- Big announcements coming with House tax bill on Wed and Fed chair appointment on Thursday

- FOMC meeting expected to be uneventful

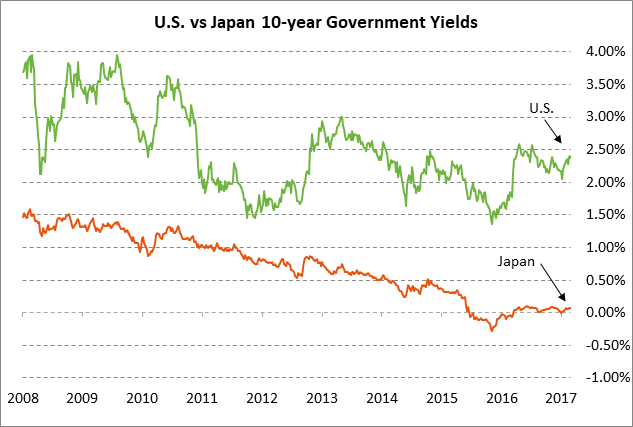

- BOJ expected to leave policy unchanged

- Oct U.S. consumer confidence expected to show a solid increase

- U.S. metropolitan home prices are expected to pick up

Big announcements coming with House tax bill on Wed and Fed chair appointment on Thursday — The markets are eagerly awaiting the announcement of the House tax bill, which is expected on Wednesday. Meanwhile, Politico reported on Monday that President Trump will announce his pick for the new Fed chair on Thursday, the day before he leaves on his 12-day trip to Asia. Regardless of media reports, however, Mr. Trump’s announcement of the new Fed chair could come at any time he chooses.

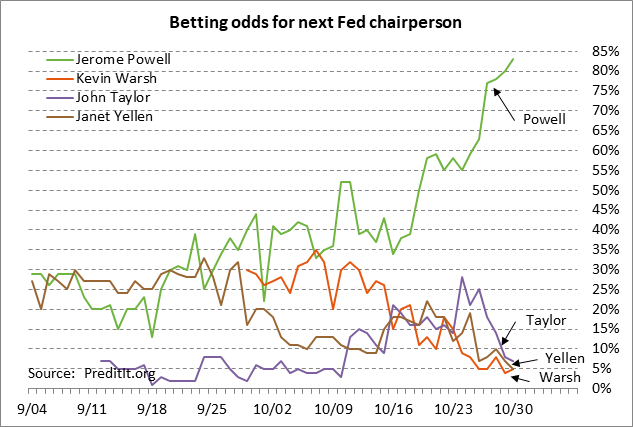

All press reports continue to say that President Trump is strongly leaning towards Fed Governor Jerome Powell as the new Fed Chair, although administration officials stress that Mr. Trump could still change his mind at the last minute. The betting odds continue to favor Mr. Powell by a wide margin, which means that the markets would be surprised, and negatively impacted, if Mr. Trump decides to appoint economist John Taylor as Fed Chair, who is considered to be a hawk. Mr. Trump could also appoint Mr. Taylor, however, to one of the open positions as a regular Fed Governor or as the Vice Chair.

The betting odds late Monday at PredictIt.org for the next Fed chair were 83% for Powell, 7% for Taylor, 5% for Yellen, 5% for Warsh, and 2% for Cohn.

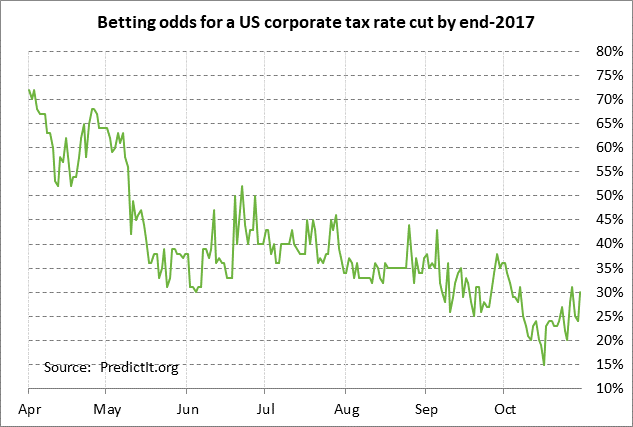

On the tax front, the stock market on Monday was undercut by a Bloomberg report that House Republicans are considering a plan for a corporate tax rate cut to be phased in over 5 years with a 3-point drop per year, ending with a 20% rate in 2022. The stock market was disappointed by the idea that a corporate tax cut might not occur up-front in 2018 as the market has been hoping. However, the Trump administration quickly threw cold water on the idea with Treasury Secretary Mnuchin saying “the objective is not to have that phase in, but we will see how that goes.”

The betting odds for a corporate tax cut by the end of 2017 rose by +6 points to 30% on Monday but remains generally low. However, the odds in our view are much better for a tax cut in 2018 since getting a tax cut passed has virtually become an existential issue for Republicans.

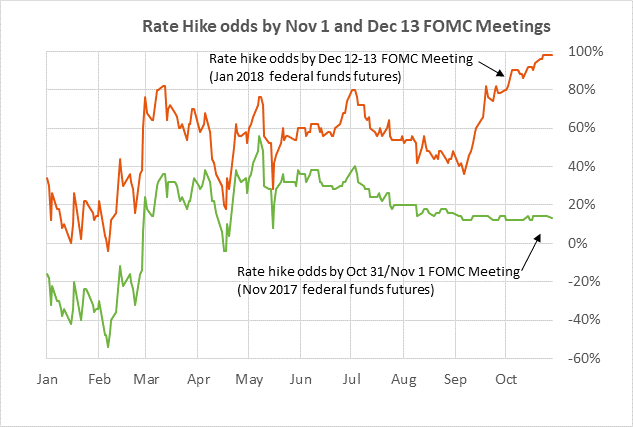

FOMC meeting expected to be uneventful — The 2-day FOMC meeting that begins today is expected to be uneventful, unless the FOMC surprises the markets with some significant changes in the wording of the post-meeting statement. The market is discounting only a negligible 13% change of a Fed rate hike today, based on the Nov 2017 federal funds futures contract.

The market is not expecting a Fed rate hike today because (1) there is no Yellen press conference scheduled for this week’s meeting, and (2) the FOMC at its last meeting in September just made a tightening move by announcing the beginning of its balance sheet drawdown program on Oct 1. The FOMC this week is expected to let the balance sheet drawdown program settle in before making its third and final rate hike of the year at its next meeting on Dec 12-13. The market is discounting a 98% chance of a Fed rate hike at the December meeting.

BOJ expected to leave policy unchanged — The BOJ at its 2-day meeting that concludes today is expected to leave its policy unchanged with its short-term policy rate at -0.1% and its 10-year JGB target at zero. The BOJ is expected to leave intact the size of its QE program at the annual figure of 80 trillion yen.

The 10-year JGB yield has recently risen to 0.07% on some upward carry-over pressure from U.S. yields, but the JGB yield has not yet challenged the perceived +0.1% upper limit of the BOJ’s target. The BOJ successfully defended the upper end of that target back in July with a large JGB buying operation to push yields lower. The BOJ continues to undershoot its 2% inflation target by a long shot, meaning the BOJ’s QE program is expected to continue at least through 2018. Japan’s core CPI in September was up by only +0.7% y/y.

Oct U.S. consumer confidence expected to show a solid increase — The market consensus is that today’s Oct Conference Board U.S. consumer confidence index will show a +1.2 point increase to 121.0, more than offsetting September’s -0.6 point decline to 119.8. The consumer confidence index soared after last November’s election and reached a 16-3/4 year high of 124.9 in February. The index has since been moving mostly sideways and in September was only -5.1 points below that high at 119.8. The University of Michigan’s U.S. consumer sentiment index for September has already been reported at +5.6 to 100.7, providing a strong back-drop for today’s Conference Board index.

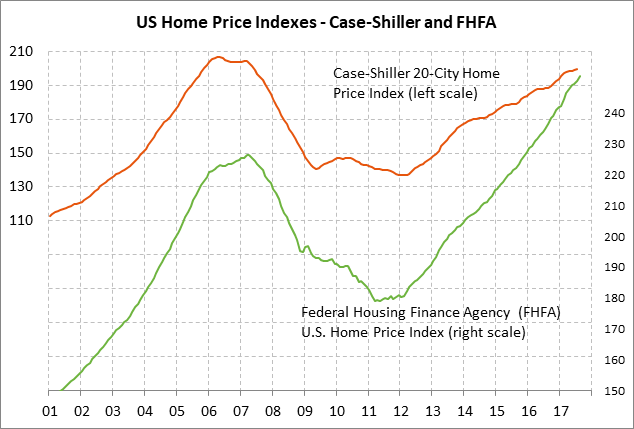

U.S. metropolitan home prices are expected to pick up — The market consensus is for today’s Aug S&P CoreLogic Composite-20 home price index to show a solid increase of +0.4% m/m and +5.9% y/y, which would be close to the July report of +0.35% m/m and +5.81% y/y. The index has shown smaller increases in the past three months (+0.1% in May and June and +0.3% in July) after sharp average increases near +0.7% from Oct 2016 through March 2017. Nevertheless, metropolitan home prices continued to march higher in recent months and were up sharply by +5.9% in July.

Home prices continue to rise due to mildly tight supplies combined with strong demand. FHFA has already reported that its home price index in August rose sharply by +0.7% m/m and +6.6% y/y, which bodes well for today’s Composite-20 index.