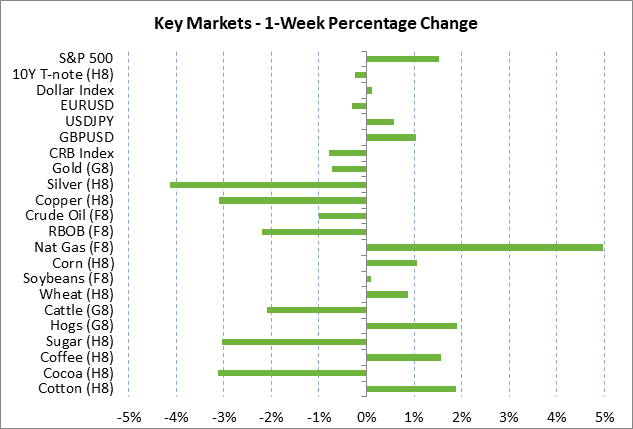

- Global market focus

- U.S. markets key on whether the Senate-House will be able to agree on a compromise tax bill

- Congress must approve a new CR by Friday to prevent a government shutdown

- U.S. markets shaken up by Flynn news

Global market focus — U.S. market attention this week will focus on (1) whether the House and Senate can iron out a common version of tax reform that can then pass both houses of Congress, (2) whether there will be a U.S. government shutdown this coming Friday night when the current continuing resolution expires, (3) anticipation of next week’s FOMC meeting where the market is discounting a 100% chance of a rate hike, (4) this week’s busy U.S. economic schedule, which is capped by Friday’s Nov payroll report (expected +200,000), and (5) whether oil prices can show any further gains this week after OPEC and non-OPEC producers last Thursday extended their production cut agreement by nine months until the end of 2018.

The European markets this week will closely follow Brexit negotiations as well as the ongoing efforts in Germany to form a government. German Chancellor Merkel’s CDU/CSU bloc this week will continue talks with Social Democrats to see if they can form a new grand coalition government. If not, then new German elections will have to be called.

Meanwhile, UK Prime Minister May today is due to meet with European Commission President Junker and deliver the UK’s proposal for the key divorce issues that must be resolved before the EU will move on to discussing a trade deal with the UK. There was substantial progress last week after reports that a provisional deal was reached on a Brexit divorce bill payment range. That progress sparked some strength in sterling and a sharp rise in UK gilt yields on the increased chance for a BOE rate hike in the latter half of 2018 if a final Brexit trade deal can be reached.

In China, the markets will continue to closely watch the government’s deleveraging campaign and the Chinese bond market. The Chinese government last Friday imposed new rules on mutual funds for investing in Hong Kong stocks and also put new restrictions on micro-loan lenders. In some good news for the Chinese markets, the Chinese 10-year bond yield last week closed moderately lower by -5.2 bp at 3.92%, which was well below the recent 3-year high of 4.035% (Nov 22). Nevertheless, Chinese stocks last week traded on the defensive and the Shanghai Composite closed the week down -1.08%, just above last Tuesday’s 3-1/4 month low.

U.S. markets key on whether the Senate-House will be able to agree on a compromise tax bill — The Senate late last Friday night passed a tax reform bill by a margin of 51-49, with Nebraska Senator Corker being the only Republican Senator who voted against the bill. That means that Senator Mitch McConnell can afford to lose only one more Senator on a compromise bill with the House. The House will mostly have to agree with the Senate bill since the Republican majority is so thin in the Senate and because the Senate must follow the arcane reconciliation rules to get the bill past the Senate parliamentarian.

Mr. McConnell and House Speaker Ryan early this week are expected to appoint members to a conference committee so they can quickly get started on ironing out a compromise bill. Republicans have only three weeks to get a bill passed if they want to meet their self-imposed deadline of having a bill on President Trump’s desk by the end of the year. The House and Senate originally planned to be in session only through the end of next week, then recessing for the rest of December for the holidays. However, it now appears likely that Congress will remain in session at least through Dec 22 in order to try to get a tax deal done and also to push through a new continuing resolution to keep the government open.

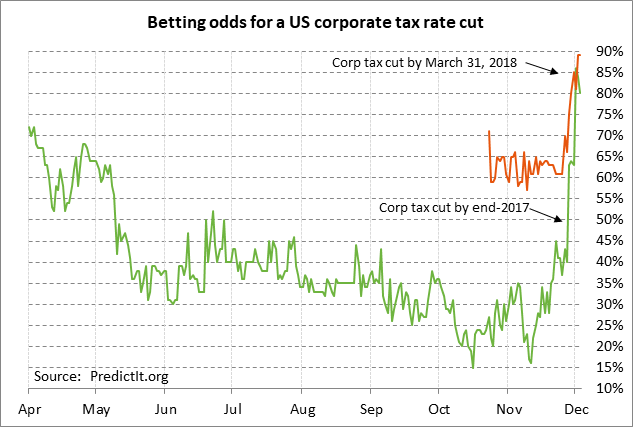

While there will undoubtedly be ups and downs over the next 2-3 weeks while Republicans work on a common tax bill, we continue to expect Republicans to find a bill that they can push through both houses of Congress since passing a tax reform bill has virtually become an existential issue for Republicans. The betting odds now heavily favor a deal getting done. The betting odds on Sunday evening were at 80% for a corporate tax cut by year-end and at 89% for a tax cut by March 31, 2018, according to PredictIt.org.

Congress must approve a new CR by Friday to prevent a government shutdown — The U.S. government faces a partial shutdown this coming Friday night at midnight if Congress cannot approve new spending authority in time to replace the expiring continuing resolution (CR).

Republican leaders over the weekend announced a plan for Congress this week to approve a new CR that will last through Dec 22, just before the Christmas holiday. Congress by Dec 22 would then have to approve another CR that would contain the actual spending levels for the remainder of the fiscal year and possibly address Democratic demands for a Dreamer solution. The Dec 22 CR would last until some time in January and would give committees time to write appropriations bills. Congress in January could then approve the actual spending bills for the remainder of 2018 that were agreed to in the Dec 22 CR.

U.S. markets shaken up by Flynn news — The U.S. stock market last Friday saw sharp intra-day losses and T-note prices rallied after news of a plea deal for former National Security Director Flynn, which indicated that the Mueller investigation has reached the top levels of the White House. The markets were mainly concerned that the Flynn news might damage the chances of a tax deal. However, the stock market this week should receive some underlying support from the Senate’s passage of the tax bill late last Friday night. The U.S. markets this week will mainly be focused on the tax bill and on Friday’s payroll report. The stock market will also be carefully watching tech stocks, which had a rocky ride last week that caused relative weakness in the Nasdaq 100 against the S&P 500 index.

Global market focus — U.S. market attention this week will focus on (1) whether the House and Senate can iron out a common version of tax reform that can then pass both houses of Congress, (2) whether there will be a U.S. government shutdown this coming Friday night when the current continuing resolution expires, (3) anticipation of next week’s FOMC meeting where the market is discounting a 100% chance of a rate hike, (4) this week’s busy U.S. economic schedule, which is capped by Friday’s Nov payroll report (expected +200,000), and (5) whether oil prices can show any further gains this week after OPEC and non-OPEC producers last Thursday extended their production cut agreement by nine months until the end of 2018.

The European markets this week will closely follow Brexit negotiations as well as the ongoing efforts in Germany to form a government. German Chancellor Merkel’s CDU/CSU bloc this week will continue talks with Social Democrats to see if they can form a new grand coalition government. If not, then new German elections will have to be called.

Meanwhile, UK Prime Minister May today is due to meet with European Commission President Junker and deliver the UK’s proposal for the key divorce issues that must be resolved before the EU will move on to discussing a trade deal with the UK. There was substantial progress last week after reports that a provisional deal was reached on a Brexit divorce bill payment range. That progress sparked some strength in sterling and a sharp rise in UK gilt yields on the increased chance for a BOE rate hike in the latter half of 2018 if a final Brexit trade deal can be reached.

In China, the markets will continue to closely watch the government’s deleveraging campaign and the Chinese bond market. The Chinese government last Friday imposed new rules on mutual funds for investing in Hong Kong stocks and also put new restrictions on micro-loan lenders. In some good news for the Chinese markets, the Chinese 10-year bond yield last week closed moderately lower by -5.2 bp at 3.92%, which was well below the recent 3-year high of 4.035% (Nov 22). Nevertheless, Chinese stocks last week traded on the defensive and the Shanghai Composite closed the week down -1.08%, just above last Tuesday’s 3-1/4 month low.

U.S. markets key on whether the Senate-House will be able to agree on a compromise tax bill — The Senate late last Friday night passed a tax reform bill by a margin of 51-49, with Nebraska Senator Corker being the only Republican Senator who voted against the bill. That means that Senator Mitch McConnell can afford to lose only one more Senator on a compromise bill with the House. The House will mostly have to agree with the Senate bill since the Republican majority is so thin in the Senate and because the Senate must follow the arcane reconciliation rules to get the bill past the Senate parliamentarian.

Mr. McConnell and House Speaker Ryan early this week are expected to appoint members to a conference committee so they can quickly get started on ironing out a compromise bill. Republicans have only three weeks to get a bill passed if they want to meet their self-imposed deadline of having a bill on President Trump’s desk by the end of the year. The House and Senate originally planned to be in session only through the end of next week, then recessing for the rest of December for the holidays. However, it now appears likely that Congress will remain in session at least through Dec 22 in order to try to get a tax deal done and also to push through a new continuing resolution to keep the government open.

While there will undoubtedly be ups and downs over the next 2-3 weeks while Republicans work on a common tax bill, we continue to expect Republicans to find a bill that they can push through both houses of Congress since passing a tax reform bill has virtually become an existential issue for Republicans. The betting odds now heavily favor a deal getting done. The betting odds on Sunday evening were at 80% for a corporate tax cut by year-end and at 89% for a tax cut by March 31, 2018, according to PredictIt.org.

Congress must approve a new CR by Friday to prevent a government shutdown — The U.S. government faces a partial shutdown this coming Friday night at midnight if Congress cannot approve new spending authority in time to replace the expiring continuing resolution (CR).

Republican leaders over the weekend announced a plan for Congress this week to approve a new CR that will last through Dec 22, just before the Christmas holiday. Congress by Dec 22 would then have to approve another CR that would contain the actual spending levels for the remainder of the fiscal year and possibly address Democratic demands for a Dreamer solution. The Dec 22 CR would last until some time in January and would give committees time to write appropriations bills. Congress in January could then approve the actual spending bills for the remainder of 2018 that were agreed to in the Dec 22 CR.

U.S. markets shaken up by Flynn news — The U.S. stock market last Friday saw sharp intra-day losses and T-note prices rallied after news of a plea deal for former National Security Director Flynn, which indicated that the Mueller investigation has reached the top levels of the White House. The markets were mainly concerned that the Flynn news might damage the chances of a tax deal. However, the stock market this week should receive some underlying support from the Senate’s passage of the tax bill late last Friday night. The U.S. markets this week will mainly be focused on the tax bill and on Friday’s payroll report. The stock market will also be carefully watching tech stocks, which had a rocky ride last week that caused relative weakness in the Nasdaq 100 against the S&P 500 index.

Global market focus — U.S. market attention this week will focus on (1) whether the House and Senate can iron out a common version of tax reform that can then pass both houses of Congress, (2) whether there will be a U.S. government shutdown this coming Friday night when the current continuing resolution expires, (3) anticipation of next week’s FOMC meeting where the market is discounting a 100% chance of a rate hike, (4) this week’s busy U.S. economic schedule, which is capped by Friday’s Nov payroll report (expected +200,000), and (5) whether oil prices can show any further gains this week after OPEC and non-OPEC producers last Thursday extended their production cut agreement by nine months until the end of 2018.

The European markets this week will closely follow Brexit negotiations as well as the ongoing efforts in Germany to form a government. German Chancellor Merkel’s CDU/CSU bloc this week will continue talks with Social Democrats to see if they can form a new grand coalition government. If not, then new German elections will have to be called.

Meanwhile, UK Prime Minister May today is due to meet with European Commission President Junker and deliver the UK’s proposal for the key divorce issues that must be resolved before the EU will move on to discussing a trade deal with the UK. There was substantial progress last week after reports that a provisional deal was reached on a Brexit divorce bill payment range. That progress sparked some strength in sterling and a sharp rise in UK gilt yields on the increased chance for a BOE rate hike in the latter half of 2018 if a final Brexit trade deal can be reached.

In China, the markets will continue to closely watch the government’s deleveraging campaign and the Chinese bond market. The Chinese government last Friday imposed new rules on mutual funds for investing in Hong Kong stocks and also put new restrictions on micro-loan lenders. In some good news for the Chinese markets, the Chinese 10-year bond yield last week closed moderately lower by -5.2 bp at 3.92%, which was well below the recent 3-year high of 4.035% (Nov 22). Nevertheless, Chinese stocks last week traded on the defensive and the Shanghai Composite closed the week down -1.08%, just above last Tuesday’s 3-1/4 month low.

U.S. markets key on whether the Senate-House will be able to agree on a compromise tax bill — The Senate late last Friday night passed a tax reform bill by a margin of 51-49, with Nebraska Senator Corker being the only Republican Senator who voted against the bill. That means that Senator Mitch McConnell can afford to lose only one more Senator on a compromise bill with the House. The House will mostly have to agree with the Senate bill since the Republican majority is so thin in the Senate and because the Senate must follow the arcane reconciliation rules to get the bill past the Senate parliamentarian.

Mr. McConnell and House Speaker Ryan early this week are expected to appoint members to a conference committee so they can quickly get started on ironing out a compromise bill. Republicans have only three weeks to get a bill passed if they want to meet their self-imposed deadline of having a bill on President Trump’s desk by the end of the year. The House and Senate originally planned to be in session only through the end of next week, then recessing for the rest of December for the holidays. However, it now appears likely that Congress will remain in session at least through Dec 22 in order to try to get a tax deal done and also to push through a new continuing resolution to keep the government open.

While there will undoubtedly be ups and downs over the next 2-3 weeks while Republicans work on a common tax bill, we continue to expect Republicans to find a bill that they can push through both houses of Congress since passing a tax reform bill has virtually become an existential issue for Republicans. The betting odds now heavily favor a deal getting done. The betting odds on Sunday evening were at 80% for a corporate tax cut by year-end and at 89% for a tax cut by March 31, 2018, according to PredictIt.org.

Congress must approve a new CR by Friday to prevent a government shutdown — The U.S. government faces a partial shutdown this coming Friday night at midnight if Congress cannot approve new spending authority in time to replace the expiring continuing resolution (CR).

Republican leaders over the weekend announced a plan for Congress this week to approve a new CR that will last through Dec 22, just before the Christmas holiday. Congress by Dec 22 would then have to approve another CR that would contain the actual spending levels for the remainder of the fiscal year and possibly address Democratic demands for a Dreamer solution. The Dec 22 CR would last until some time in January and would give committees time to write appropriations bills. Congress in January could then approve the actual spending bills for the remainder of 2018 that were agreed to in the Dec 22 CR.

U.S. markets shaken up by Flynn news — The U.S. stock market last Friday saw sharp intra-day losses and T-note prices rallied after news of a plea deal for former National Security Director Flynn, which indicated that the Mueller investigation has reached the top levels of the White House. The markets were mainly concerned that the Flynn news might damage the chances of a tax deal. However, the stock market this week should receive some underlying support from the Senate’s passage of the tax bill late last Friday night. The U.S. markets this week will mainly be focused on the tax bill and on Friday’s payroll report. The stock market will also be carefully watching tech stocks, which had a rocky ride last week that caused relative weakness in the Nasdaq 100 against the S&P 500 index.