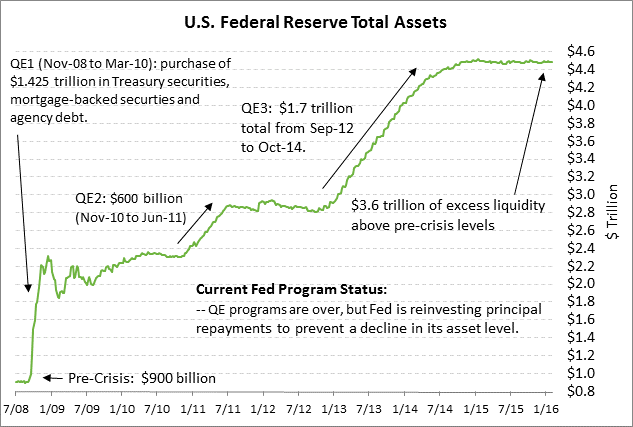

-

- Yellen doesn’t budge much on raising interest rates

- Unemployment claims are elevated but remain within shooting distance of recent decade-plus lows

- 30-year T-note auction to yield near 2.51%

Yellen doesn’t budge much on raising interest rates — Fed Chair Yellen yesterday, on the first day of her 2-day appearance before Congressional committees, said that the Fed is still on track to raise interest rates at a gradual rate. However, she did note that there are various risks for the U.S. economy that could cause the Fed in the future to shift its view on raising interest rates.

Commenting on these risks, Ms. Yellen said that “Financial conditions in the United States have recently become less supportive of growth, with declines in the broad measures of equity prices, higher borrowing rates for riskier borrowers, and a further appreciation of the dollar.” She said that, “These developments, if they prove persistent, could weigh on the outlook for economic activity and the labor market, although declines in longer term interest rates and oil prices provide some offset.”

She also noted that, “Foreign economic developments… pose risks to U.S. economic growth.” She also said that low commodity and oil prices could “trigger financial stresses in commodity-exporting economies, particularly in vulnerable emerging market economies, and for commodity-producing firms in many countries.” On the overseas and commodity-related risks, she said, “Should any of these downside risks materialize, foreign activity and demand for U.S. exports could weaken and financial market conditions could tighten further.”

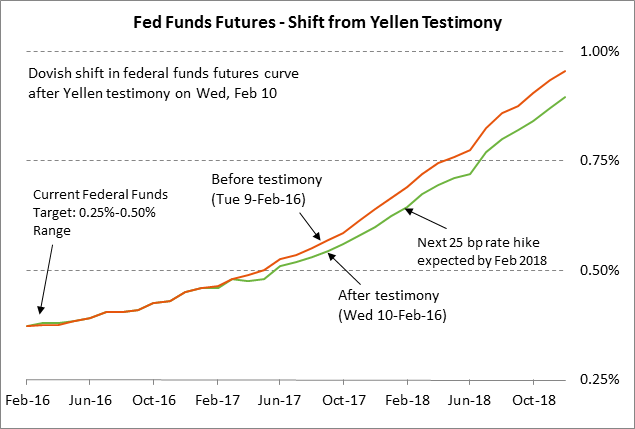

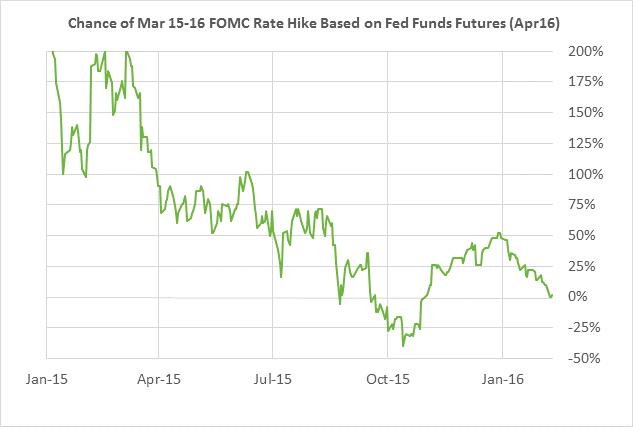

While noting these various risks, Ms. Yellen also outlined a variety of more positive developments in the U.S. economy that justify the Fed’s plan to continue raising interest rates. Ms. Yellen effectively said that the Fed is in a “watch and wait” mode whereby it is reassessing the current balance of risks. Ms. Yellen gave no indication of how likely a rate hike might be at the FOMC’s next meeting on March 15-16. The market is assessing only a 2% chance of a +25 bp rate hike at that meeting.

The federal funds futures market showed a mildly dovish shift in response to Ms. Yellen’s comments on Wednesday. The federal funds futures curve (on a yield basis) showed no movement for the remainder of 2016, but fell by -4 bp on the Dec 2017 futures contract and by -6 bp on the Dec 2018 contract. The federal funds futures market is not fully discounting the Fed’s next +25 bp rate hike until Feb 2018 and the following 25 bp rate hike until Nov 2018.

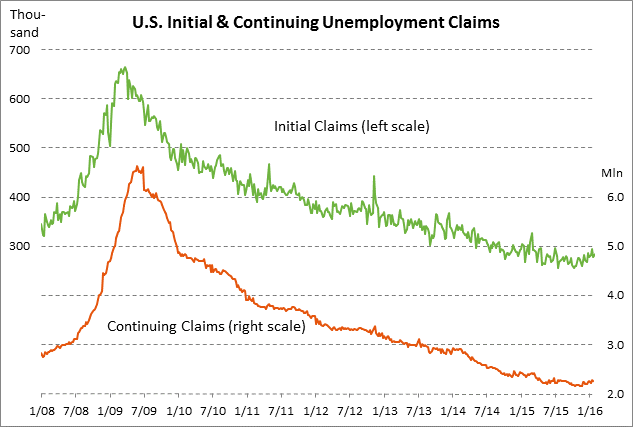

Unemployment claims are elevated but remain within shooting distance of recent decade-plus lows — The markets are watching the unemployment claims data carefully to assess whether businesses are beginning to lighten up on their staffing levels due to the recent financial volatility and shaky economic data. The initial and continuing unemployment claims series in recent weeks have been mildly elevated, but not to the extent of any major concern since they are still within shooting distance of recent decade-plus lows. The initial claims series is +30,000 above its 42-year low of 255,000 posted in July 2015 while the continuing claims series is +109,000 above its 15-year low of 2.146 million posted in Oct 2015.

The market is expecting today’s initial unemployment claims report to show a -5,000 decline to 280,000, reversing part of last week’s +8,000 gain to 285,000. Meanwhile, the market is expecting today’s continuing claims report to show a -10,000 decline to 2.245 million, adding to last week’s decline of -18,000 to 2.255 million.

30-year T-note auction to yield near 2.51% — The Treasury today will sell $15 billion of 30-year T-bonds, concluding this week’s $52 billion refunding operation. The Treasury today will sell a new 30-year bond as opposed to reopening a previous issue. The $15 billion size of today’s new 30-year bond auction is $1 billion smaller than the $16 billion size since seen since Nov 2009, reflecting the Treasury’s plan to reduce coupon sales and boost T-bill sales.

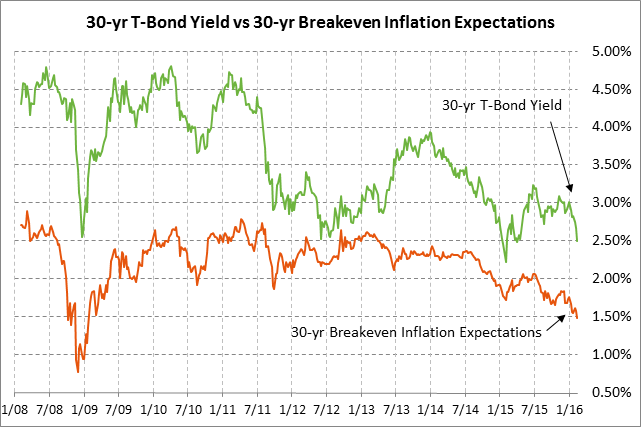

Today’s 30-year T-bond was trading at 2.51% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of 1.04% against the current 30-year breakeven inflation expectations rate of 1.47%. The 12-auction averages for the 30-year are as follows: 2.33 bid cover ratio, 5.3 bp tail to the median yield, 14.5 bp tail to the low yield, and 59% taken at the high yield. The 30-year T-bond is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 55.1% of the last twelve 30-year auctions, matching the average of 55.1% for all recent Treasury coupon auctions.