- U.S. JOLTS job openings expected to show a small decline but remain generally strong

- Post-election low in 10-year T-note yield suggests lower-yields-for-longer

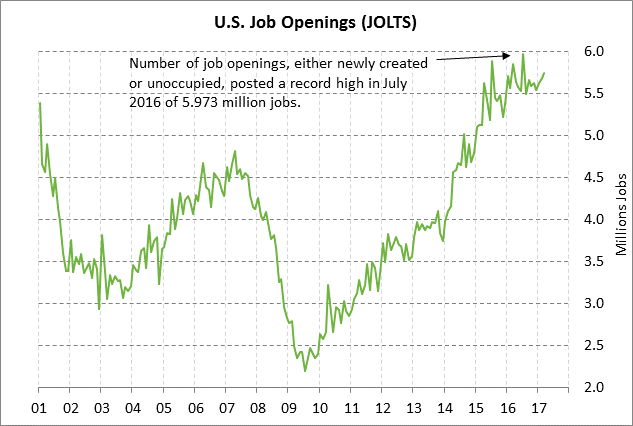

U.S. JOLTS job openings expected to show a small decline but remain generally strong – The market consensus for today’s April JOLTS U.S. job openings report is for a small +7,000 increase to 5.750 million following March’s strong report of +61,000 to 5.743 million.

The JOLTS job openings series remains in strong shape at 102,000 jobs above the 12-month average of 5.641 million. The series is far above the 4.5 million average seen before the Great Recession. The continued high level of the JOLTS job openings series is a positive leading indicator for the payroll report since many job openings will turn into an actual job hire within 1-3 months when the hiring process is complete.

The markets will be watching today’s job openings report more closely than usual due to last Friday’s weak May payroll report of +138,000. The weak payroll report may have been due in part to (1) seasonal distortions caused by the end of the school year, and (2) reduced hiring as the U.S. economy nears full employment. Nevertheless, the weak 3-month payroll average of +121,000 is causing some market concern that businesses may be pulling back on hiring.

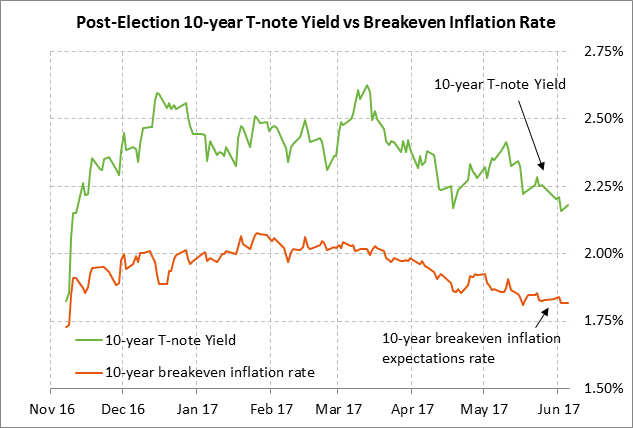

Post-election low in 10-year T-note yield suggests lower-yields-for-longer — The 10-year T-note yield on Monday closed +2 bp at 2.18%, which was just +4 bp above last Friday’s 6-3/4 month low of 2.14%. The 10-year T-note yield last Friday fell to the new post-election low due to the weaker-than-expected May payroll report of +138,000 and the tepid May average hourly earnings report of +2.5% y/y.

The 10-year T-note yield is now only +35 bp above the pre-election level of 1.83%, which is much less than the peak of +81 bp above the pre-election level when the 10-year yield in December hit its 2-1/2 year high of 2.64%.

The U.S. 10-year T-note yield has fallen in the past three months due to (1) weaker inflation pressures, (2) reduced expectations for Fed tightening later this year and in 2018-19, (3) some doubts about the health of the U.S. economy after weak Q1 consumer spending and tepid job gains in March-May, (4) continued strong foreign demand for U.S. Treasuries due to low bond yields in Europe and Japan, (5) the slow Republican growth agenda, (6) the threat of a major Republican-Democratic showdown this autumn over the 2018 budget and the need for a debt ceiling hike, and (7) some safe-haven demand with a possible Italian election this fall and with various geopolitical risks including North Korea.

Factors that are still putting upward pressure on yields, however, include (1) the Fed’s intention thus far to proceed with its rate-hike regime regardless of market doubts, (2) the possibility that the market could get spooked about the Fed’s balance sheet reduction program although the Fed intends to start the program off slowly, and (3) the possibility that Congressional Republicans could still produce tax cut legislation this year that would give the U.S. economy some fiscal stimulus next year.

Turning back to the dovish factors for T-note yields, the U.S. inflation outlook has cooled over the past three months, which has helped push T-note yields lower. The 10-year breakeven inflation expectations rate on Monday was at 1.82%, which is down by more than -18 bp from levels above 2.00% level seen as recently as mid-March. The 10-year breakeven rate is now only +9 bp above the pre-election level of 1.73%.

The U.S. inflation outlook has cooled due to (1) the decline in the April core PCE deflator to a 1-1/4 year low of +1.5% y/y from the 4-3/4 year high of +1.8% posted in Jan-Feb, (2) lower oil prices that have pushed the headline U.S. inflation statistics lower, and (3) the slow Republican growth agenda that has largely eliminated post-election concerns about a surge in inflation from fiscal stimulus and infrastructure spending.

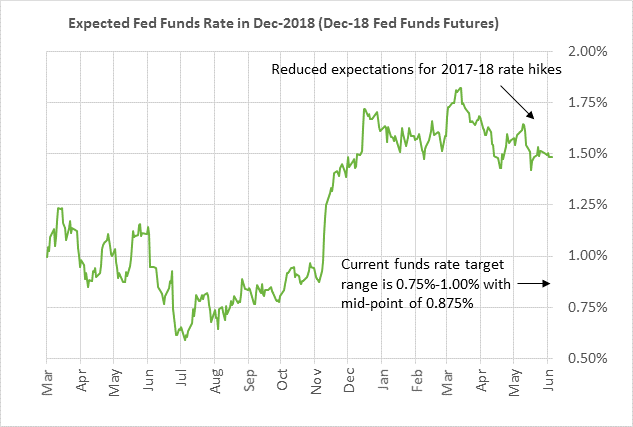

Reduced expectations for Fed rate hikes have also pushed T-note yields lower. The markets see a reduced need for Fed rate hikes over the next 1-1/2 years since the U.S. economy and inflation remain tepid and since Republicans are having difficulty producing tax cut and infrastructure programs.

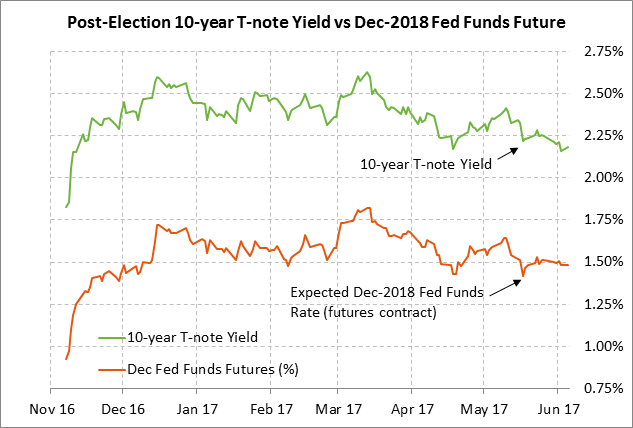

As the nearby chart shows, there is a strong correlation between the 10-year T-note yield and the Dec 2018 federal funds futures contract (which reflects the expected average federal funds rate during the month of Dec 2018). The market is currently expecting the federal funds rate to rise to only 1.485% by Dec 2018, which is only 61 bp above the current target mid-point of 0.875%. That means that after next week’s likely +25 bp rate hike, the market is expecting only another 1-1/2 rate hikes over the next 1-1/2 years. Expectations for 1-1/2 rate more rate hikes is far less than the Fed’s forecast of four more rate hikes by the end of 2018 (one more in 2017 and three in 2018).

We look for the 10-year T-note yield over the near-term to remain near the lower end of its post-election range. Yields could move even lower if (1) the U.S. economy produces more disappointing economic data, or (2) if there is some sudden safe-haven demand tied to a big sell-off in stocks, new Washington political uncertainty, or overseas turmoil. However, we suspect that yields could rise mildly over the next few months if the U.S. economy regains some momentum and if the Fed indicates that it remains on track for its third rate hike by September or December. T-note yields could also move higher if the market starts to get nervous about the Fed’s balance sheet reduction program of if Republicans start to coalesce around a large tax reform bill.