- Weekly U.S. market focus

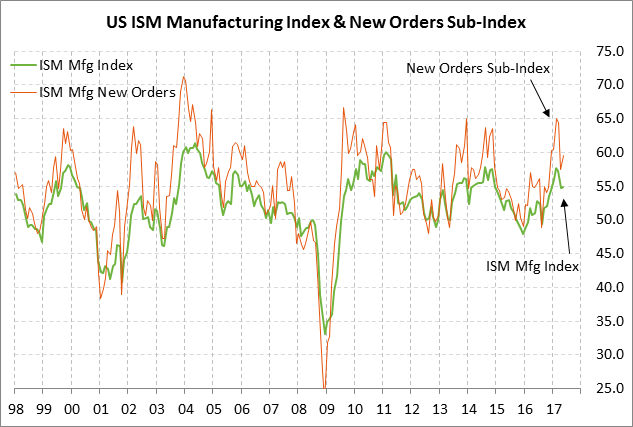

- U.S. ISM manufacturing index expected to remain strong

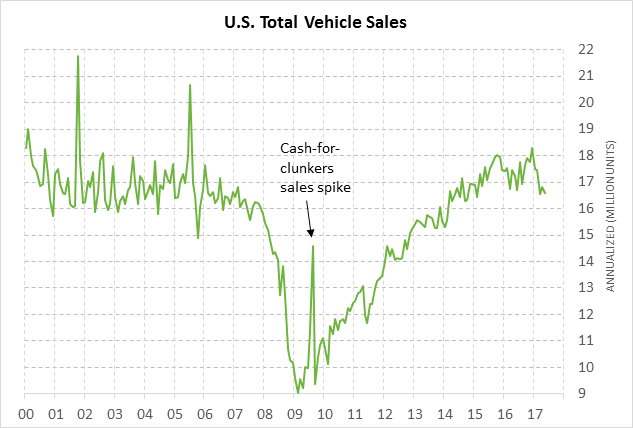

- U.S. vehicle sales expected to post new 2-1/4 year low

- T-note yield rises to 1-1/2 month high on hawkish Draghi and rising oil prices

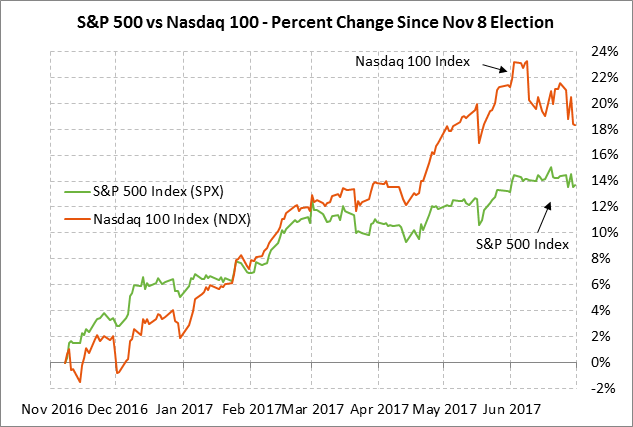

- U.S. stocks remain on the defensive due to tech stocks and rising rates

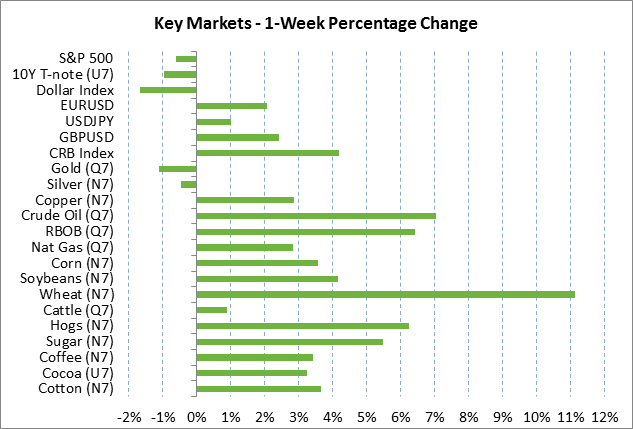

Weekly U.S. market focus — The U.S. markets during this holiday-shortened week will focus on (1) whether Friday’s June payroll report shows the expected improvement in payroll growth to +175,000 from the weak 3-month (Mar-May) moving average of +121,000, (2) the G-20 Summit meeting on Fri-Sat in Hamburg with some key side meetings including Xi-Merkel and Trump-Putin, (3) whether Wednesday’s minutes from the June 13-14 FOMC meeting contain any hints on the timing of the Fed’s next rate hike and/or the beginning of the Fed’s balance sheet reduction program, and (4) whether the nascent recovery in oil prices continues as Aug crude oil prices last week rebounded by +7.04%% to a 3-week high close of $46.04.

Oil prices last week saw some support from indications that U.S. oil production may be starting to falter after last week’s large -100,000 bpd (-1.1%) decline from the previous week’s 2-year high. In addition, Baker Hughes on Friday reported that active U.S. oil rigs fell by -2 rigs to 756 from the previous week’s 2-1/4 year high of 758 rigs, which was the first decline in rigs in 5 months. Last week’s +7% recovery in oil prices helped the SPDR Oil & Gas Exploration & Production ETF (XOP) to rally +2.90% on the week. Keeping a lid on oil prices, however, is the sharp +32% rise in Libyan production to 1.0 million bpd in June from 760,000 bpd in May.

Congress is on recess this week but will return next week with Senate Republicans trying to find a way forward on an Obamacare repeal-and-replace bill. After returning next week, Congress will have only three weeks to work on health insurance, a 2018 budget, and a host of other issues. Congress will then recess for the entire month of August and will return in September with little time left to pass spending authority for the new fiscal year that starts on Oct 1 and approve a debt ceiling hike by the X-date in early to mid-October. The markets in Sep-Oct will face the double threat of a government shutdown and Treasury default.

The Japanese markets on Monday will react to the big loss by Prime Minister Abe’s LDP party in Sunday’s Tokyo election. The LDP won only 19-29 seats in the Tokyo assembly based on early exit polls, far below the 40-50 seats taken by the new Tokyo Residents First party in the 127-seat assembly. The Tokyo loss illustrated the falling popularity of the ruling LDP party and will likely force Prime Minister Abe to reshuffle his cabinet. The LDP faces national elections next year.

U.S. ISM manufacturing index expected to remain strong — The market consensus for today’s June ISM manufacturing index is for a +0.3 point increase to 55.2, adding to May’s +0.1 point increase to 54.9. Markit’s preliminary-June U.S. manufacturing PMI has already been released and showed a -0.6 point decline to 52.1, which did not bode well for today’s ISM index. The final-June Markit report today is expected to be left unrevised at 52.1.

The ISM manufacturing index after the November election rose by +5.7 points to a 2-3/4 year high of 57.7 in February. The index fell back in March-April but stabilized at 54.9 in May, which is a level that illustrates fairly strong confidence among U.S. manufacturing executives. Meanwhile, the manufacturing new orders sub-index rebounded higher by +2.0 points to 59.5 in May, which was a strong figure suggesting that the manufacturing orders pipeline continues to fill.

The U.S. manufacturing sector is seeing strength from (1) the oil sector, and (2) an improved export outlook based on this year’s decline in the dollar and improved economic growth overseas. The main negative for the U.S. manufacturing sector is emerging weakness in the U.S. auto sector.

U.S. vehicle sales expected to post new 2-1/4 year low — The market consensus is for today’s June total vehicle sales report to fall to 16.50 million from 16.58 million in May, which would take out March’s 2-1/4 year low of 16.53 million. The weakness in auto sales has raised questions about consumer spending and consumer health in general, particularly due to rising defaults in sub-prime auto loans. Rising risk in auto loans is causing some lenders to tighten up their credit standards, thus making it harder for consumers to finance and buy a car. A major warning sign for vehicle sales is that truck sales have topped out and fallen back in the past several months. In the past three years, strong truck sales have carried vehicle sales as a whole and have masked the steady decline in auto sales seen since late 2015. Auto sales in June hit a 5-3/4 year low of 5.96 million units.

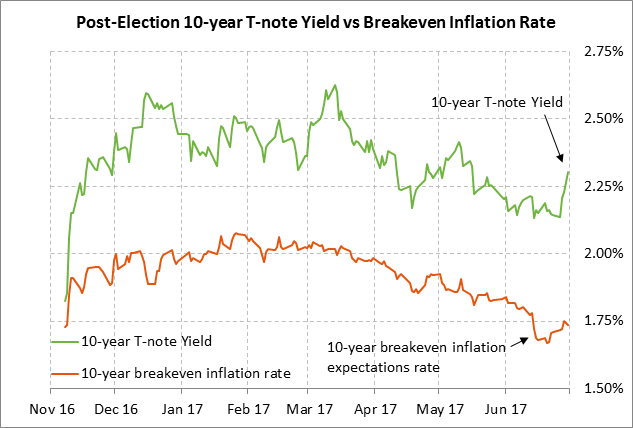

T-note yield rises to 1-1/2 month high on hawkish Draghi and rising oil prices — The 10-year T-note yield last week rose sharply by +16 bp to 2.30% and posted a 1-1/2 month high. Bearish factors included (1) the +21 bp surge in the 10-year bund yield to a 3-1/2 month high after ECB President Draghi last Tuesday issued some hawkish comments that made it appear as though he is starting to lay the ground work for an ECB QE tapering decision to be announced at the Sep or Oct meetings, (2) rising Fed rate hike expectations, and (3) last week’s +7.04% surge in Aug WTI crude oil prices, which led to an +8 bp rise in the 10-year breakeven rate to 1.74% from the mid-June 8-1/2 month low of 1.66%.

U.S. stocks remain on the defensive due to tech stocks and rising rates — The U.S. stock market last week traded on the defensive with the S&P 500 index last Thursday posting a new 1-month low and closing the week down -0.61%. Bearish factors included (1) continued weakness in tech stocks with the Nasdaq 100 index posting a new 1-1/2 month low on Thursday and closing the week down -2.69%, (2) the sharp +16 bp rise in the U.S. T-note yield, and (3) carry-over weakness from the sharp -2.87% sell-off in the Euro Stoxx 50 index.