- U.S. home prices expected to remain strong

- U.S. consumer confidence expected to fall back from Oct’s 16-3/4 year high but remain strong

- Powell Fed era begins

- Odds for tax bill passage by March 2018 jump to 70%

- 7-year T-note auction to yield near 2.22%

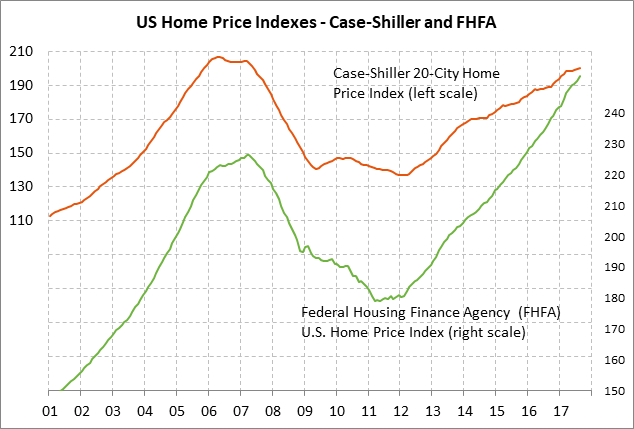

U.S. home prices expected to remain strong — Today’s home price reports are expected to show continued strength in home prices due to both strong demand and tight supplies. The October existing home sales level of 5.48 million units was only -4% below the 10-year high of 5.70 million units posted back in March, illustrating strong home demand. Meanwhile, the supply of homes available for sale remains tight at 4.9 months, which is well below the long-term average of 7.0 months and the 7-8 month level that the National Association of Realtors says is consistent with stable home prices. Home prices should rise further in coming months as strong demand and tight supply conditions continue.

The consensus is for today’s Sep FHFA house price index to show a +0.5% m/m increase, adding to Aug’s +0.7% increase. Meanwhile, the consensus is for today’s Sep S&P CoreLogic composite-20 home price index to show a +0.3% m/m increase, adding to Aug’s +0.45% increase.

The broader FHFA index has risen sharply by +6.6% on a year-on-year basis and by a total of +41% from its housing-bust trough. Meanwhile, the Composite-20 index of metropolitan homes has risen sharply by +6.0% y/y and by +46% from its housing-bust low.

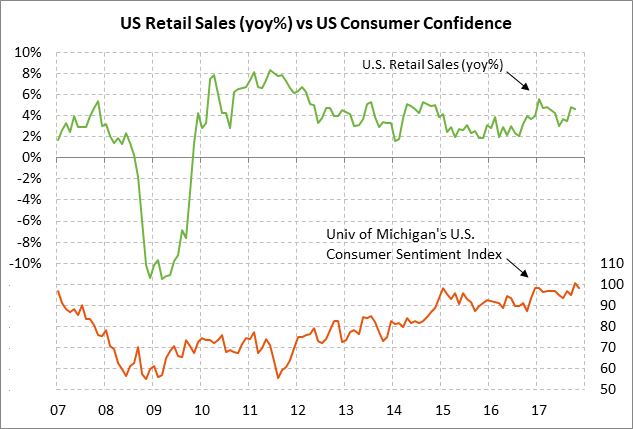

U.S. consumer confidence expected to fall back from Oct’s 16-3/4 year high but remain strong — The market is expecting today’s Nov Conference Board U.S. consumer confidence index to show a -1.9 point decline to 124.0, giving back part of October’s +5.3 point surge to a new 16-3/4 year high of 125.9. Expectations for a modest decline in today’s report are supported by the already-reported news that the University of Michigan’s U.S. consumer confidence index in November fell by -2.2 points to 98.5 from Oct’s 13-3/4 year high of 100.7.

U.S. consumer confidence remains very strong due to (1) record highs in the stock market, (2) improving household wealth with the rising stock market and real estate market, (3) the strong labor market, which gives consumers more confidence about job security, and (4) rising income levels. Negative factors for consumer sentiment include (1) Washington political uncertainty, (2) geopolitical worries such as North Korea, and (3) the 50 cent/gallon rise in gasoline prices in the past 5 months.

Powell Fed era begins — Jerome Powell will appear today before the Senate Banking Committee for his nomination hearing to become the new Fed Chair. Since Mr. Powell is currently a Fed Governor, he is in the somewhat awkward position of being under pressure to reiterate the Fed’s usual themes today while also being asked what he might do differently as Fed Chair. The market suspects that there is actually not much daylight between Mr. Powell and the Fed’s current stance, which means he might sound a lot like Ms. Yellen today when talking about the economy and monetary policy. The markets today will also start adjusting to Mr. Powell’s style as the new “explainer-in-chief” for monetary policy, which hopefully does not include any random surprises or gaffs.

Odds for tax bill passage by March 2018 jump to 70% — President Trump is scheduled to meet today with Senate Republicans to pressure them into passing a tax bill. Mr. Trump is also scheduled to meet with Congressional leaders (Ryan, Pelosi, McConnell, Schumer) about the need for a spending bill to keep the government open when the current continuing resolution (CR) expires next Friday (Dec 8).

Congress will likely be forced to approve a short-term CR to delay the deadline for a spending bill until either late December or January. Republicans are sprinting toward trying to get a tax bill passed and have not had time to focus on a spending bill. The spending bill will require some Democratic support to pass and is expected to run into some serious obstacles.

The full Senate is expected to vote on a tax bill by this Thursday. If the Senate passes the bill, then the House and Senate will then have to see if they can find a compromise bill that can pass both houses of Congress. We continue to expect Congress to approve a tax cut since it has become nearly an existential issue for the Republican party.

The betting odds late Monday afternoon of 44% for a corporate tax cut by year-end were just -1 point below last Wednesday’s 4-month high of 45%. The odds of a corporate tax cut by March 31, 2018 have jumped to 70% due to the Senate’s progress on the bill.

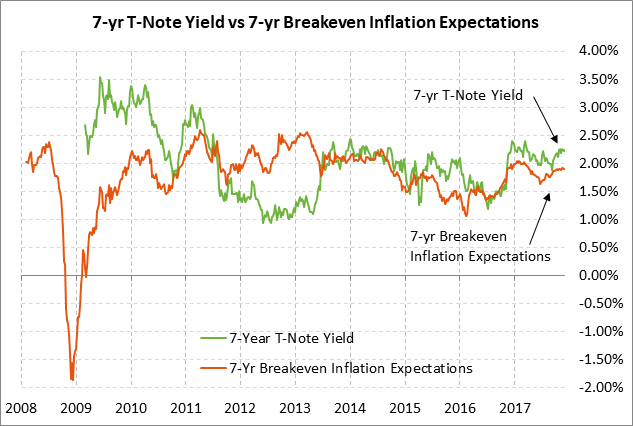

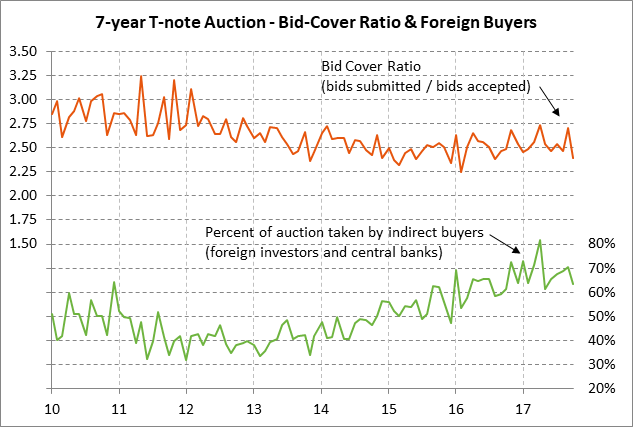

7-year T-note auction to yield near 2.22% — The Treasury today will sell $28 billion of 7-year T-notes, concluding this week’s $88 billion T-note package. Today’s 7-year T-note issue was trading at 2.23% in when-issued trading late Monday afternoon. That translates to an inflation-adjusted yield of 0.34% against the current 7-year breakeven rate of 1.89%.

The 12-auction averages for the 7-year are as follows: 2.55 bid cover ratio, $12 million in non-competitive bids, 4.5 bp tail to the median yield, 20.3 bp tail to the low yield, and 42% taken at the high yield. The 7-year is the second most popular coupon security among foreign investors and central banks, behind the 30-year TIPS. Indirect bidders, a proxy for foreign buying, have taken an average of 68.6% of the last twelve 7-year T-note auctions, well above the average of 61.8% for all recent Treasury coupon auctions.