- Tech stocks show continued weakness

- Betting odds rise to 95% for tax bill by Q1

- Congress moves toward passing a short-term CR to keep the government open past Friday

- U.S. ISM non-manufacturing index expected to remain strong

- U.S. trade deficit expected to widen

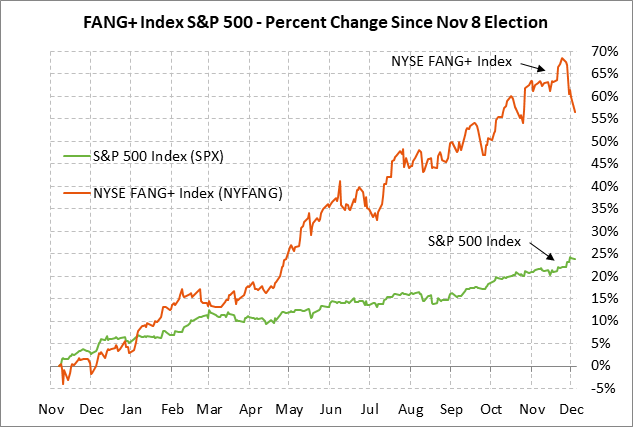

Tech stocks show continued weakness — Tech stocks on Monday showed continued weakness with the Nymex FANG+ index (a 10-stock index of FANG and similar stocks) closing the day sharply lower by -2.11%. The FANG+ index has now fallen by a total of -7.8% from last Tuesday’s record high and posted a new 5-week low on Monday. The Nasdaq 100 index on Monday closed -1.17%, much weaker than the -0.11% decline in the S&P 500 index.

Tech stocks have been hurt in the past week by (1) heavy year-end long liquidation pressure after this year’s run-up, (2) rotation out of tech stocks, which will receive a smaller tax benefit from tax reform relative to the higher-taxed industrial and financial sectors, and (3) the surprise news that the Senate last Friday night added a 20% corporate alternative minimum tax (AMT) to its tax bill, which would mean that corporations would not be able to obtain any benefit from popular tax deductions such as the R&D credit or write-offs for equipment spending and intellectual property.

The Senate appeared to make a drafting error in its tax bill since a 20% corporate AMT would make no sense with the corporate tax rate being cut to 20%. There is hope that the House’s tax bill will prevail on that issue since the House repealed the AMT altogether.

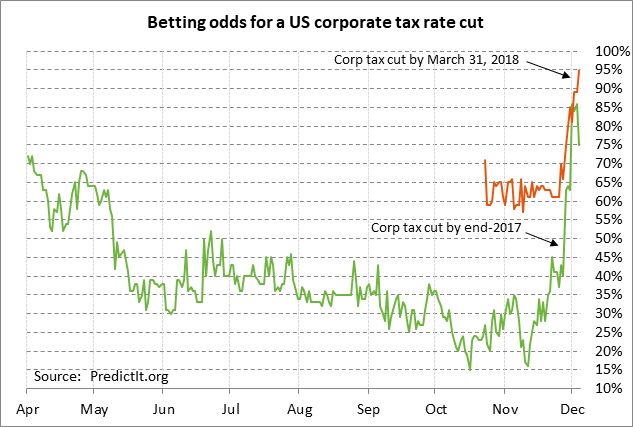

Betting odds rise to 95% for tax bill by Q1— The betting odds on Monday for Congress to approve a tax bill by March 31, 2018 rose by 6 points to a record 95%, according to PredictIt.com. Meanwhile, the betting odds for a tax deal by year-end remained high at 75%.

The House and Senate are in the process of naming members to a conference committee that will negotiate a compromise tax bill that will then be presented to both houses of Congress for their approval. However, the reality is that a small handful of House and Senate Republican leaders will privately drive the tax bill negotiations in a continuation of the way that the health care and tax bills have been handled thus far. The conference committee is simply for show since they will have little input into the final bill.

Republicans leaders now have only four weeks to get a bill passed if they want to meet their self-imposed deadline of having a bill on President Trump’s desk by the end of the year. The House and Senate originally planned to be in session only through the end of next week, but it now appears that Congress will have to remain in session through Dec 22 or even Dec 30 to address a new continuing resolution to keep the government open.

Congress moves toward passing a short-term CR to keep the government open past Friday — Congress appears to be moving towards easily passing a roll-over of the continuing resolution (CR) that expires this Friday night at midnight. Republican leaders originally intended to pass a CR this week that lasts until Dec 22. However, House Freedom Caucus members on Monday forced Speaker Ryan to consider a Dec 30 CR instead with their threat to vote against sending the tax bill to a conference with the Senate.

The fight will not be over this Friday’s CR, but rather over the second CR that will have to be passed by either Dec 22 or Dec 30. The government shut-down threat is therefore focused on late December rather than on this Friday.

This week’s CR will give Congressional leaders more time to come up with a spending deal for the rest of fiscal 2018. Pelosi/Schumer are scheduled to meet Thursday at the White House with President Trump and Ryan/McConnell to discuss how to handle year-end business including the 2-step CR process. Senate Majority Leader McConnell on Monday said that a budget deal could include disaster aid and a CHIP extension, but said that it would not include immigration issues such as a Dreamer fix. That means that the Democrats will have to decide by late-Dec whether they will threaten a government shutdown if they do not get a Dreamer fix.

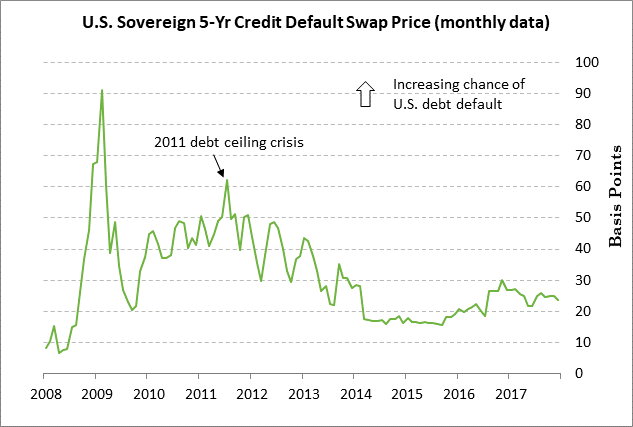

The threat of a government shutdown is not having any impact on the market’s perception of the U.S. credit quality since a shutdown would not risk a Treasury default. The current debt ceiling extension will expire this Friday, as well as the CR, but a new debt ceiling hike will not be necessary until spring 2018 since the Treasury can once again use emergency procedures to stay under the debt limit. The U.S. 5-year credit default swap (the price of insurance against a U.S. sovereign debt default) has moved sideways in a narrow range in recent months and was subdued at only 23.77 bp on Monday.

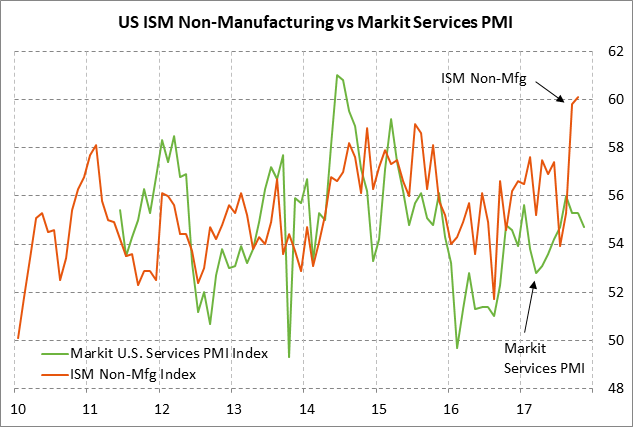

U.S. ISM non-manufacturing index expected to remain strong — The market consensus is for today’s Nov ISM non-manufacturing index to show a -1.1 point decline to 59.0. However, that decline would still leave the index in strong territory, just mildly below October’s 12-year high of 60.1. Business confidence remains strong due to (1) the 3% GDP growth seen in the past two quarters, (2) stronger overseas economic growth, and (3) expectations for tax cuts.

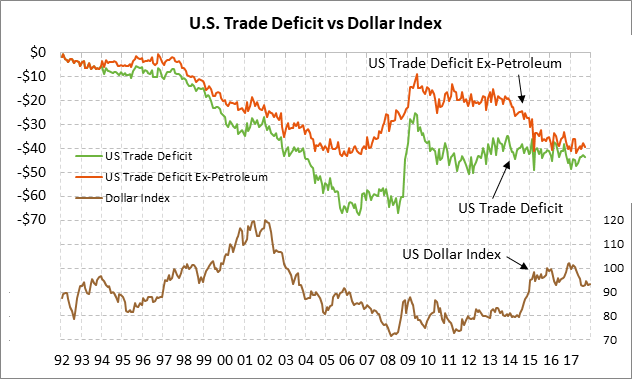

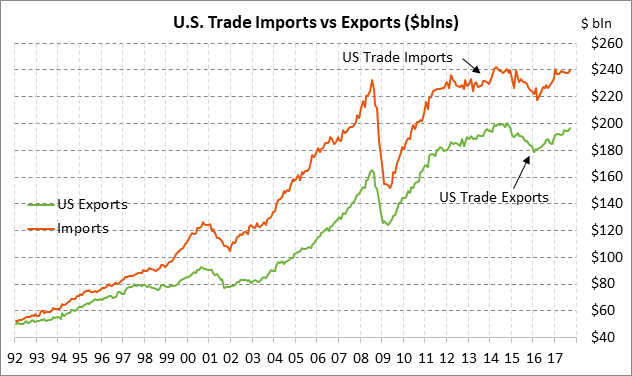

U.S. trade deficit expected to widen — The market consensus is for today’s Oct trade deficit report to widen moderately to -$47.4 billion from Sep’s -$43.5 billion. The expected report would push the deficit up to a 9-month high and leave it moderately wider than the 12-month trend average of -$44.9 billion. The deficit has been pushed higher in recent months by the increase in oil prices, which boosted the value of imported oil. Indeed, imports in September were up by +6.1% y/y, stronger than export growth of +4.6% y/y. A wider U.S. trade deficit would not be well-received at the White House and may increase the odds for protectionist trade measures.

Tech stocks show continued weakness — Tech stocks on Monday showed continued weakness with the Nymex FANG+ index (a 10-stock index of FANG and similar stocks) closing the day sharply lower by -2.11%. The FANG+ index has now fallen by a total of -7.8% from last Tuesday’s record high and posted a new 5-week low on Monday. The Nasdaq 100 index on Monday closed -1.17%, much weaker than the -0.11% decline in the S&P 500 index.

Tech stocks have been hurt in the past week by (1) heavy year-end long liquidation pressure after this year’s run-up, (2) rotation out of tech stocks, which will receive a smaller tax benefit from tax reform relative to the higher-taxed industrial and financial sectors, and (3) the surprise news that the Senate last Friday night added a 20% corporate alternative minimum tax (AMT) to its tax bill, which would mean that corporations would not be able to obtain any benefit from popular tax deductions such as the R&D credit or write-offs for equipment spending and intellectual property.

The Senate appeared to make a drafting error in its tax bill since a 20% corporate AMT would make no sense with the corporate tax rate being cut to 20%. There is hope that the House’s tax bill will prevail on that issue since the House repealed the AMT altogether.

Betting odds rise to 95% for tax bill by Q1— The betting odds on Monday for Congress to approve a tax bill by March 31, 2018 rose by 6 points to a record 95%, according to PredictIt.com. Meanwhile, the betting odds for a tax deal by year-end remained high at 75%.

The House and Senate are in the process of naming members to a conference committee that will negotiate a compromise tax bill that will then be presented to both houses of Congress for their approval. However, the reality is that a small handful of House and Senate Republican leaders will privately drive the tax bill negotiations in a continuation of the way that the health care and tax bills have been handled thus far. The conference committee is simply for show since they will have little input into the final bill.

Republicans leaders now have only four weeks to get a bill passed if they want to meet their self-imposed deadline of having a bill on President Trump’s desk by the end of the year. The House and Senate originally planned to be in session only through the end of next week, but it now appears that Congress will have to remain in session through Dec 22 or even Dec 30 to address a new continuing resolution to keep the government open.

Congress moves toward passing a short-term CR to keep the government open past Friday — Congress appears to be moving towards easily passing a roll-over of the continuing resolution (CR) that expires this Friday night at midnight. Republican leaders originally intended to pass a CR this week that lasts until Dec 22. However, House Freedom Caucus members on Monday forced Speaker Ryan to consider a Dec 30 CR instead with their threat to vote against sending the tax bill to a conference with the Senate.

The fight will not be over this Friday’s CR, but rather over the second CR that will have to be passed by either Dec 22 or Dec 30. The government shut-down threat is therefore focused on late December rather than on this Friday.

This week’s CR will give Congressional leaders more time to come up with a spending deal for the rest of fiscal 2018. Pelosi/Schumer are scheduled to meet Thursday at the White House with President Trump and Ryan/McConnell to discuss how to handle year-end business including the 2-step CR process. Senate Majority Leader McConnell on Monday said that a budget deal could include disaster aid and a CHIP extension, but said that it would not include immigration issues such as a Dreamer fix. That means that the Democrats will have to decide by late-Dec whether they will threaten a government shutdown if they do not get a Dreamer fix.

The threat of a government shutdown is not having any impact on the market’s perception of the U.S. credit quality since a shutdown would not risk a Treasury default. The current debt ceiling extension will expire this Friday, as well as the CR, but a new debt ceiling hike will not be necessary until spring 2018 since the Treasury can once again use emergency procedures to stay under the debt limit. The U.S. 5-year credit default swap (the price of insurance against a U.S. sovereign debt default) has moved sideways in a narrow range in recent months and was subdued at only 23.77 bp on Monday.

U.S. ISM non-manufacturing index expected to remain strong — The market consensus is for today’s Nov ISM non-manufacturing index to show a -1.1 point decline to 59.0. However, that decline would still leave the index in strong territory, just mildly below October’s 12-year high of 60.1. Business confidence remains strong due to (1) the 3% GDP growth seen in the past two quarters, (2) stronger overseas economic growth, and (3) expectations for tax cuts.

U.S. trade deficit expected to widen — The market consensus is for today’s Oct trade deficit report to widen moderately to -$47.4 billion from Sep’s -$43.5 billion. The expected report would push the deficit up to a 9-month high and leave it moderately wider than the 12-month trend average of -$44.9 billion. The deficit has been pushed higher in recent months by the increase in oil prices, which boosted the value of imported oil. Indeed, imports in September were up by +6.1% y/y, stronger than export growth of +4.6% y/y. A wider U.S. trade deficit would not be well-received at the White House and may increase the odds for protectionist trade measures.