S. economy will show weak GDP figures that could dampen confidence enough to cause the U.S. economy to slowly slide into a recession.

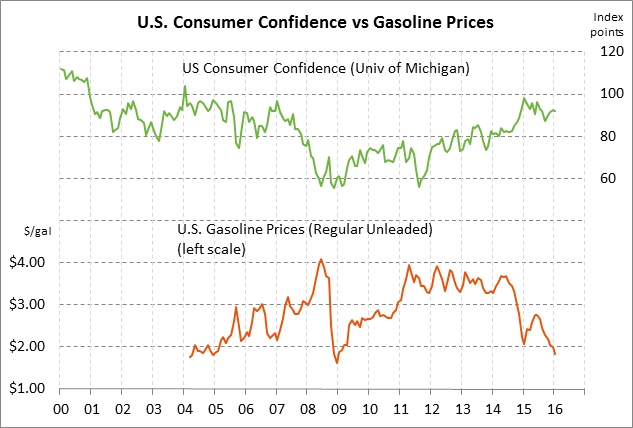

U.S. consumer sentiment remains generally strong so far despite financial market turmoil — The market is expecting today’s preliminary-Feb U.S. consumer sentiment index from the University of Michigan to show a +0.5 increase to 92.5, reversing most of January’s decline of -0.6 to 92.0. It would be rather remarkable if today’s consumer sentiment report can show an increase of +0.5 points after only a -0.6 point decline in January considering all the recent financial market turmoil.

The U.S. consumer confidence level of 92.0 in January was only -6.1 points below the 12-year high of 98.1 posted in Feb 2015, illustrating that consumers still remain generally confident about the U.S. economy. U.S. consumer sentiment is seeing support from the generally strong labor market, rising wages, and low gasoline prices. U.S. consumers have mostly ignored recent negative factors such as the stock market correction and the soft Q4 GDP report of only +0.7%.

U.S. import prices expected to show another sharp decline — The market is expecting today’s Jan import price index to show another sharp decline of -1.5% m/m and -6.8% y/y following Dec’s report of -1.2% m/m and -8.2% y/y. U.S. import prices continue to see sharp downward pressure from the plunge in oil and commodity prices and from the downward impact from the strong dollar. Falling crude oil prices clearly do not account for all the weakness in import prices since U.S. import prices ex-petroleum in December fell to a 6-1/4 year low of -3.7% y/y.

The weakness in import prices is one of the factors putting downward pressure on the PCE deflator, which is the Fed’s preferred inflation measure. The PCE deflator in December rose by only +0.6% y/y and the core PCE deflator rose by only +1.4% y/y, well below the Fed’s inflation target of +2.0%.

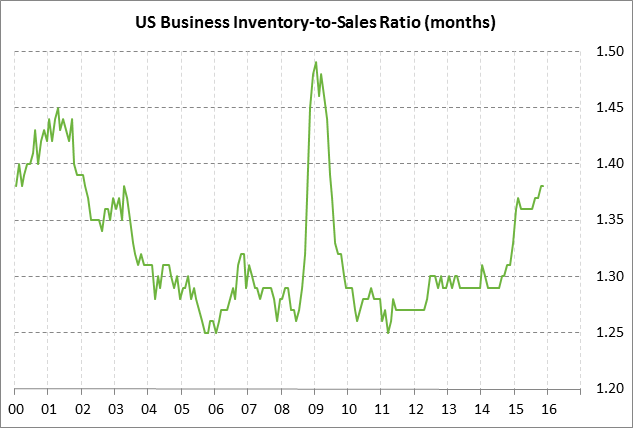

U.S. business inventories are high and continue to be a threat to U.S. GDP growth — The market is expecting today’s Dec business inventories report to show an increase of +0.2%, reversing November’s -0.2% decline. U.S. inventories are at elevated levels as seen by the fact that the business inventory-to-sales ratio in November was at a 6-1/2 year high of 1.38 months. The current level of inventories of 1.38 months is well above the 1.29 average seen in 2006/07 before the 2007/09 recession, illustrating that the U.S. economy needs to see a larger inventory correction before businesses will be under pressure to order new goods to replenish their shelves. An inventory correction already subtracted -0.7 points from Q3 GDP and -0.5 points from Q4 GDP and the inventory correction has further to go, which will keep downward pressure on GDP in the first half of 2016.

Weekly market focus — The markets next week will continue to focus on China, European bank stocks, crude oil, and Fed policy. The Jan 26-27 FOMC minutes will be released on Wednesday and the Treasury will sell 30-year TIPS on Thursday. Next week’s U.S. economic calendar is fairly busy and is expected to be mixed. Strong U.S. economic reports next week include (1) Tuesday’s Feb Empire manufacturing index (expected +9.37 to -10.00), (2) Wednesday’s Jan housing starts report (expected +2.5% after Dec’s -2.5%), (3) Wednesday’s Jan industrial production (expected +0.3% after Dec’s -0.4%), and (4) Thursday’s Feb Philadelphia Fed index (expected +0.6 to -2.9 after Jan’s +6.7 to -3.5). Weak or neutral reports next week include (1) Tuesday’s Feb NAHB index (expected unchanged at 60 after Jan’s unchanged report), and (3) Thursday’s Jan leading indicators (expected -0.2% after Dec’s -0.2%). On the inflation front, the PPI and CPI reports are expected to be steady to higher. Wednesday’s Jan PPI is expected to strengthen to -0.6% y/y from Dec’s -1.0% and the Jan core PPI is expected to strengthen to +0.5% from Dec’s +0.3% y/y. Friday’s Jan CPI is expected to strengthen to +1.3% y/y from Dec’s +0.7%, but the Jan core CPI is expected to be unchanged from Dec at +2.1% y/y.