- Weekly U.S. market focus

- Payroll report supports view of stable U.S. economy and on-track Fed

- Q2 earnings season begins with positive expectations

- U.S. T-note yields have seen upward pressure from bunds and domestic factors

U.S. stock market keys on tech stocks and interest rates

Weekly U.S. market focus — The U.S. markets this week will focus on (1) Fed Chair Yellen’s semi-annual testimony to House and Senate committees on Wed-Thu and whether she provides any hints on the timing of the Fed’s balance sheet reduction program or the next rate hike, (2) whether Republicans in Congress can make any progress on their health care or tax bills as they return from last week’s recess, (3) the beginning of Q2 earnings season with 9 of the S&P 500 companies due to report this week, (4) whether big moves in U.S. tech stocks continue to buffet the direction of the overall U.S. stock market, (5) whether bund yields start to top out after soaring for the past two weeks and causing a sharp upward move in U.S. T-note yields, and (6) oil prices, which continue to trade defensively with a 1-week low last Friday.

The G-20 meeting this past Friday-Saturday was generally successful in papering over differences and avoiding any negative surprises. The G-20 tried to co-opt President Trump into considering Chinese steel overcapacity at a multilateral level, but the markets are nevertheless waiting to see whether the Trump administration at any time now might announce tariffs on U.S. steel imports based on a claimed threat to U.S. national security. There are fears that such an announcement could lead to trade retaliation by other countries.

This week’s main U.S. economic reports include Thursday’s June PPI (expected +1.9% y/y headline and +2.0% core from May’s +2.4% headline and +2.1% core) and Friday’s June retail sales (expected +0.3%) and June CPI (expected +1.7% y/y headline and +1.7% from May’s +1.9% and +1.7%). Other U.S. reports on Friday include June industrial production (expected +0.3%) and the preliminary-July U.S. consumer sentiment index (expected -0.1 to 95.0). The Treasury on Tue-Thu will sell $56 billion of 3-year, 10-year and 30-year securities.

In overseas news this week, the market will be watching (1) Wednesday’s Bank of Canada policy meeting, which is expected to produce a +25 bp rate hike, (2) whether the Bank of Japan is successful in preventing the 10-year JGB yield from rising above 0.10%, and (3) this coming Sunday’s Chinese economic data that includes Q2 GDP (expected +6.8% after Q1’s +6.9%), June industrial production (expected unchanged from May at +6.5% y/y), and June retail sales (expected +10.7% y/y vs May’s +10.6%).

Payroll report supports view of stable U.S. economy and on-track Fed — Last Friday’s June payroll report of +222,000 was substantially stronger than market expectations of +178,000. In addition, there were upward revisions totaling +47,000 for April (to +207,000 from +174,000) and May (to +152,000 from +138,000). Friday’s report produced a 3-month moving average for payrolls of a respectable +194,000.

Last Friday’s payroll report supported the Fed’s view that the recent weakness in the U.S. economy was transitory and that growth should improve through the remainder of the year. Friday’s average hourly earnings report of +2.5% y/y was up from May’s preliminary level of +2.4% but was slightly below the consensus of +2.6%. All in all, Friday’s unemployment report indicated a steady U.S. economy in which the Fed will see a green light for its intended near-term tightening path, which includes one more rate hike in 2017 and the beginning of its balance sheet reduction program. The market is discounting the odds for a Fed rate hike at 30% by September and 72% by December.

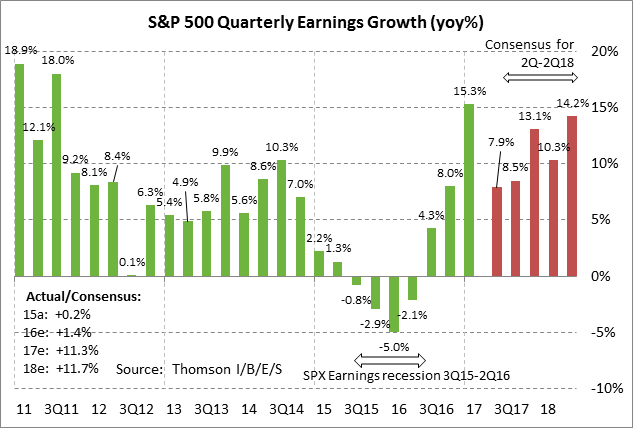

Q2 earnings season begins with positive expectations — The Q2 earnings season ramps up this week with 9 of the S&P 500 companies scheduled to report. Notable reports this week include Pepsico and Yum Brands on Tuesday; Delta on Thursday; and Citigroup, JP Morgan Chase, and Wells Fargo on Friday. The market consensus is for Q2 earnings growth of +7.9% (+4.8% ex-energy), according to surveys by Thomson Reuters I/B/E/S, down from expectations of +10.2% as of April 1 and +11.9% as of Jan 1. Looking ahead, earnings growth is expected to remain relatively strong through year-end with growth of +8.5% in Q3 and +13.1%. On a calendar year basis, the consensus is for SPX earnings growth of +11.3% in 2017 and +11.7% in 2018.

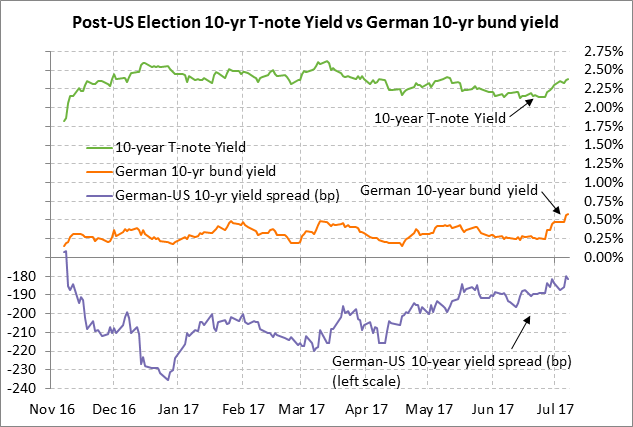

U.S. T-note yields have seen upward pressure from bunds and domestic factors — The 10-year T-note yield in the space of just two weeks has soared by +24.3 bp and closed last Friday at a new 2-month high of 2.386%. That upward move was due to (1) the +31.8 bp surge in the German 10-year bund yield to last Friday’s 1-1/2 year high of 0.573% that was caused by hawkish comments by ECB President Draghi and ideas that the ECB is moving towards a QE tapering announcement at either its Sep or Oct meeting, (2) a +15.5 bp surge in the Dec 2018 federal funds futures contract to 1.61%, reflecting increase market expectations for Fed tightening over the next 1-1/2 years, and (3) a +4.2 bp rise in the 10-year breakeven rate over the past two weeks. The T-note market this week will key mainly on bund yields, whether Ms. Yellen is hawkish in her testimony on Wed-Thu, the reception for this week’s Treasury auctions, and the U.S. economic data.

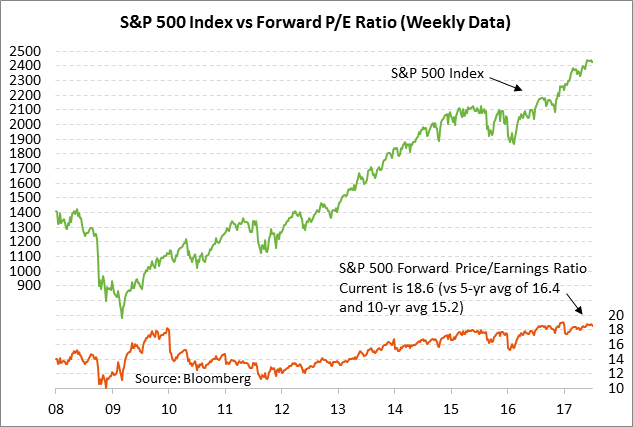

U.S. stock market keys on tech stocks and interest rates — The U.S. stock market this week will continue to take its cues from tech stocks and T-note yields. Weak tech stocks and higher T-note yields have conspired in the past several weeks to cause a mild downside correction in U.S. stocks. The stock market starting this week will also have Q2 earnings reports to digest. Strong earnings should continue to underpin the stock market but concerns will continue about stretched valuations with the SPX forward P/E at 18.6 (vs the 5-year average of 16.4 and 10-year average of 15.2).