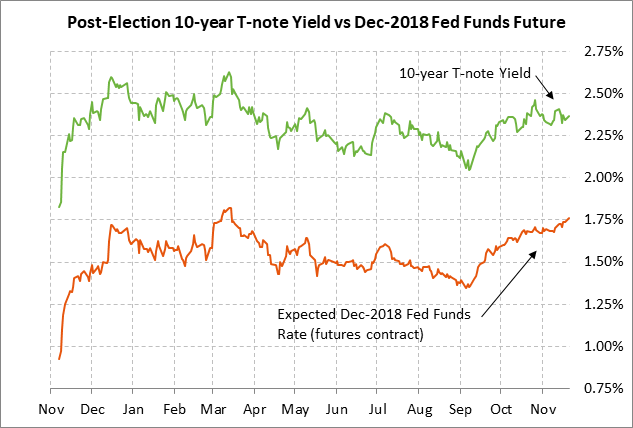

- Yellen’s resignation has no real impact on 2018 Fed policy outlook

- Germany appears to be slipping towards new elections

- U.S. home sales expected to remain steady after hurricane disruptions

Yellen’s resignation has no real impact on 2018 Fed policy outlook — Fed Chair Janet Yellen on Monday announced that she would step down, not only as Fed Chair when Jerome Powell is sworn in as the new Fed Chair, but also from her Fed Governor term, which lasts until 2024. If she so chose, Ms. Yellen could have stayed at the Fed as a Governor until her term expired in 2024.

However, we fully expected Ms. Yellen to step down as a courtesy to Jerome Powell so that he has full rein to take over as the new Fed Chair without Ms. Yellen’s influence lurking in the background, potentially as an undermining force. We view Ms. Yellen’s resignation announcement as healthy for the Fed’s functioning going forward, although her experience and her ability to talk to the markets will certainly be missed.

Ms. Yellen’s resignation announcement on Monday, however, did confirm that President Trump has another Fed Governor position to fill. The Fed’s Board of Governors has seven positions, including the Fed Chair, Vice Chair, and five Governors. Once Jerome Powell switches from a Fed Governor to the Fed Chair position, open seats will include the Vice Chair and three Governor positions. There will be only two Governors carrying over into early 2018, i.e., Lael Brainard and Randy Quarles.

That means that President Trump currently must replace a majority of the Fed seats with own picks, giving him wide latitude to affect the dovish/hawkish bent of the Fed going into 2018. Mr. Trump has already appointed Jerome Powell as the new Fed Chair, which was viewed by the markets as a dovish choice relative to the other main contenders of John Taylor or Kevin Warsh.

The turnover of FOMC voters will also be affected by the normal rotation of regional Fed Presidents who will become FOMC voters in 2018. Specifically, Fed Presidents who will become FOMC voters in 2018 include Cleveland’s Mester, Richmond’s Mullinix, Atlanta’s Bostic, and San Francisco’s Williams. Fed Presidents losing their FOMC voting rights in 2017 include Chicago’s Evans, Philadelphia’s Harker, Dallas’ Kaplan, and Minneapolis’ Kashkari.

Adding to the turnover, NY Fed President Dudley has announced his resignation, meaning his replacement will be an FOMC voter in 2018 since the NY Fed has a permanent voting position on the FOMC.

The big turnover in FOMC voters in 2018, and the new leadership from Jerome Powell, could imply a major new direction for the Fed in 2018. However, we expect little change in the Fed’s overall policy course in 2018. Mr. Powell is expected to push the status quo for Fed policy and he will undoubtedly be fully supported by the Fed’s staff.

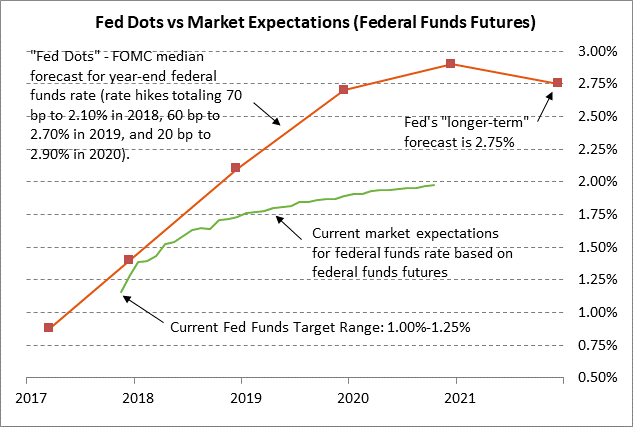

The markets continue to doubt that the Fed will follow through with the Fed-dot forecast for three +25 bp rate hikes in 2018 to add to December’s expected rate hike. The markets are only discounting 1-1/2 rate hikes in 2018, which is half of the Fed-dot forecast for three rate hikes.

However, we believe that the Fed will end up making good on its forecast for three rate hikes in 2018, assuming there are no intervening disasters. We believe that the Fed is chomping at the bit to at least get the funds rate target up to its current forecast of 2.1% by the end of 2018 so that the funds rate is slightly above inflation. The current funds rate target midpoint of 1.125% is below inflation, meaning the funds rate is at a negative inflation-adjusted (real) level. With a solid U.S. economy and a tight labor market, there is no justification at present for a negative real funds rate. With a negative real funds rate, the Fed is simply asking for trouble by encouraging bubbles and risk-taking. We believe the Fed will move to at least a slightly positive real funds rate as soon as it reasonably can.

Germany appears to be slipping towards new elections — After German coalition talks collapsed on Sunday night, German Chancellor Merkel on Monday seemed to rule out trying to rule with a minority government (where government action is taken with ad hoc coalitions). Ms. Merkel on Monday said she would rather face voters than risk an unstable German government.

Meanwhile, Social Democrats on Monday seemed to remain opposed to entering a new coalition with Ms. Merkel’s CSU party. That means that Ms. Merkel’s only options are to (1) try to resume talks for a CSU-Greens-Free Democrats coalition despite Sunday night’s breakdown, or (2) call for a new national election. The polls suggest that the outcome of a new election would be roughly the same as the last election in October, meaning a new election might not put Germany any closer to having a functioning government.

German stocks on Monday morning initially sold off on the Sunday-night news of the collapse of coalition talks. However, the German Dax on Monday recovered and closed the day up +0.50%, which was a larger gain than the +0.39% close in the Euro Stoxx 50 index. However, EUR/USD closed the day down -0.48% on the heightened Eurozone political uncertainty.

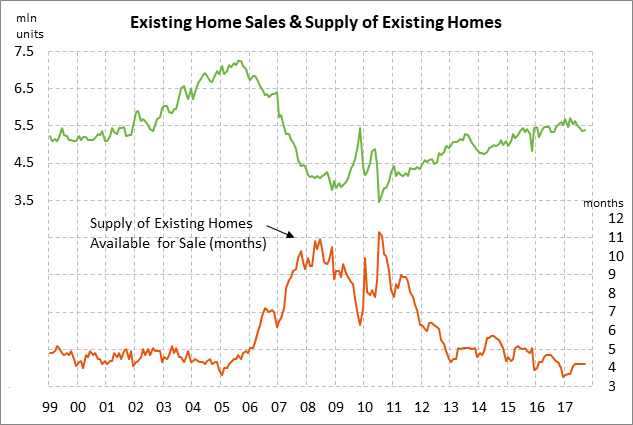

U.S. home sales expected to remain steady after hurricane disruptions — The market consensus is for today’s Oct existing home sales report to show a +0.2% gain to 5.40 million, adding to Sep’s +0.7% gain to 5.39 million. Home sales in the South in September fell by -0.9% due to hurricane disruptions but that decline was more than offset by gains in the West and Midwest. Oct home sales should see a small increase on a recovery of sales in the South. However, home sales in general are being dampened by high prices and tight availability.