- Global bond yields rise on a confluence of bearish factors

- Senate tax bill is making progress as a vote is expected either Thursday or Friday

- Markets await production-cut decision at today’s OPEC/non-OPEC meeting

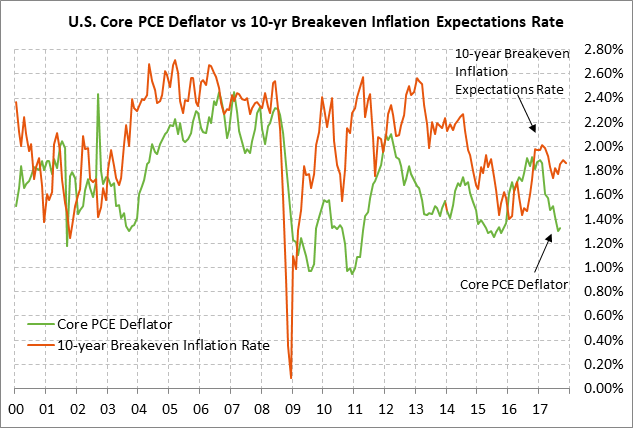

- Core PCE deflator expected to tick higher

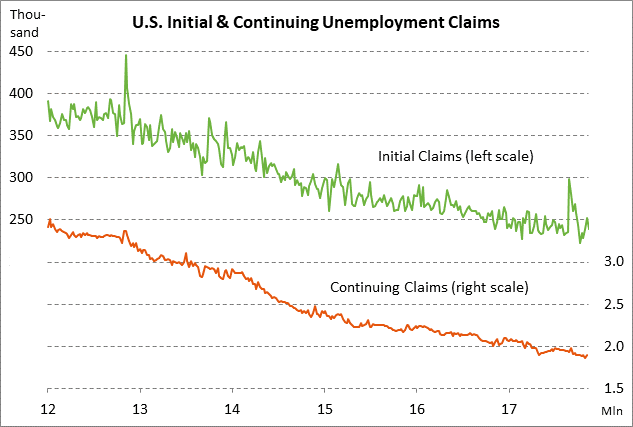

- Claims expected to remain favorable

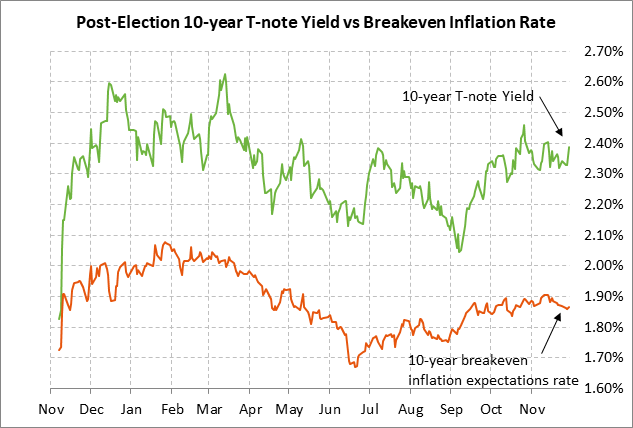

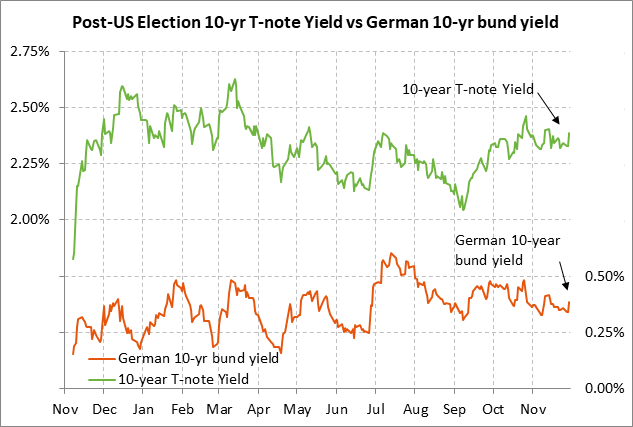

Global bond yields rise on a confluence of bearish factors — The 10-year T-note yield on Wednesday rose to a new 2-week high and closed sharply higher by +5.9 bp at 2.386%. European bond yields rose as well with the 10-year German bund yield rising by +4.6 bp to 0.385% and the 10-year UK gilt rising by +8.5 bp to a 2-1/2 week high of 1.337%.

U.S. T-note yields were pushed sharply higher by several bearish factors: (1) Fed Chair Yellen’s comment that the U.S. economic expansion is broadening as well as the stronger-than-expected upward revision in U.S. Q3 GDP to +3.3% from +3.0%, (2) increased inflation concerns after Ms. Yellen reiterated her view that the soft inflation statistics are transitory and after the Fed’s Beige Book said that “price pressures have strengthened since the last report” (the 10-year breakeven rate on Wed closed +0.6 bp at 1.866%), (3) Ms. Yellen’s comment that she is worried about the upward trajectory of the U.S. debt-to-GDP ratio, which would worsen under the Republican tax reform bill and would mean increased Treasury security supply in coming years, and (4) the substantially higher odds that the Senate will pass its tax bill by Friday.

Meanwhile, the German 10-year bund yield was boosted by the rise in U.S. T-note yields and also by the rise in the German Nov CPI to +1.8% y/y from Oct’s +1.6%m, stronger than expectations of +1.7%. The UK 10-year gilt yield rose sharply on increased expectations for another BOE rate hike after news that the UK and EU are close to an agreement in principle on Brexit divorce issues, which may allow talks to move ahead to a trade deal. The markets on Wednesday accelerated expectations for the BOE’s next rate hike to September from December 2018. The BOE may need to raise rates again to address the inflation pressures that have been caused by the post-Brexit weakness in sterling.

UK Prime Minister May is scheduled to present her formal divorce offer this coming Monday at a lunch with European Commission President Jean-Claude Juncker. Monday’s offer would give national governments some time to consider the offer and announce a decision at the EU Summit in two weeks on Dec 14 as to whether the UK-EU can move on to trade talks.

Senate tax bill is making progress as a vote is expected either Thursday or Friday — The Senate’s tax bill made progress on Wednesday after the Senate voted to open floor debate. Senate Majority Leader McConnell plans to have a vote-a-rama starting on Thursday when Senators can offer and vote on amendments, concluding with a vote on the final bill. Senate Majority Whip Cornyn says he thinks Republicans have the votes to pass the bill.

Mr. McConnell seems to be effectively picking off the holdouts one by one with changes in the legislation. The most contentious issue at this point is Senator Corker’s request for a trigger for tax hikes down the road if the bill bloats the budget deficit beyond expectations. Conservatives and even moderate Senators are generally opposed to that idea. However, there may be some language by which Mr. Corker can claim victory without any hard triggers actually being put into the legislation.

Meanwhile, Maine’s Senator Susan Collins now seems ready to support the bill, which contains a repeal of the Obamacare mandate, after she received a promise from President Trump and Mr. McConnell that they will support the bipartisan package of Obamacare fixes. Senator McCain, who deep-sixed the Obamacare repeal, has yet to say whether he will support the bill and remains a wildcard.

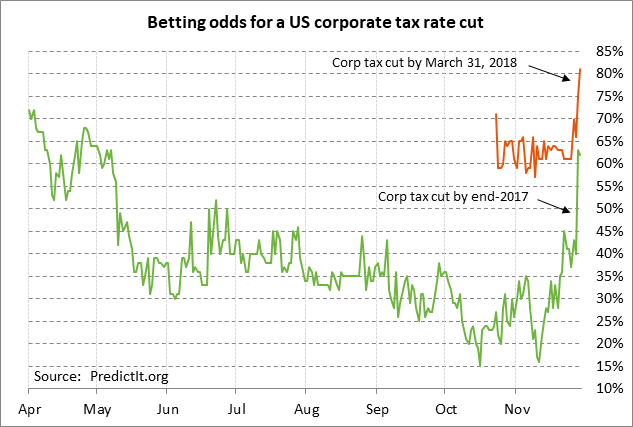

The betting odds late Wednesday for a corporate tax cut by year-end fell -1 point to 62% from Tuesday’s record high of 63%. The odds for a tax cut by March 31, 2018, rose by another +6 points to a record high of 81%, illustrating that market expectations for a deal are now strong.

Markets await production-cut decision at today’s OPEC/non-OPEC meeting — OPEC members have already agreed to extend their production cut by 9 months to the end of 2018, but are now waiting on Russia for its decision. Russia seems willing to go along with the 9-month extension if there is some certainty about what happens after the 9-month extension concludes.

Any decision today that amounts to less than a 9-month extension would likely result in a sharp sell-off in oil prices. Moreover, it remains to be seen how much of a boost in crude oil prices there might be if the 9-month extension goes through because the market has already largely discounted that outcome. It is possible, therefore, that there will be little sustainable upside for crude oil prices regardless of the OPEC/non-OPEC decision.

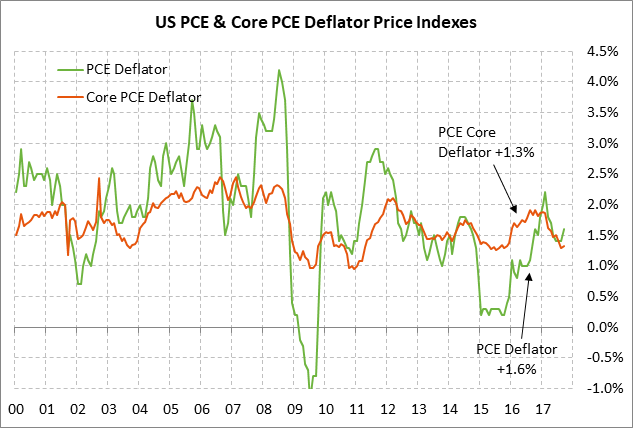

Core PCE deflator expected to tick higher — The consensus is for the Oct core PCE deflator to tick higher to +1.4% y/y from Sep’s +1.3%, but for the headline deflator to ease to +1.5% y/y from Sep’s +1.6%. The expected Oct core deflator of +1.4% y/y would still be well below the Fed’s +2.0% target. However, Fed Chair Yellen on Wednesday reiterated her view that the soft inflation statistics are only transitory.

Claims expected to remain favorable — The market consensus is for today’s weekly initial unemployment claims report to show a small +1,000 increase to 240,000 (after last week’s -13,000 to 239,000) and for continuing claims to show a -14,000 decline to 1.890 million (after last week’s +36,000 to 1.904 million). The claims series remains in good shape with initial claims at only +16,000 above Oct’s 44-3/4 year low of 223,000 and continuing claims at only +36,000 above early-Nov’s 44-year low of 1.868 million.

Global bond yields rise on a confluence of bearish factors — The 10-year T-note yield on Wednesday rose to a new 2-week high and closed sharply higher by +5.9 bp at 2.386%. European bond yields rose as well with the 10-year German bund yield rising by +4.6 bp to 0.385% and the 10-year UK gilt rising by +8.5 bp to a 2-1/2 week high of 1.337%.

U.S. T-note yields were pushed sharply higher by several bearish factors: (1) Fed Chair Yellen’s comment that the U.S. economic expansion is broadening as well as the stronger-than-expected upward revision in U.S. Q3 GDP to +3.3% from +3.0%, (2) increased inflation concerns after Ms. Yellen reiterated her view that the soft inflation statistics are transitory and after the Fed’s Beige Book said that “price pressures have strengthened since the last report” (the 10-year breakeven rate on Wed closed +0.6 bp at 1.866%), (3) Ms. Yellen’s comment that she is worried about the upward trajectory of the U.S. debt-to-GDP ratio, which would worsen under the Republican tax reform bill and would mean increased Treasury security supply in coming years, and (4) the substantially higher odds that the Senate will pass its tax bill by Friday.

Meanwhile, the German 10-year bund yield was boosted by the rise in U.S. T-note yields and also by the rise in the German Nov CPI to +1.8% y/y from Oct’s +1.6%m, stronger than expectations of +1.7%. The UK 10-year gilt yield rose sharply on increased expectations for another BOE rate hike after news that the UK and EU are close to an agreement in principle on Brexit divorce issues, which may allow talks to move ahead to a trade deal. The markets on Wednesday accelerated expectations for the BOE’s next rate hike to September from December 2018. The BOE may need to raise rates again to address the inflation pressures that have been caused by the post-Brexit weakness in sterling.

UK Prime Minister May is scheduled to present her formal divorce offer this coming Monday at a lunch with European Commission President Jean-Claude Juncker. Monday’s offer would give national governments some time to consider the offer and announce a decision at the EU Summit in two weeks on Dec 14 as to whether the UK-EU can move on to trade talks.

Senate tax bill is making progress as a vote is expected either Thursday or Friday — The Senate’s tax bill made progress on Wednesday after the Senate voted to open floor debate. Senate Majority Leader McConnell plans to have a vote-a-rama starting on Thursday when Senators can offer and vote on amendments, concluding with a vote on the final bill. Senate Majority Whip Cornyn says he thinks Republicans have the votes to pass the bill.

Mr. McConnell seems to be effectively picking off the holdouts one by one with changes in the legislation. The most contentious issue at this point is Senator Corker’s request for a trigger for tax hikes down the road if the bill bloats the budget deficit beyond expectations. Conservatives and even moderate Senators are generally opposed to that idea. However, there may be some language by which Mr. Corker can claim victory without any hard triggers actually being put into the legislation.

Meanwhile, Maine’s Senator Susan Collins now seems ready to support the bill, which contains a repeal of the Obamacare mandate, after she received a promise from President Trump and Mr. McConnell that they will support the bipartisan package of Obamacare fixes. Senator McCain, who deep-sixed the Obamacare repeal, has yet to say whether he will support the bill and remains a wildcard.

The betting odds late Wednesday for a corporate tax cut by year-end fell -1 point to 62% from Tuesday’s record high of 63%. The odds for a tax cut by March 31, 2018, rose by another +6 points to a record high of 81%, illustrating that market expectations for a deal are now strong.

Markets await production-cut decision at today’s OPEC/non-OPEC meeting — OPEC members have already agreed to extend their production cut by 9 months to the end of 2018, but are now waiting on Russia for its decision. Russia seems willing to go along with the 9-month extension if there is some certainty about what happens after the 9-month extension concludes.

Any decision today that amounts to less than a 9-month extension would likely result in a sharp sell-off in oil prices. Moreover, it remains to be seen how much of a boost in crude oil prices there might be if the 9-month extension goes through because the market has already largely discounted that outcome. It is possible, therefore, that there will be little sustainable upside for crude oil prices regardless of the OPEC/non-OPEC decision.

Core PCE deflator expected to tick higher — The consensus is for the Oct core PCE deflator to tick higher to +1.4% y/y from Sep’s +1.3%, but for the headline deflator to ease to +1.5% y/y from Sep’s +1.6%. The expected Oct core deflator of +1.4% y/y would still be well below the Fed’s +2.0% target. However, Fed Chair Yellen on Wednesday reiterated her view that the soft inflation statistics are only transitory.

Claims expected to remain favorable — The market consensus is for today’s weekly initial unemployment claims report to show a small +1,000 increase to 240,000 (after last week’s -13,000 to 239,000) and for continuing claims to show a -14,000 decline to 1.890 million (after last week’s +36,000 to 1.904 million). The claims series remains in good shape with initial claims at only +16,000 above Oct’s 44-3/4 year low of 223,000 and continuing claims at only +36,000 above early-Nov’s 44-year low of 1.868 million.