- U.S. PCE deflator expected to edge lower and provide support for the sharp drop in inflation expectations

- U.S. personal income and consumption expected to show modest increases

- U.S. consumer sentiment expected to remain generally strong

- CBO sets early to mid-Oct as X-date for debt limit increase

U.S. PCE deflator expected to edge lower and provide support for the sharp drop in inflation expectations — The markets will be carefully watching today’s PCE deflator report to confirm whether inflation expectations should be as low as they are. The sharp drop in inflation expectations over the past three months has been the main factor driving Treasury yields lower, which in turn has provided support for stock prices and undercut the dollar. The PCE deflator is the Fed’s preferred inflation measure, making today’s report more important than either the CPI or PPI reports.

There has been a dramatic decline in the inflation statistics since March, which has been instrumental in driving inflation expectations lower. The CPI in the last three reporting months of March-May actually showed a deflationary decline of -1.0% on an annualized basis. On a year-on-year basis, the CPI in May fell to +1.9% y/y from February’s 5-1/4 year high of +2.7%.

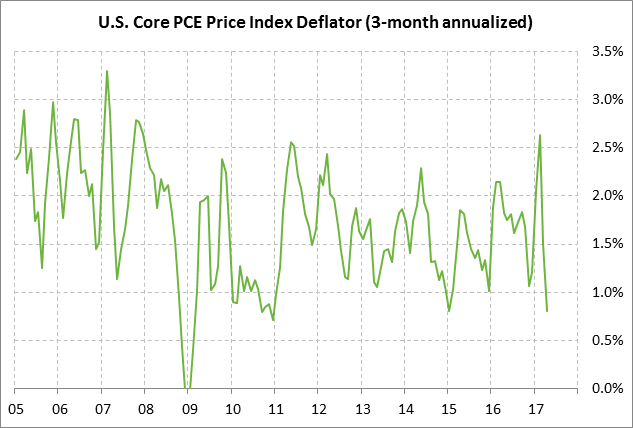

The core CPI showed a similar decline, illustrating that price weakness is not solely due to low oil prices. Specifically, the core CPI fell to +1.7% y/y in May from the 8-3/4 year high of +2.3% y/y posted in January. The core CPI in the 3 months through May was unchanged on an annualized basis, right on the edge of deflation.

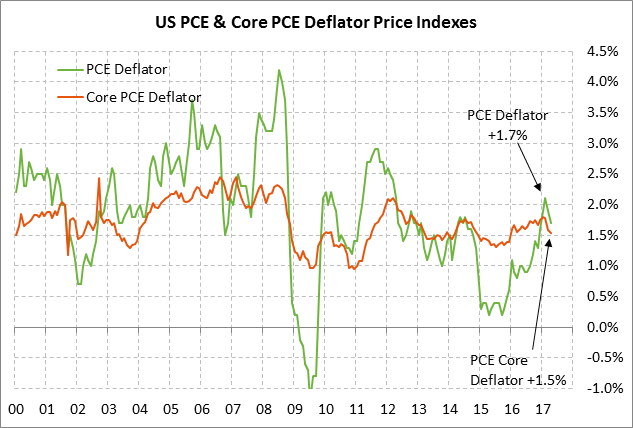

The PCE deflator has seen similar weakness. The PCE deflator in the last three months has shown a 3-month annualized gain of only +0.4% and the core CPI showed a +0.8% gain. On a year-on-year basis, the PCE deflator fell to +1.7% y/y in April from Feb’s 5-year high of +2.1%. The core PCE deflator fell to +1.5% in April from the 4-3/4 year high of +1.8% y/y posted in Jan-Feb.

The consensus is for today’s PCE deflator report for May to show continued weakness with a decline to +1.5% y/y from April’s +1.7%. The May core PCE deflator is expected to ease to +1.4% y/y from April’s +1.5%, which is well below the Fed’s inflation target of +2.0%.

Fed Chair Yellen in her recent comments has brushed off the recent decline in the inflation statistics as transitory. Ms. Yellen has made it clear that the Fed does not intend to be deterred from raising interest rates by the recent weakness in the inflation statistics. However, the weakness in the recent inflation data has caused other Fed officials to express some caution about further rate hikes.

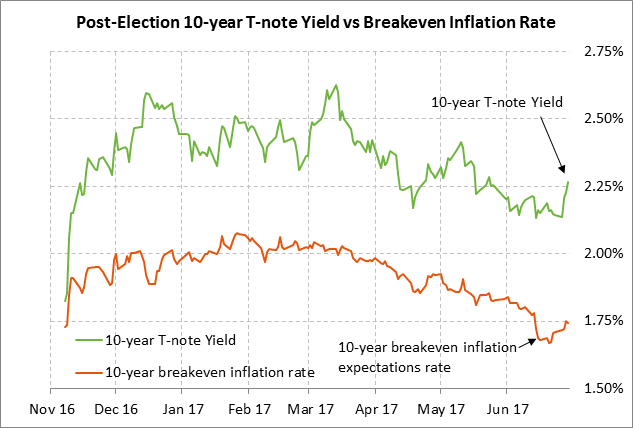

The importance of lower inflation expectations in driving T-note yields lower can be seen in the nearby chart. The 10-year breakeven inflation expectations rate since mid-March has fallen sharply by -26 bp from 2.00% to the current level of 1.74%. Over that same time-frame, the 10-year T-note yield has fallen by nearly the same amount, i.e., by -20 bp from 2.46% to the current level of 2.26%.

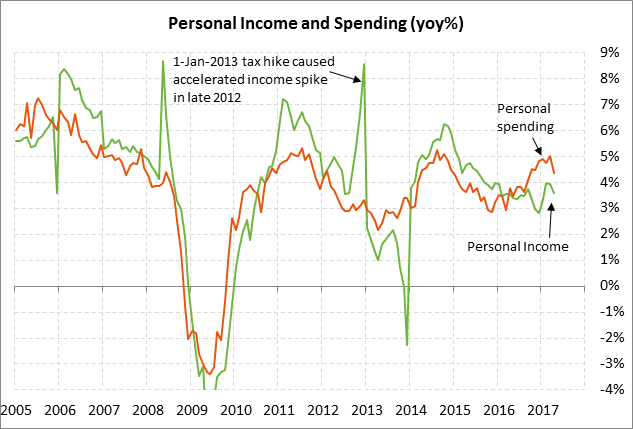

U.S. personal income and consumption expected to show modest increases — The market consensus is for today’s May personal spending report to show only a +0.1% increase, downshifting from April’s +0.4%. Meanwhile, the consensus is for today’s May personal income report to show an increase of +0.3%, adding to April’s +0.4% increase. The markets are also watching consumer income and spending very carefully since the recent weakness in consumer spending was the main factor behind the weak Q1 GDP report of +1.4%.

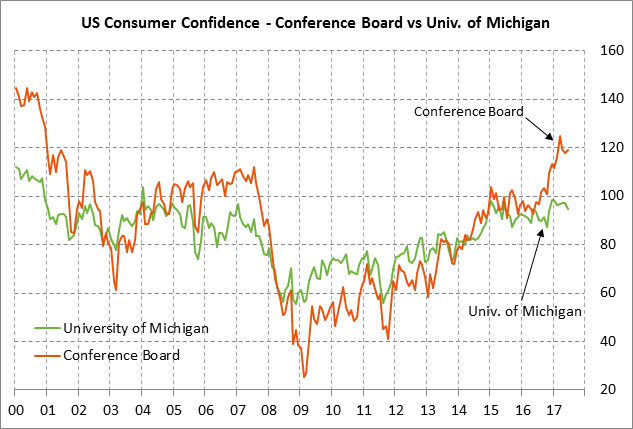

U.S. consumer sentiment expected to remain generally strong — The market consensus is for today’s final-Jun University of Michigan U.S. consumer sentiment index to be left unrevised from early June at 94.5, thus leaving the index down by -2.6 points from May. After the Nov 2016 election, the consumer sentiment index surged by +11.3 points to a 13-1/4 year high of 98.5 in January. However, the index has since fallen back and is 4.0 points below that high.

U.S. consumer sentiment remains high due to the strong labor market, record highs in the stock market, rising home prices and household wealth, expectations for personal tax cuts, and low gasoline prices. Negative factors include Washington political uncertainty and slow wage gains.

CBO sets early to mid-Oct as X-date for debt limit increase — The Congressional Budget Office on Thursday said that the debt limit must be raised by “early to mid-October.” That was the first specific estimate given by a government agency. Previously, Treasury Secretary Mnuchin had noted that the Treasury could last until early September with its emergency measures but did not go further in providing an X-date. The X-date is the day on which the Treasury will run out of cash and will no longer be able to pay all of its financial obligations, essentially putting the Treasury in the same position as a bankrupt company that cannot borrow money and has no cash left.

The Bipartisan Policy Center in recent weeks has been estimating that the Treasury’s X-date would be some time in October or November. The group says that Oct 2 is a particularly dangerous date since a large pension fund payment is due on that day, but the CBO apparently thinks the Treasury can make it past that Oct 2 date.

The fact that the CBO put the X-date past the October 1 start of the new fiscal year means that Congress may combine an Oct 1 spending deal and a debt limit increase in a single must-pass bill, instead of considering the measures separately. In any case, the markets in October now face the double threat of a government shutdown and/or a Treasury default if Congress does not act.

Attachment file(s):