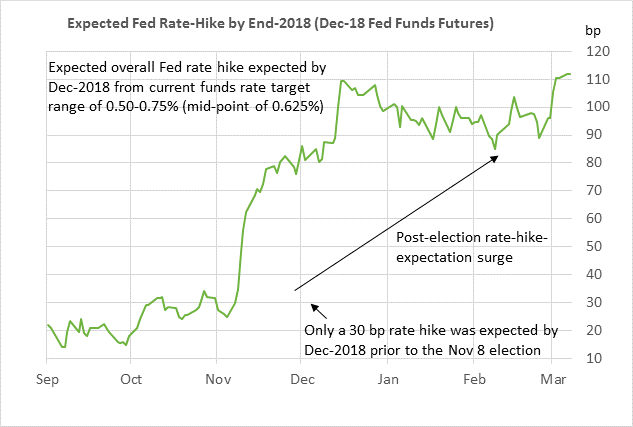

- Former Fed official Kocherlakota raises possibility that FOMC had a recent video conference to decide on a rate hike

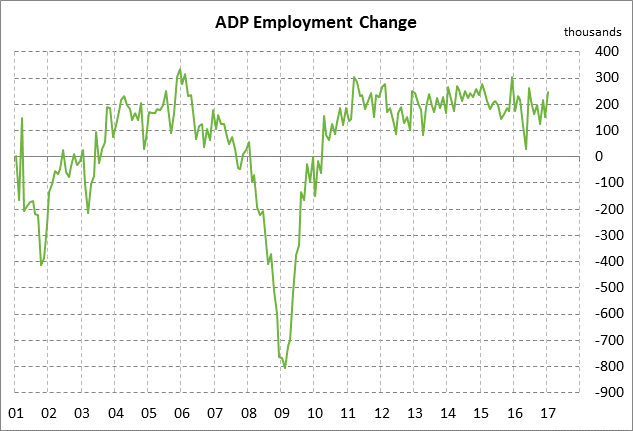

- ADP employment expected to show trend increase

- 10-year T-note auction to yield near 2.53%

- Weekly EIA report

Former Fed official Kocherlakota raises possibility that FOMC had a recent video conference to decide on a rate hike — Former Minneapolis Fed President Narayana Kocherlakota in a Bloomberg column on Tuesday raised the possibility that the FOMC may have held a secret, unscheduled meeting by video conference to discuss whether to raise interest rates at the official FOMC meeting next week. Mr. Kocherlakota is now back in the private sector as an economics professor at the University of Rochester.

We found it a little strange that Fed Chair Yellen last Friday essentially pre-announced a rate hike for next week, presupposing the votes of her colleagues. Her pre-announcement would make a lot more sense if she had already polled FOMC members in an unscheduled conference call in the past week or two. If there was such a meeting, Mr. Kocherlakota argues that the Fed should disclose its existence in the interests of transparency with at least a short public announcement.

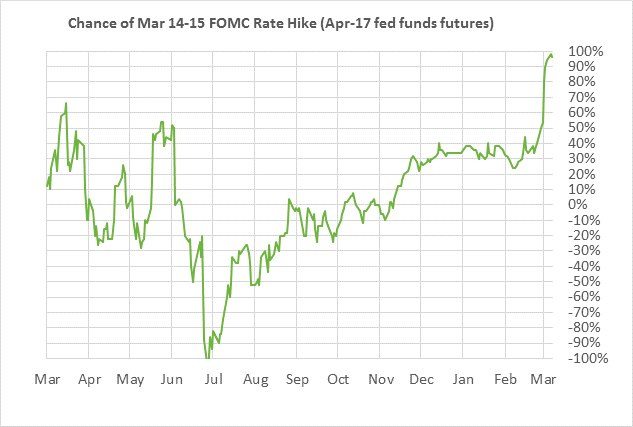

If Ms. Yellen did hold a video conference in the past week or two, she may have done so because she wanted to force market expectations higher for a rate hike at the March 14-15 meeting but first wanted to make sure she had votes for that rate hike. Market expectations for a March rate hike were at only 40% on Friday, Feb 24, and Ms. Yellen may have been concerned about springing a rate hike on the markets with expectations that low. In any case, Ms. Yellen and her associates last week were wildly successful in ramping up expectations for a rate hike next week to nearly 100%. Certainly, no one will be surprised when the Fed next week raises its funds rate target by 25 bp to 0.75%-1.00%.

ADP employment expected to show trend increase — The market is expecting today’s Feb ADP employment report to show an increase of +189,000, which happens to exactly match the 12-month trend increase for the series. ADP employment showed some volatility in the last two months by showing a weak +153,000 report in December followed by a strong +246,000 increase in January, producing a 2-month average of +200,000.

On the labor front, the market is mainly looking ahead to Friday’s Feb unemployment report, which is expected to show a solid +190,000 increase in payrolls following Jan’s strong report of +227,000. Friday’s Feb average hourly earnings report is expected to show an improvement to +2.8% y/y from +2.5% in Jan, thus matching the 7-1/2 year high of +2.8% posted on two recent occasions.

The consensus is for Friday’s Feb unemployment rate to fall -0.1 to 4.7%, leaving it only +0.1 point above the 9-3/4 year low of 4.6% posted in Nov 2016. The Jan unemployment rate of 4.8% was in line with the Fed’s long-term forecast for the unemployment rate, but still slightly above the FOMC’s forecast of 4.5% for 2017-2019.

Fed Chair Yellen last Friday said that a rate hike at next week’s FOMC meeting would “likely be appropriate” if the economic data evolves as the Fed expects. Given the relative certainty of that statement, it is not clear whether Friday’s payroll report could even be weak enough to dissuade the Fed from going ahead with next week’s rate hike.

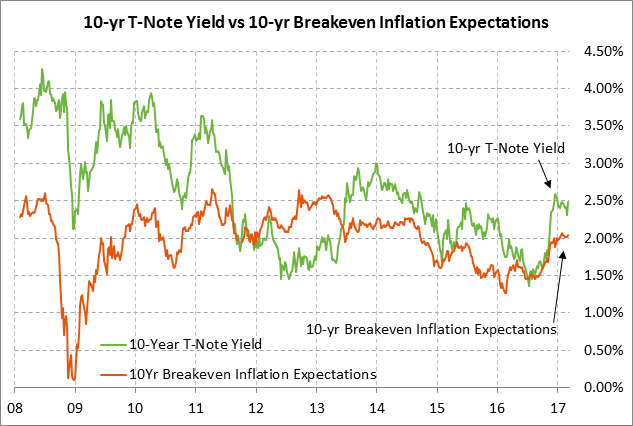

10-year T-note auction to yield near 2.53% — The Treasury today will sell $20 billion of 10-year T-notes in the first reopening of the 2-1/4% 10-year T-note of Feb 2017 first sold in February. The Treasury will then conclude this week’s $56 billion coupon package by selling $12 billion of reopened 30-year T-bonds on Thursday. Today’s 10-year T-note issue was trading at 2.53% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of 0.50% against the current 10-year breakeven inflation expectations rate of 2.03%.

The 12-auction averages for the 10-year are as follows: 2.48 bid cover ratio, $16 million in non-competitive bids, 5.1 bp tail to the median yield, 12.1 bp tail to the low yield, and 44% taken at the high yield. The 10-year T-note is the second most popular security behind the 10-year TIPS among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 63.4% of the last twelve 10-year T-note auctions, well above the average of 59.2% of all recent Treasury coupon auctions.

Tuesday’s 3-year T-note auction produced mildly disappointing results as investors apparently got cold feet ahead of next week’s FOMC meeting where the FOMC could adopt a more hawkish set of Fed dots. The auction yield of 1.630% was about 0.5 bp higher than expected and the bid cover ratio of 2.74 was weaker than the 12-auction average of 2.80. In addition, foreign bidding was weak with indirect bidders taking only 49.3% of the auction, below the 12-auction average of 51.4%.

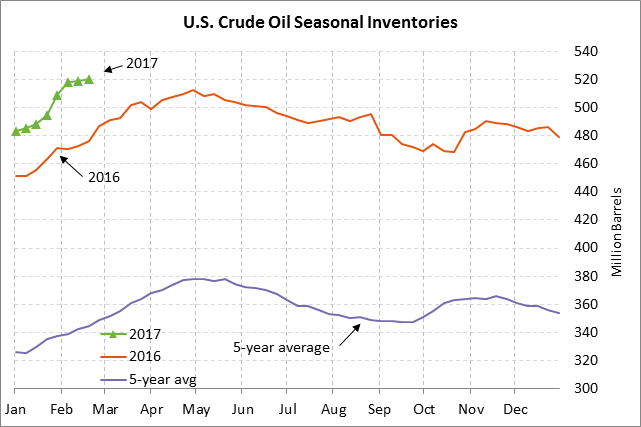

Weekly EIA report — The market consensus for today’s weekly EIA report is for a +1.4 million bbl rise in U.S. crude oil inventories, a -2.0 million bbl decline in gasoline inventories, a -1.0 million bbl decline in distillate inventories, and a +0.5 point rise in the refinery utilization rate to 86.5%. U.S. crude oil inventories remain in a massive glut at 38.7% above the 5-year seasonal average. Product inventories are ample with gasoline inventories at +7.9% above the 5-year seasonal average and with distillates at +23.6% above average.

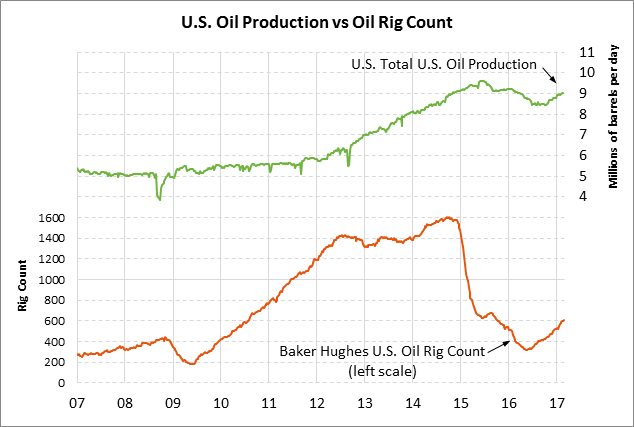

U.S. crude oil production in last week’s EIA report rose by +0.3% w/w to a new 1-year high of 9.032 million bpd. That was up by +604,000 bpd (+7.2%) from the 2-3/4 year low posted in July 2016. The number of active U.S. oil rigs has surged by +293 rigs (+93%) to a 1-1/2 year high of 609 rigs from the 7-1/2 year low of 316 rigs posted in May 2016.