- Weekly market focus

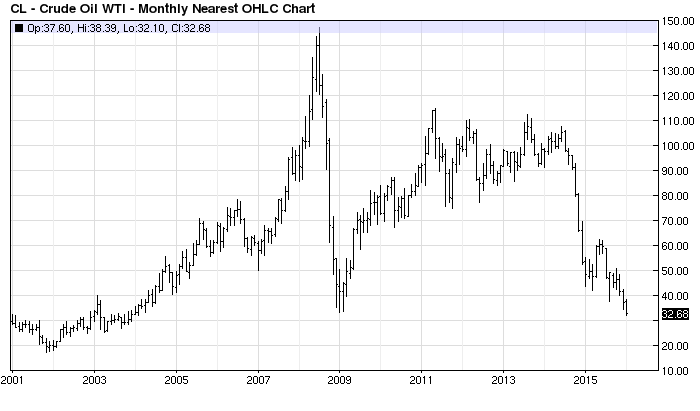

- Oil prices will remain weak as Iranian flood of oil grows closer

- Fed expectations turn more dovish with Chinese turmoil and U.S. stock market correction

- Q4 earnings season begins with poor expectations

Weekly market focus — The markets this week will focus on (1) whether the turmoil continues in China with fresh negative carry-over for the world economy and world financial markets, (2) whether oil prices this week extend last week’s -10.5% sell-off to a 12-year low, (3) whether the U.S. stock market extends its downward correction on the Chinese turmoil and the weakness in oil and commodity prices, (4) last week’s dovish shift in expectations for the Fed’s next rate hike, (5) the beginning of Q4 earnings season today, and (6) this week’s Treasury auction package of $58 billion of 3-year and 10-year T-notes and 30-year bonds.

This week’s U.S. economic schedule is relatively light with key reports including Wednesday’s Fed Beige Book and Thursday’s Dec import price index (expected -1.4% m/m). Friday brings a raft of reports that include Dec retail sales (expected -0.1% and +0.2% ex-autos), Dec PPI (expected -1.0% y/y and core +0.3%), Dec industrial production (expected -0.1% after Nov’s -0.6%), and the preliminary-Jan University of Michigan U.S. consumer confidence index (expected unchanged after Dec’s +1.3).

Last Friday’s strong Dec payroll report of +292,000 and the +41,000 upward revision for Nov to 252,000, put the U.S. economic data in a more positive light. However, last week’s downward correction in the U.S. stock market and the concern about the Chinese and world economy overshadowed the payroll report as the markets worry about a further deterioration of the U.S. manufacturing sector and about reduced U.S. business and consumer confidence.

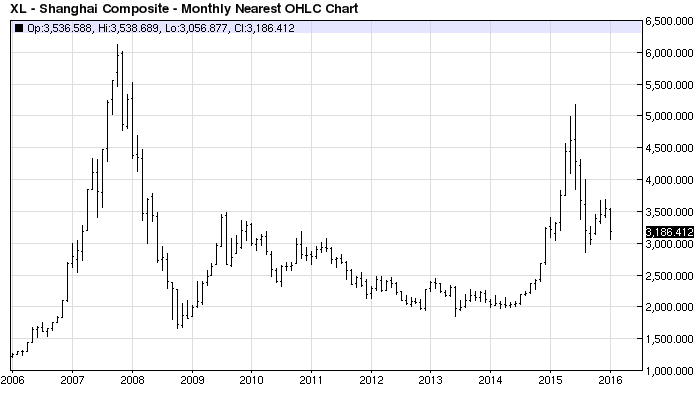

Chinese stock market stabilizes on Friday after circuit breakers were dropped — The Shanghai Composite index last Friday managed to close +1.97% higher after Chinese regulators on Thursday suspended circuit breakers, thus reducing investor concerns about getting locked into the market without being able to sell. Trading was halted for the day last Monday and Thursday by the -7% circuit breaker. The Shanghai Composite index last week closed -10.0%, adding to the previous week’s -2.5% sell-off.

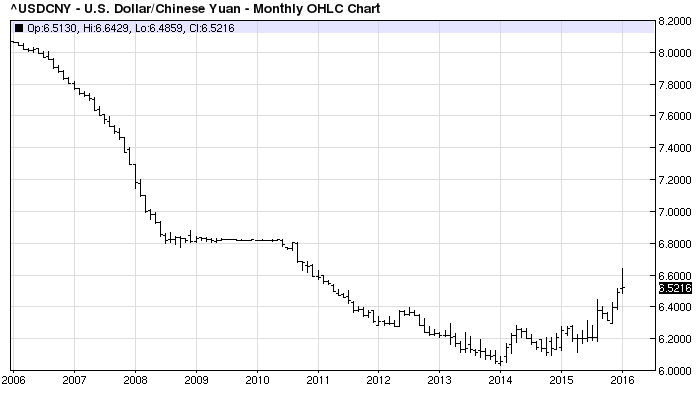

Despite last week’s -10% sell-off, the Shanghai index closed the week well above the 1-year low posted in Aug 2015 by +11.8% and more than +50% above the mid-2014 level that prevailed before the Chinese stock market bubble started to emerge in late 2014. That indicates that there could still be plenty of downside potential for the Chinese stock market given the likelihood for further yuan depreciation and uncertainty about the health of the Chinese economy. The yuan last week closed -1.6% lower against the dollar as the Chinese central bank guided the currency lower in an attempt to stimulate exports. However, the weaker yuan also sparked capital flight as investors worry about the declining value of their yuan-denominated investments. China saw an outflow of about $267 billion over the 3-month period of Sep-Nov as investors moved their capital overseas to seek better returns.

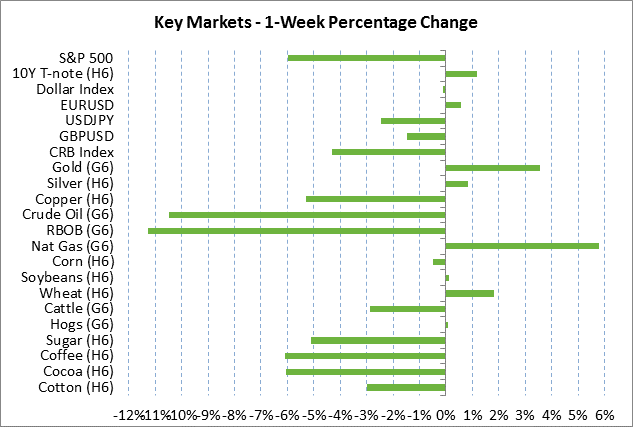

Oil prices will remain weak as Iranian flood of oil grows closer — Oil prices could see a temporary reprieve this week if the Chinese turmoil subsides and if concerns ease a bit about the Chinese economy and reduced energy demand. However, there is no sign as yet that Saudi Arabia and its Gulf partners plan to let up on their price war on high-cost producers in an attempt to protect their market share. Moreover, the process keeps marching forward toward dropping sanctions on Iran, which will lead to a flood of new Iranian production and exports by mid-year.

Meanwhile, the glut of crude oil in the U.S. continues as oil producers drag their feet on cutting production in response to lower prices. U.S. oil production has so far dropped by only -4% from the 43-year high posted in June 2015, meaning oil continues to flood into storage. U.S. oil inventories are currently a massive +36.1% (128 million bbls) above the 5-year seasonal average. We look for oil prices show continued weakness this year until producers cut production by enough to fall below the tepid level of world demand and allow the epic glut of world oil inventories to subside.

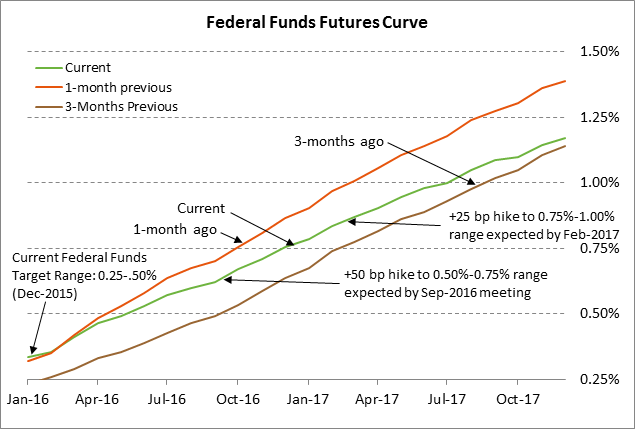

Fed expectations turn more dovish with Chinese turmoil and U.S. stock market correction — The market last week substantially deferred expectations for the timing of the Fed’s next rate hike due to the turmoil in China and the downward correction in the U.S. stock market. The federal funds futures market now is not fully discounting the Fed’s next rate hike until September (versus previous expectations of June) and the following rate hike until Feb 2017 (versus previous expectations of Dec 2016). With the lackluster global economy and with U.S. inflation showing no signs of rising towards the Fed’s +2.0% target, the Fed is under no pressure to implement its next rate hike. Indeed, the markets are in need of some cheer-leading by the Fed as the U.S. economy takes a hit from the petroleum-sector recession and as business and consumer confidence takes a hit from overseas turmoil.

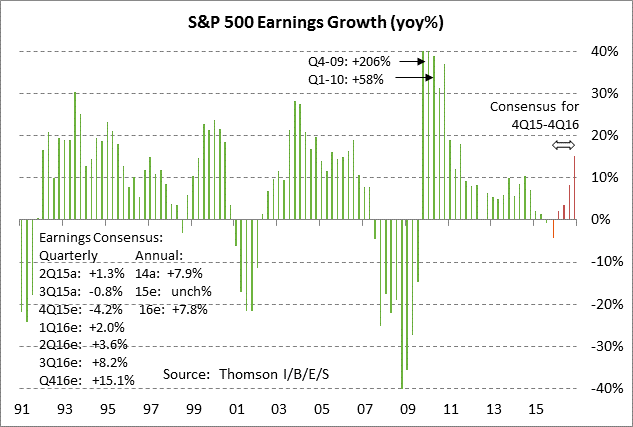

Q4 earnings season begins with poor expectations — Q4 earnings season unofficially begins today with Alcoa’s Q4 earnings report. There are a total of 11 SPX companies that report earnings this week with other notable reports including JP Morgan Chase and Intel on Thursday, and Citigroup, Wells Fargo, US Bancorp and Blackrock on Friday. The market consensus for Q4 2015 earnings is for a decline of -4.2%. The market is then expecting earnings to improve in 2016 to +2.0% in Q1, +3.6% in Q2, +8.2% in Q3, and +15.1% in Q4. On a calendar year basis, the market is expecting earnings to improve to +7.5% in 2016 after being unchanged in 2015.