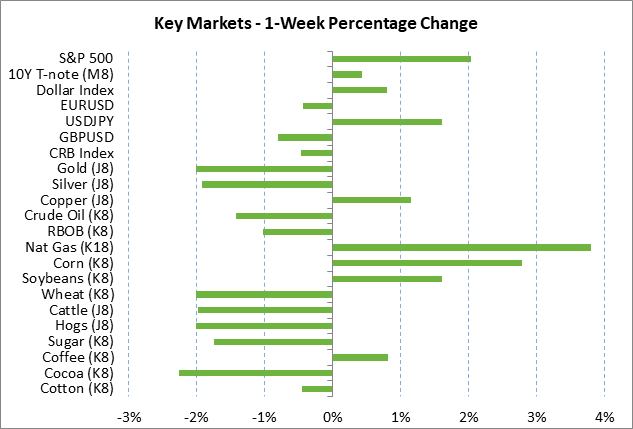

- Weekly global market focus

- Crunch time is approaching for Trump administration’s Chinese tariffs

- U.S. stocks remain vulnerable to trade and tech woes while T-notes gain on uncertainty

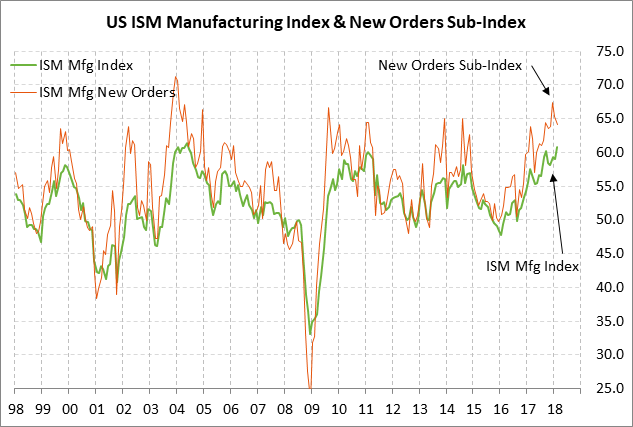

- U.S. ISM manufacturing index expected to show continued strong manufacturing confidence

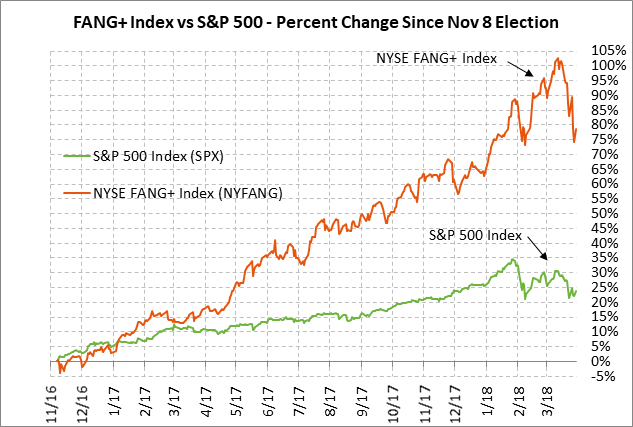

Weekly global market focus — The U.S. markets this week will focus on (1) any fresh trade tensions as the list of $50 billion worth of Chinese products subject to U.S. tariffs is due to be released by Friday, (2) tech stocks after the Nymex FANG+ index plunged by an overall -11.2% over the last two weeks versus the smaller -3.9% sell-off in the S&P 500 index, (3) a busy week for Fed speakers as the market continues to assess the odds for four rate hikes in 2018 versus the Fed-dot forecast for only three rate hikes, (4) anticipation of Q1 earnings season, which begins next week, (5) this week’s U.S. economic calendar which is capped by Friday’s March unemployment report, and (6) geopolitics as the markets wait to see how North Korea reacts as the U.S. and South Korea on Sunday began their annual military exercises.

In Europe, the markets are closed today for the Easter Monday holiday. The European markets are looking ahead to Wednesday’s March Eurozone CPI, which is expected to edge higher to +1.4% y/y from Feb’s +1.2%, although the core CPI is expected to rise to only +1.1% y/y from Feb’s +1.0% and remain far below the ECB’s inflation target of just under +2%.

Italian President Mattarella on Tuesday is expected to begin talks with the major Italian political parties to gauge which party or coalition should be given the first chance to try to form a government. Forza Italia leader Berlusconi last week expressed some willingness for his center-right coalition, led by the League, to discuss a possible coalition government with Five Star. The markets would not be happy about a populist government formed by the League and Five Star, but would be partially appeased if the establishment Forza Italia party is included in the coalition and acts as an anchor to keep the coalition from adopting extreme policies.

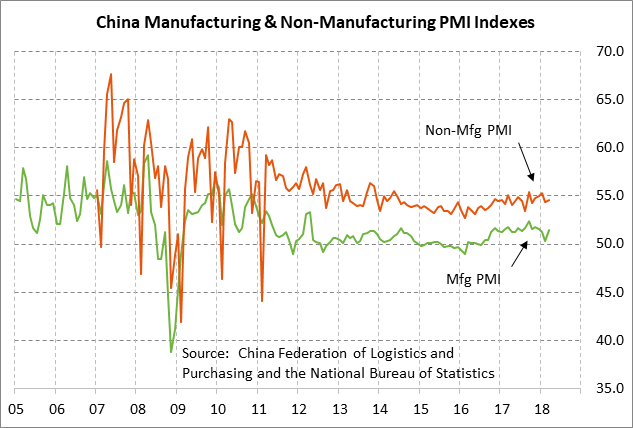

The Asian markets on Monday will initially focus on the weekend Chinese PMI reports and Sunday night’s Japanese Tankan report. Friday night’s Chinese PMI report was supportive since the Chinese March manufacturing PMI rose by +1.2 points to 51.5, which was substantially stronger than market expectations of +0.3 to 50.6. Te strong March report overcame Feb’s -1.0 point decline and indicated that Chinese manufacturing confidence improved despite U.S. tariff threats and the strong yuan. Friday night’s March non-manufacturing PMI rose by +0.2 points to 54.6, which was in line with market expectations and left the index at a solid level.

Crunch time is approaching for Trump administration’s Chinese tariffs — U.S. Trade Representative Lighthizer has until this Friday (April 6) to release the exact list of $50 billion of Chinese products that will be subject to U.S. tariffs. However, Mr. Lighthizer might well announce the list of products sooner than Friday. After the proposed list is released, there will then be a 30-day public comment period. After the comment period, Mr. Lighthizer could announce a final tariff plan at basically anytime. The schedule means that there is still time for a negotiated solution. The U.S. stock market early last week stabilized somewhat after Treasury Secretary Mnuchin said he was “cautiously hopeful” for a negotiated solution.

China has yet to announce any retaliatory measures for the Trump administration’s announcement of tariffs on $50 billion of Chinese goods for IP violations, although such an announcement could come at any time if China sees little hope for negotiations. China has so far announced only a relatively small package of tariffs on $3 billion of U.S. goods in retaliation for U.S. tariffs on steel and aluminum imports.

The Trump administration’s temporary exemption from tariffs on U.S. steel and aluminum imports for a long list of countries including Europe will last until only May 1. That means those countries have only another month to provide enough concessions to the Trump administration to be permanently exempted from the tariffs.

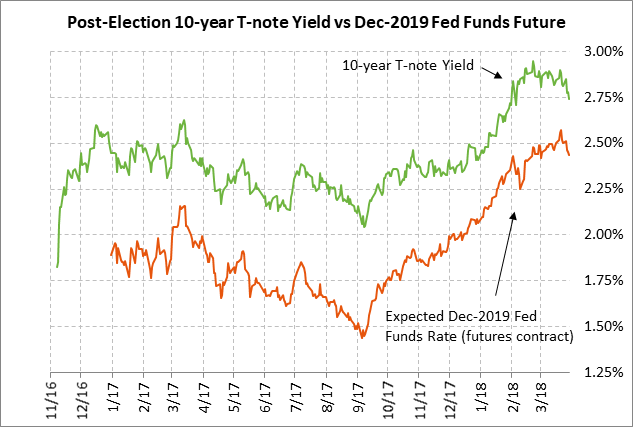

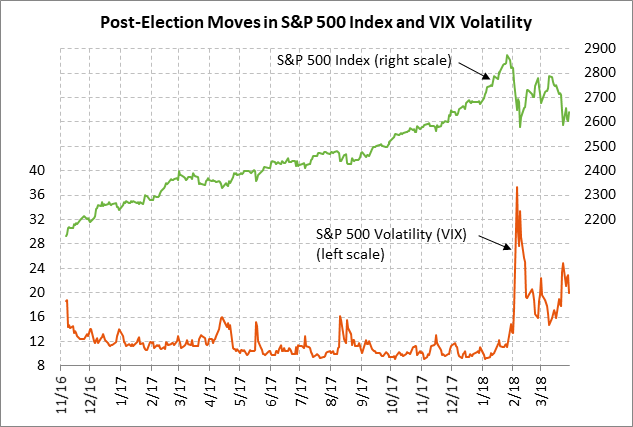

U.S. stocks remain vulnerable to trade and tech woes while T-notes gain on uncertainty — The U.S. stock market stabilized last Thursday but remains vulnerable to the recent bearish factors including trade tensions and tech woes. Tech stocks in the past two weeks have been pummeled by (1) concern about the Trump administration’s plan to block Chinese investment in high-tech U.S. industries, (2) increased concern about tech regulation after the Facebook privacy breech and the recent autonomous car crashes, and (3) heavy long liquidation pressures. Trade tension are likely to continue this week with President Trump on Sunday tweeting that he will cancel NAFTA if Mexico doesn’t do more to secure the border and stop drug flows. There are only 7 of the S&P 500 companies that report earnings this week. Meanwhile, T-note prices rallied to a 1-3/4 month high last week due to the stock market uncertainty, combined with a -13 bp reduction of Fed rate-hike expectations through 2019.

U.S. ISM manufacturing index expected to show continued strong manufacturing confidence — The market consensus is for today’s Mar ISM manufacturing index to show a -0.8 point decline to 60.0, reversing part of Feb’s +1.7 point increase to a new 14-year high of 60.8. Feb’s 14-year high in the ISM index illustrates the strong confidence among U.S. manufacturing executives. Helping the outlook, order flows have been strong with the Feb manufacturing new-orders sub-index at 64.2.

Meanwhile, the March ISM manufacturing employment sub-index in February surged by +5.5 points to 59.7, which was only -0.1 point below the 6-3/4 year high of 59.8 posted in late 2017. The strong employment index is positive for manufacturing hiring. Indeed, this Friday’s March manufacturing payroll report is expected to show a solid +24,000 increase, adding to Feb’s +31,000 increase.