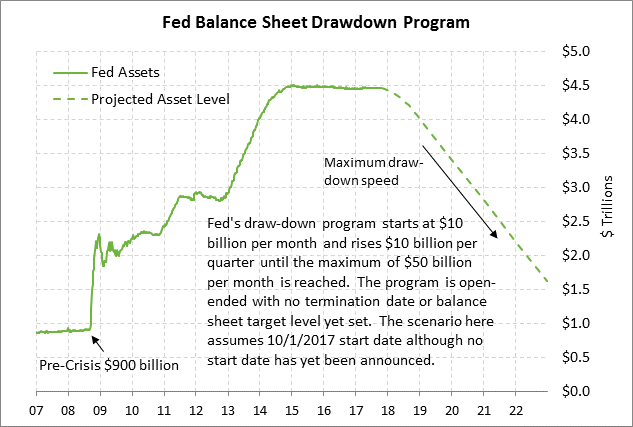

- Balance sheet reduction likely to take priority over the next rate hike as FOMC minutes are released today

- U.S. factory orders report expected to be weak

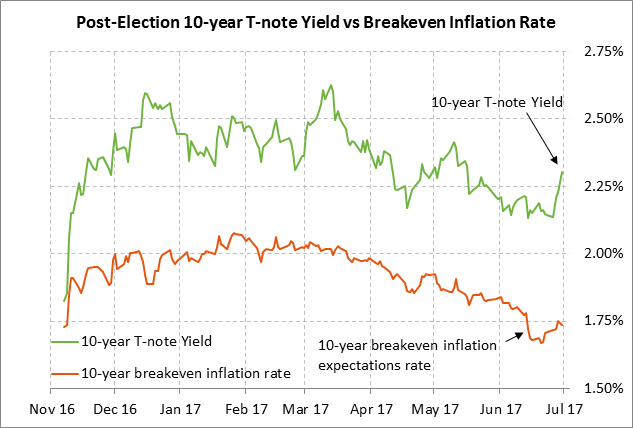

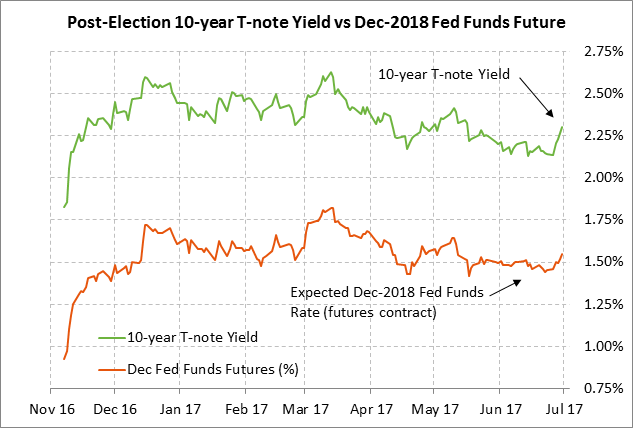

- Rise in 10-year T-note yield is mainly due to surge in bund yields but also to higher inflation expectations and tighter Fed policy expectations

Balance sheet reduction likely to take priority over the next rate hike as FOMC minutes are released today — The FOMC today will release the minutes from its June 13-14 meeting. The FOMC at that meeting announced a fully-anticipated +25 bp rate hike to 1.00-1.25% and also announced the details of its balance sheet reduction program, which the FOMC said would begin “later this year.”

We continue to believe that the Fed is likely to start its balance sheet reduction plan at the beginning of the fourth quarter so that the plan is concurrent with calendar quarters. The Fed has said that it will begin the plan with a capped roll-off of $10 billion per month, rising by $10 billion every three months until the maximum cap of $50 billion per month is reached.

If the Fed indeed wants to begin its balance sheet reduction program on Oct 1, then the Fed could announce that start date at either of its next two meetings on July 25-26 or Sep 19-20. The main caveat for a Q4 start for the balance sheet program, however, is that there is the double threat of a U.S. government shut-down on Oct 1 and/or a Treasury default in early to mid-October when the debt ceiling must be raised. The Fed might want to delay its balance sheet reduction plan until those threats have passed.

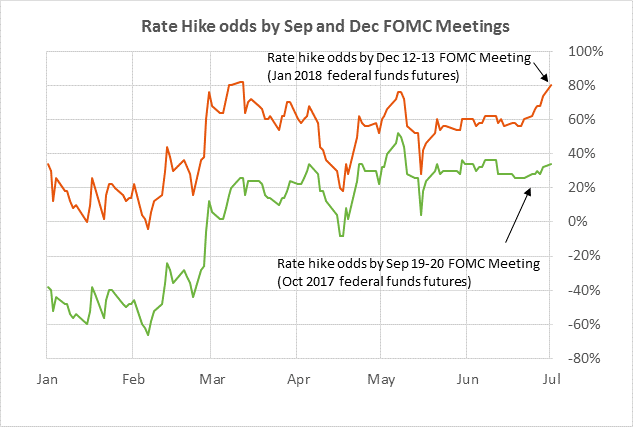

The Fed has so far lifted interest rates twice this year, leaving one more rate hike if the Fed wants to meet its Fed-dot forecast of three rate hikes per year during 2017 through 2019. The markets are attributing low odds for that rate hike at the next three FOMC meetings, i.e., 12% by the July 25-26 meeting, 28% by the Sep 19-20 meeting, and 30% by the Oct 31/Nov 1 meeting. However, the odds improve to 62% for the last meeting of the year on Dec 12-13.

The markets still have significant doubts about whether the Fed will go through with that third rate hike because of the recent softness in the U.S. economic data and inflation statistics. In addition, we believe that the FOMC is placing a higher priority at present on getting its balance sheet reduction program started than on raising interest rates another notch, meaning the Fed might defer a rate hike if necessary in order to get its balance sheet program going.

We suspect the Fed would like to get its balance sheet program fully established before potential Fed uncertainty emerges late this year when President Trump is expected to announce a new Fed chairperson to take Janet Yellen’s place when her chair term expires on Feb 3, 2018. Mr. Trump has said he would consider reappointing Ms. Yellen to another term as Fed chair, but there have been media reports that Mr. Trump’s economic advisors favor choosing a new Fed chief. It would be beneficial for the Fed for the balance sheet reduction program to already be in progress when Senate hearings are likely to be held late this year for a new Fed chairperson, thus avoiding the possibility that a yet-to-be-started balance sheet program could become a political football.

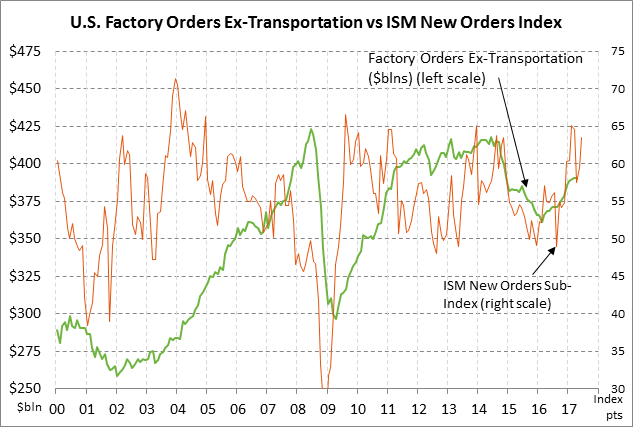

U.S. factory orders report expected to be weak — The market consensus for today’s May factory orders report is for a decline of -0.5%, weakening from April’s report of -0.2% and +0.1% ex transportation. Expectations for a weak factory orders report today stem in part from the already-reported May durable goods orders report of -1.1% and +0.1% ex-transportation. Durable goods orders account for about half of the factory orders series.

Despite expectations for a lackluster factory orders report today, there was positive news for the manufacturing sector in this past Monday’s ISM report. The June ISM manufacturing index unexpectedly rose by +2.9 points to a new 2-1/4 year high of 57.8. Moreover, the ISM manufacturing new orders sub-index rose by +4.0 points to the strong level of 63.5, indicating a strong orders pipeline.

Rise in 10-year T-note yield is mainly due to surge in bund yields but also to higher inflation expectations and tighter Fed policy expectations — The 10-year T-note yield on Monday moved higher by another +5 bp to 2.35%, bringing the 1-1/2 week surge to a total of 21 bp since June 23. That jump in the 10-year T-note yield has mainly been due to the 22 bp surge in the 10-year German bund yield to a 3-1/2 month high of 0.48%. The surge in the bund yield in turn was caused by ECB President Draghi’s hawkish comments last Tuesday when he appeared to begin the process of preparing the markets for QE tapering in 2018 with an ECB announcement at either its Sep or Oct meetings. The surge in the bund yield was bearish for T-notes due to expectations for weaker European demand for Treasury securities because of improved Eurozone yields at home. In addition, the end of the ECB’s QE program in 2018 would mean reduced global liquidity in general.

The recent surge in the 10-year T-note yield has also been due, however, to higher inflation expectations and tighter Fed expectations. The 10-year breakeven rate has risen by +5 bp in the past 1-1/2 weeks due to the +9% surge in oil prices. Meanwhile, the rise in Fed rate-hike expectations can be seen in the +13.5 bp rise in the Dec 2018 federal funds futures contract to a yield of 1.59% from 1.455% on June 23.

The sharp drop in T-note prices seen since last week caused volatility to at least temporarily surge. The TYVIX index, which measures 30-day expected volatility for the 10-year T-note futures contract, jumped to a 1-1/2 month high of 4.87% last Friday and then eased slightly to 4.82% on Monday. That was sharply higher than the 8-1/2 month low of 3.98% posted on June 16 and 26.