- Weekly U.S. market focus

- U.S. unemployment report has only minor consequences for Fed policy

- ISM non-manufacturing index expected to remain strong

- U.S. factory orders expected to edge lower

- U.S. stocks and T-notes post new highs after tepid payroll report

Weekly U.S. market focus — The U.S. markets this week will mainly focus on (1) Washington as Congress returns to session, and (2) next week’s FOMC meeting where a rate-hike is virtually guaranteed and there could also be some balance sheet details. This week’s U.S. economic calendar is very light with the main reports being today’s May ISM non-manufacturing index (expected -0.4) and April factory orders report (-0.2%).

Congress returns to session this week after last week’s Memorial Day recess. Congressional Republicans remain focused on a fiscal 2018 budget, an autumn debt ceiling hike, and health-care and tax-cut legislation. Former FBI Director Comey is scheduled to testify on Thursday before the Senate Intelligence Committee unless his appearance is derailed by the White House. The Trump administration this week is formally rolling out its $1 trillion infrastructure plan, which has attracted little interest from Congress. The White House today will hold an event to launch its proposal to privatize the U.S. air-traffic control system and President Trump will travel to Ohio later this week to hold an infrastructure-focused event.

Key overseas events this week include Thursday’s ECB meeting and UK general election. The ECB on Thursday is generally expected to adjust its guidance by possibly shifting to a balanced risk assessment (from a downside risk assessment) and/or dropping its reference to the possibility of lower rates. Thursday’s outcome of the UK election is expected to have the bulk of its impact on sterling, with some possible negative carry-over impact for European stocks if Conservatives do poorly and the risks rise for a disorderly Brexit.

U.S. unemployment report has only minor consequences for Fed policy — Last Friday’s May payroll report of +138,000 was substantially weaker than the consensus of +180,000. There were also downward revisions totaling -66,000 for March (to +50,000 from +79,000) and April (to +174,000 from +211,000). The 3-month payroll average is now only +121,000. The May unemployment rate fell to a new 16-year low of 4.3% but that decline was due mainly to a shrinkage of the workforce rather than a surge in jobs.

The markets were not alarmed by last Friday’s weak May payroll report since (1) the payroll report in May can be volatile due to the difficulty of adjusting for the end of the school year, and (2) job growth is expected to slow somewhat from recent levels as the economy nears full employment.

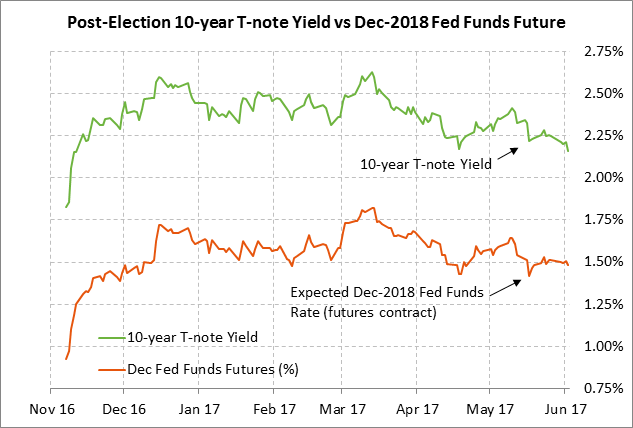

Last Friday’s payroll report had virtually no impact on market expectations that the FOMC at its meeting next week will raise its federal funds target range by +25 bp to 1.00-1.25%. The market is still discounting the chances for a rate hike next week at 100%. The odds were little changed at 34% for a rate hike by September and 60% by December.

However, the weak payroll report did cause the market to slightly reduce the chances for Fed rate hikes in 2018-19. The federal funds futures curve last Friday turned more dovish by -2 bp for Dec 2018 and by -4 bp for Dec 2019. The market is now expecting the federal funds rate to be 1.67% in Dec 2019, which is up by +79 bp from the current mid-point target of 0.875% but -133 bp short of the Fed’s goal of pushing the funds rate up to 3.00% by the end of 2019.

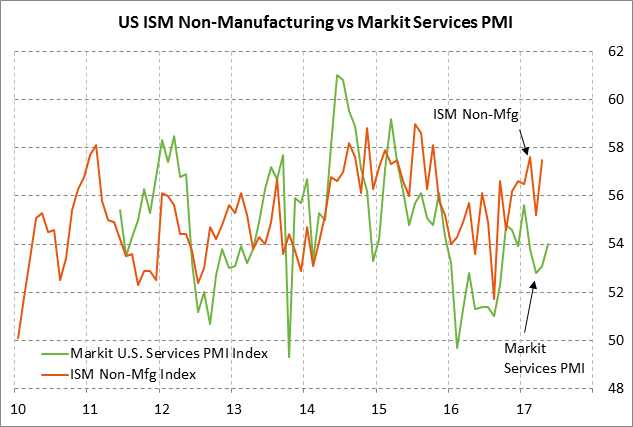

ISM non-manufacturing index expected to remain strong — The consensus for today’s May ISM non-manufacturing PMI is for a -0.4 point decline to 57.1, giving back a little of April’s large +2.3 point gain to 57.5. The non-manufacturing PMI in April was in strong shape at only -0.1 point below the 13-month high of 57.6 posted in February. Markit’s preliminary-May U.S. services PMI rose by +0.9 points to 54.0, which was a positive signal for today’s ISM report. Last Thursday’s May ISM manufacturing index rose by +0.1 point to 54.9 and was a little stronger than the consensus for an unchanged report.

U.S. factory orders expected to edge lower — The consensus for today’s April factory orders report is for a small -0.2% decline, reversing part of March’s +0.5% gain. Factory orders ex-transportation have improved substantially and have not shown a monthly decline in over a year. On a year-on-year basis, March factory orders were up +6.3% y/y and factory orders ex-transportation were up +6.5% y/y.

U.S. stocks and T-notes post new highs after tepid payroll report — The S&P 500 index last Friday rallied to a new record high and closed the day up +0.37%. Meanwhile, June 10-year T-note futures posted a new 6-3/4 month nearest-futures high. The 10-year T-note yield fell to a new 6-3/4 year low of 2.14% and closed the day down -5 bp at 2.16%.

Stock and T-note prices were supported by ideas that last Friday’s weak payroll report means the Fed may be less aggressive than earlier thought with its rate-hike regime. Friday’s cooler payroll report, along with the tepid +2.5% y/y increase in May average hourly earnings, pushed inflation expectations lower, also providing a boost to T-note prices and by extension to stock prices. The 10-year breakeven inflation expectations rate last Friday fell by -2.1 bp to 1.818%, which is just +4 bp above the mid-May 7-month low of 1.778%.

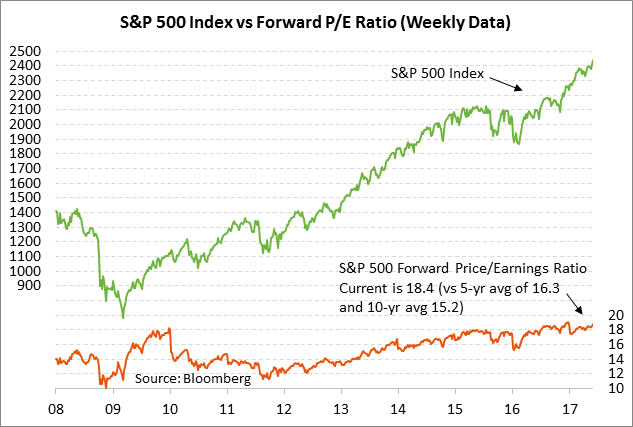

The U.S. stock market has rallied sharply in the past two weeks on continued support from strong 2017-18 earnings expectations along with a cooler outlook for U.S. interest rates. The market is also still holding out some hopes for at least a modest-sized tax cut and some infrastructure spending. However, the 2-week rally has also pushed the S&P 500 forward P/E ratio up to 18.76, which is well above the 5-year average of 16.3 and the 10-year average of 15.2.