- Triple-Thursday arrives with potential for volatility

- Comey testimony seems unlikely to move the ball much

- Dovish ECB meeting expected

- UK election watershed margin is 50 seats

- Unemployment claims

Triple-Thursday arrives with potential for volatility — There are three big events today: (1) the UK general election, (2) the ECB meeting, and (3) former FBI Director Comey’s testimony to the Senate Intelligence Committee.

The event with the most volatility potential for the U.S. markets is the Comey hearing because of the possible implications for President Trump and the Republican agenda. By contrast, the consequences of the UK election are likely to be limited mainly to the UK markets, and secondarily to the continental European markets if Conservatives don’t win and Brexit gets more complicated. The ECB meeting is expected to produce at most a guidance shift and is not likely to produce any big surprises.

Comey testimony seems unlikely to move the ball much — The U.S. markets have largely been ignoring the Russian investigation and the political turmoil in Washington, even though the turmoil has clearly had an impact on slowing down the Republican tax and infrastructure agenda. However, U.S. stocks back in mid-May did take a brief 2-day hit on the news that former FBI Director Comey wrote a contemporaneous memo about President Trump’s alleged request to Mr. Comey to let go of the FBI’s Flynn inquiry, which raised talk about obstruction of justice.

The Senate Intelligence Committee on Wednesday stole much of Mr. Comey’s thunder by releasing the prepared statement that Mr. Comey will read today. Of course, further information could emerge today as Mr. Comey is questioned by Committee members. Mr. Comey in his prepared statement lays out some potentially damaging allegations about his interactions with President Trump but he does not draw his own conclusion about whether President Trump obstructed justice, which after all is a charge that only Congress can decide in an impeachment process.

At this point, the obstruction of justice claim may still not be strong enough to force House Republicans to start thinking seriously about impeachment. Indeed, the betting odds are fairly strong at 77% that President Trump will still be the president at the end of 2017 and at 61% for the end of 2018, according to PredictIt.org. Still, if damaging facts continue to emerge on the Russian investigation and related matters, the markets may become more concerned about paralysis in Washington and an even slower Republican agenda.

Dovish ECB meeting expected — Market expectations for a dovish ECB meeting outcome today were boosted by Wednesday’s Bloomberg report quoting euro-area officials as saying that the ECB today will cut its inflation outlook due to the slide in energy prices. The market had originally thought the ECB might cut its 2017 inflation forecast but leave its 2017-18 forecasts unchanged. However, Bloomberg on Wednesday said that the ECB’s inflation forecast will be cut for 2018-19 as well, although the story warned that the draft figures have not yet been formally approved by the ECB and could change. The Bloomberg article said the ECB’s new CPI inflation forecasts will be roughly around +1.5% each year in 2017, 2018 and 2019. Those would be down from the ECB’s forecast in March of +1.7% in 2017, +1.6% in 2018, and +1.7% in 2019.

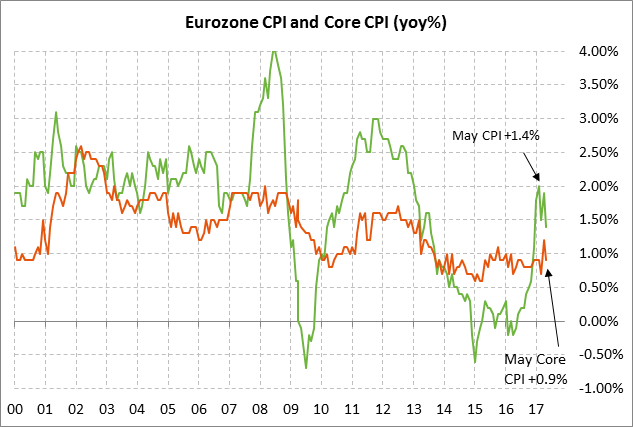

If the ECB does in fact reduce its inflation forecast to around +1.5% through 2019, that would mean that the ECB does not see much hope of reaching its inflation target of just below 2% over the next 2-1/2 years. That suggests that the ECB may move even more slowly on tightening up its guidance and tapering QE. The Eurozone CPI in May was at only +1.4% y/y and the core CPI was even lower at +0.9% y/y.

The markets are generally expecting the ECB today to shift to a balanced risk assessment from its current view that the risks are “still tilted to the downside.” The market seems to be assigning about a 50-50 chance that the ECB today will drop its reference to “lower” interest rates in its guidance that interest rates will stay at “present or lower levels” until “well past” the end of quantitative easing. On QE, the market consensus is that the ECB in September will announce that it will taper its QE program down to zero during the first half of 2018.

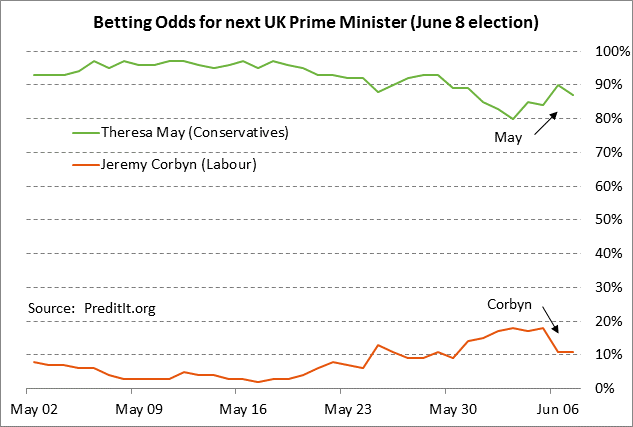

UK election watershed margin is 50 seats — The UK race has tightened in recent weeks with Conservatives now holding only a single-digit lead against Labour, down from 20 points at the beginning of the campaign. Nevertheless, Conservatives are still the overwhelming favorites to win the election. The betting odds are very strong at 87% that Theresa May will keep her job as Prime Minister versus odds of only 11% for Labour leader Jeremy Corbyn.

The key for market reaction will be the Conservatives’ margin of victory in the seat count. A larger margin of victory would be more supportive for sterling because it would give Prime Minister May a stronger hand to negotiate Brexit. Conservatives will be disappointed if they do not at least boost their seat margin to 50 seats from the current 17 seats. Sterling and UK stocks are likely to sell off sharply in the unlikely event of a hung Parliament where neither party has a majority of seats since that would lead to political gridlock just as Brexit negotiations are due to begin.

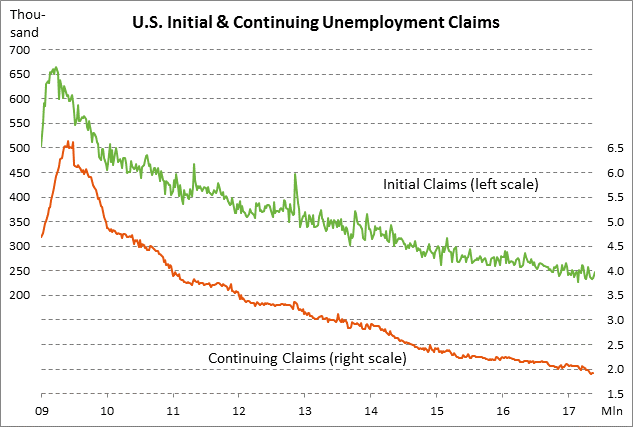

Unemployment claims — The consensus is that today’s initial unemployment claims report will show a -8,000 decline to 240,000 (after last week’s +13,000 increase to 248,000) and that continuing claims will show a +5,000 increase to 1.920 million (after last week’s -9,000 decline to 1.915 million). Claims remain in favorable shape since initial claims are only +21,000 above Feb’s 44-year low and continuing claims are only +16,000 above May’s 28-year low.