- Weekly market focus

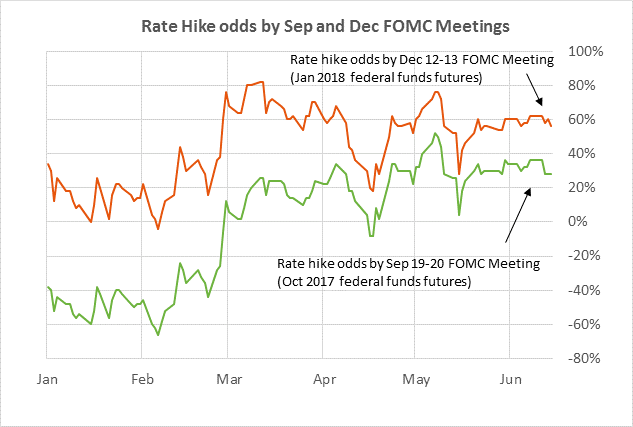

- Fed policy expectations turn more dovish

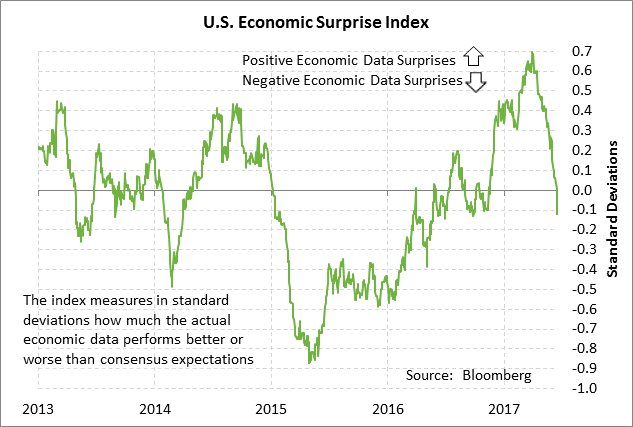

- U.S. economic surprise index falls to a 9-month low

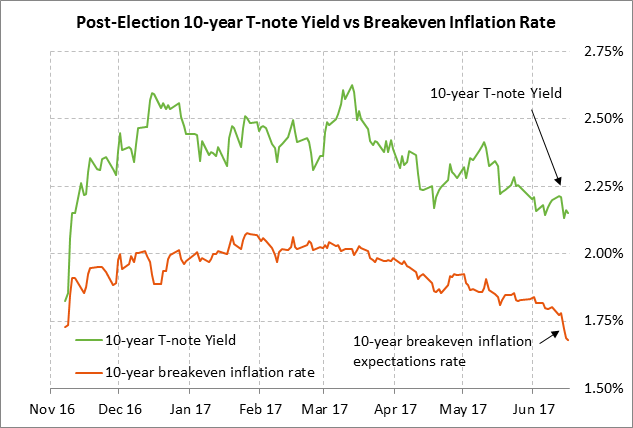

- T-note prices consolidate near 7-month high due to soft economic data and more dovish inflation expectations

- U.S. stock market remains resilient

Weekly market focus — The U.S. markets this week will focus on (1) whether Fed officials in seven different appearances this week suggest they might be turning a bit more dovish in the wake of softer inflation and economic data, (2) whether tech stocks continue to see weakness and continue to undermine the broad market, (3) any new developments on the Russia investigation as White House political uncertainty continues to weigh on the Republican growth agenda, (4) oil prices, which are teetering on the edge of May’s 14-month low, (5) Thursday’s Treasury auction of $5 billion of 30-year TIPS, and (6) a light earnings week with 9 of the SPX companies reporting including Lennar, Adobe and FedEx on Tuesday and Oracle on Wednesday.

In overseas news, the markets today will react to yesterday’s French legislative elections in which French President Macron’s “Republic on the March” party based on early returns appeared to have won a clear parliamentary majority but on low voter turnout. The markets will carefully watch the Chinese central bank in the unexpected event that it raises rates another notch to keep up with last week’s Fed rate hike. The ECB on Thursday will publish its monthly economic bulletin. UK Prime Minister May’s government is scheduled to formally begin Brexit negotiations this week despite the weakened state of Ms. May’s new government.

Fed policy expectations turn more dovish — The FOMC last week raised rates by another +25 bp but market expectations for the Fed’s future policy nevertheless turned more dovish. The federal funds futures curve last week turned more dovish by 2 bp for the late 2017 contracts, 2-4 bp for the 2018 contracts, and 4-5 bp for the 2019 contracts. The market last week reduced the odds for a rate hike later this year to 28% (from 36%) by September and to 56% (from 62%) by December.

Last week’s more dovish view of Fed policy was driven by soft inflation and economic data. The May CPI last week fell to +1.9% y/y and the core CPI fell to +1.7% y/y. Meanwhile, the 10-year breakeven inflation expectations rate last Friday fell to a 7-month low of 1.68% where it was well below the Fed’s inflation target of +2.0% and was even -5 bp below the pre-election level of 1.73%. Inflation expectations fell due to (1) the decline in the CPI report, (2) continued weakness in crude oil and commodity prices in general, (3) softer U.S. economic data, and (4) reduced expectations for the Republican growth agenda.

U.S. economic surprise index falls to a 9-month low — Fed policy expectations also turned more dovish last week due to weak U.S. economic data. Last Wednesday’s May retail sales fell by -0.3% and retail sales have shown virtually no net increase since February. Last Friday’s preliminary-June University of Michigan U.S. consumer sentiment index fell by -3.0 points to 84.7, weaker than market expectations for little change. Last Friday’s May housing starts report fell by -4.9%, weaker than market expectations of +1.7%. Last Thursday’s May manufacturing production report showed a -0.4% decline, weaker than market expectations of +0.1%.

The recent weakness in the U.S. economic data has caused the Bloomberg U.S. Economic Surprise index to plunge over the past 2-1/2 months. That index fell into negative territory last week for the first time since last November. The plunge in the index shows how the recent U.S. economic data has been substantially weaker than market expectations.

Fed Chair Yellen in her post-FOMC press conference last week brushed off the recent weakness in the inflation statistics as transitory and expressed confidence about the economy. Ms. Yellen still seems intent on implementing another rate hike by year-end and also beginning the Fed’s balance sheet roll-off program. However, some Fed officials are already getting cold feet. Dallas Fed President Robert Kaplan last Friday said that he is not ready to call a pause to Fed rate hikes, but that he wants to see “more evidence that we’re making progress in reaching our 2% inflation objective” before he would be comfortable in raising the funds rate another notch. Meanwhile, Minneapolis Fed President Neel Kashkari last Friday said he dissented from last week’s FOMC rate hike rate hike because of the recent softening of inflation pressures.

T-note prices consolidate near 7-month high due to soft economic data and more dovish inflation expectations — 10-year T-note future prices last week posted a 7-month nearest-futures high. Meanwhile, the 10-year T-note yield fell to a 7-month low of 2.10% on Wednesday before rebounding higher to 2.15% by Friday. The 10-year T-note yield is now only +32 bp above the pre-election level of 1.83% even though the Fed since the election has raised the funds rate three times by a total of +75 bp. 10-year T-note prices should continue to see an upside trading bias as long as the U.S. economic data and inflation are pointing lower.

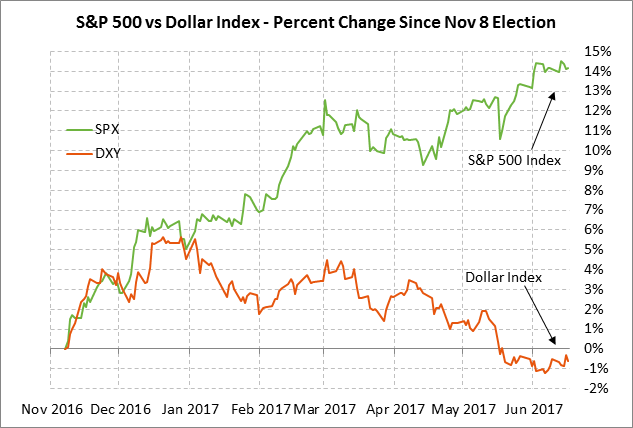

U.S. stock market remains resilient — The S&P 500 index last week consolidated near its recent record high and closed only -0.5% below that record high last Friday. The S&P 500 has been able to largely shake off the weakness in tech stocks that has helped drive the Nasdaq 100 index to an overall -4.5% downward correction. The resilience of the broad market suggests that investors remain generally positive on U.S. stocks despite such bearish factors as (1) the soft patch of U.S. economic data, (2) White House political uncertainty and the slow Republican agenda, and (3) stretched valuations. U.S. stocks last week were boosted by the 7-week lows in the 10-year T-note yield and the dollar index and by also by more dovish expectations for Fed policy. We remain cautiously bullish on stocks but the negative factors are starting to pile up.