- Payrolls expected to show a trend increase and unemployment rate is expected to remain at a 7-3/4 year low

- U.S. trade deficit expected to widen slightly

- U.S. consumer credit expected to show below-trend growth

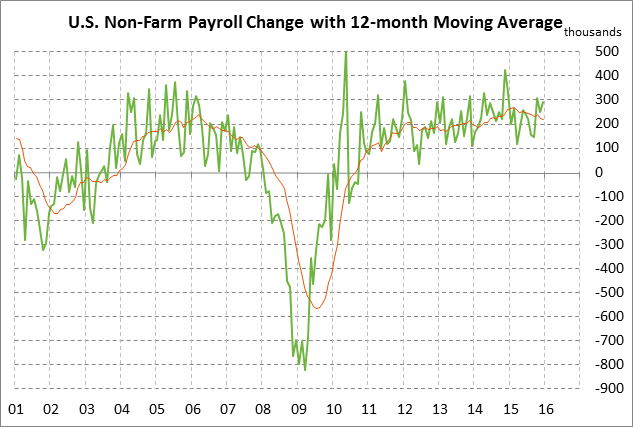

Payrolls expected to show a trend increase and unemployment rate is expected to remain at a 7-3/4 year low — The market is expecting today’s Jan payroll report to fall back to a longer-term near-trend increase of +190,000 after the surprising strength seen in Q4 (Oct +307,000, Nov +252,000, Dec +292,000). Wednesday’s Dec ADP report of +205,000 was mildly above expectations of +193,000 and supported the view for a near-trend increase in today’s payroll report.

It will be difficult for today’s Jan payroll report to keep up with the 3-month average of an impressive +284,000. Indeed, the downside stock market correction in January and the turmoil caused by China and the 12-year low in oil prices may have caused some businesses to get cold feet about hiring more workers in January and caused them to wait until they have a chance to see how things shake out.

A weaker-than-expected Jan payroll report today would contribute to the sense in the market that the U.S. economy is losing some momentum. A stronger-than-expected Jan payroll report today, by contrast, would support the view that the U.S. economy is still muddling through its various challenges and is in decent shape, all considered.

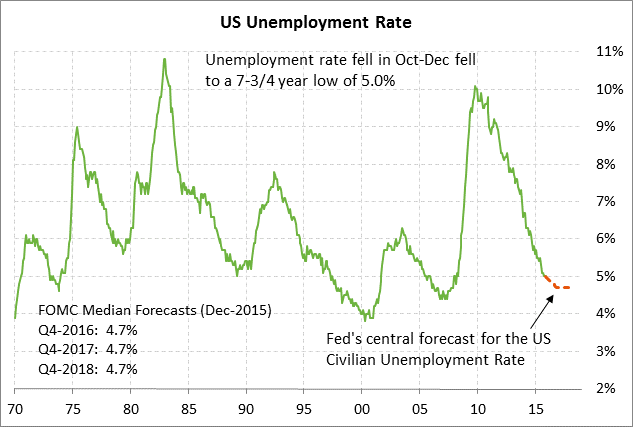

The market consensus is for today’s Jan unemployment report to be unchanged from the 7-3/4 year low of 5.0% posted in the last three reporting months of Oct-Dec. The unemployment rate is only +0.3 points above the Fed’s forecast that the unemployment rate by late this year will fall to 4.7% and remain at that level through 2017-18.

However, the Fed knows that the unemployment rate has fallen as quickly as it has in the past several years partially because of a shrinking labor force as opposed to falling only because of a vast number of new jobs. Indeed, the labor force participation rate in Sep/Oct fell to a 38-year low of 62.4% and rebounded to just 62.6% in Dec, indicating that only 62.6% of the U.S. population is engaged in the labor market with a job or looking for a job. That is sharply below the record high of 67.3% posted in early 2000. The U.S. labor market has been shrinking because (1) baby-boomers have started to retire, (2) many people went back to school while the economy was in the dumps or joined the underground economy, and (3) some people simply became discouraged about the job prospects and quit looking for a job altogether.

The Fed also remains concerned about the persistently high level of long-term unemployment, which is a serious problem since those unemployed people become less employable as time goes on because they lose skills and contacts. The share of the long-term unemployed (i.e., unemployed 27 weeks or longer) fell to a 6-3/4 year low of 25.7% in November and then rose slightly to 26.3% in December, which was far above the pre-recession (2000-07) average of 17.5%.

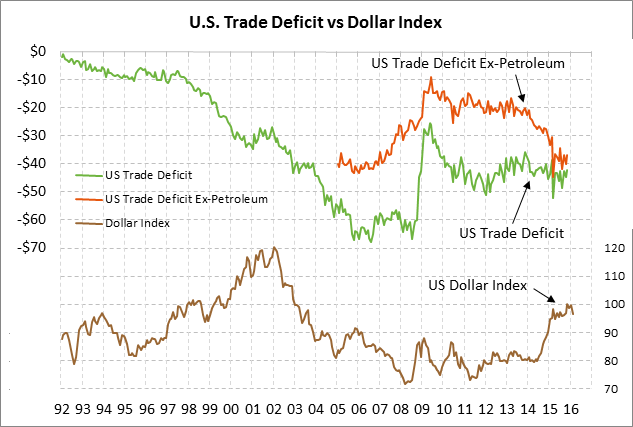

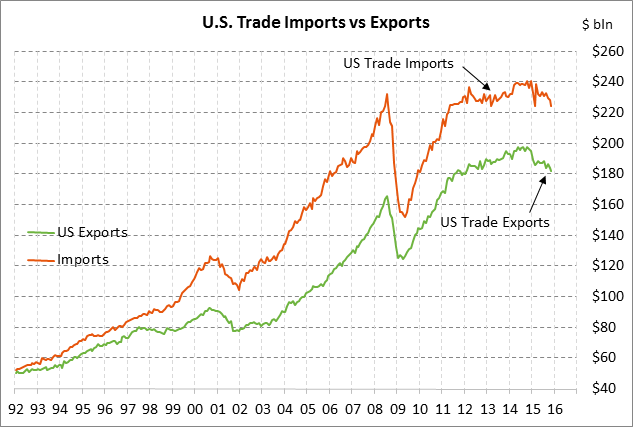

U.S. trade deficit expected to widen slightly — The market is expecting today’s Dec trade deficit to expand mildly to -$43.20 billion from -$42.37 billion in November. Today’s expected report of -$43.20 billion would be fairly close to the 12-month average of -$44.5 million, indicating that the market is looking for the sideways trend in the U.S. trade deficit to generally continue.

The U.S. trade deficit is moving generally sideways as exports and imports are seeing similar weakness. U.S. exports hit a record high of $197.8 billion in Oct 2014 but have since fallen by -7.9% and posted a new 3-3/4 year low of $182.2 billion in November. U.S. exports in November were down -7.1% y/y. U.S. exports have been hurt by (1) the strong dollar, which makes U.S. exports more expensive and less competitively priced, and (2) weak overseas growth that has reduced demand for U.S. products.

Meanwhile, U.S. imports have also been weak, falling by -6.6% from the record high of $240.5 billion posted in Dec 2014 to the 9-month low of $224.6 billion posted in November. Imports in Nov were down by -4.9% y/y. U.S. imports have seen downward pressure from lackluster U.S. economic growth and from the plunge in oil prices, which has reduced the dollar value of U.S. oil imports.

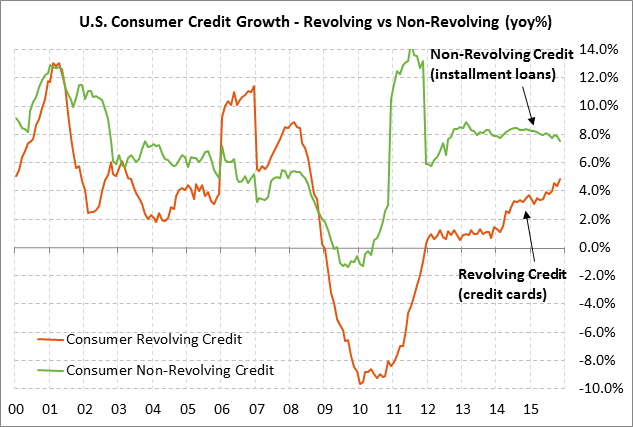

U.S. consumer credit expected to show below-trend growth — The market is expecting today’s Dec consumer credit report to show an increase of +$16.0 billion, recovering a bit from Nov’s weak report of +$13.95 billion but remaining below the 12-month trend average of +$18.8 billion. U.S. consumer credit has been below-trend in the past two reporting months of Oct-Nov, suggesting some consumer reluctance to take on more debt. In addition, some consumers are using their savings from lower gasoline prices to pay down their credit card balances, thus reducing revolving credit.

Most of U.S. credit growth continues to come from installment loans rather than credit cards. U.S. installment debt (e.g., car and student loans) was strong at +7.6% y/y in Nov, well above the +4.9% y/y growth in revolving credit growth (i.e., credit cards). However, U.S. installment debt growth has been slowing as seen by the fact that the Nov year-on-year figure of +7.6% y/y was a 3-1/3 year low. Consumer credit card debt, by contrast, posted a 7-1/3 year high of +4.9% in November.