- Cohn resignation does not bode well for U.S. trade tensions

- Fed Beige Book expected to find continued solid U.S. economic growth

- U.S. ADP report is expected to show a solid increase

- U.S. trade deficit expected to expand to a 9-year high

Cohn resignation does not bode well for U.S. trade tensions — White House economic advisor Gary Cohn late Tuesday resigned from the White House over President Trump’s insistence on steel and aluminum tariffs. Mr. Cohn’s departure leaves Treasury Secretary Mnuchin as the only Wall Street voice of moderation on trade left in the White House. March S&P E-mini futures late Tuesday afternoon fell more than -1% on the Cohn news.

President Trump is now likely to pursue the harder line on trade that he prefers, with encouragement from trade-hawk advisors such as Commerce Secretary Wilbur Ross and White House trade advisor Peter Navarro. White House trade policy in the past few weeks had already became more chaotic after the departure of White House staff secretary Rob Porter. While he was in the White House, Mr. Porter had been organizing weekly trade meetings to try to keep trade policy on more of an even keel.

Aside from steel and aluminum tariffs, the markets are worried that Mr. Trump may lash out at China over intellectual property and perhaps also go through with his threat to unilaterally withdraw from NAFTA. Indeed, Bloomberg Tuesday afternoon reported that the Trump administration is considering tariffs on a broad range of Chinese imports and a clamp-down on Chinese investments in the U.S. as punishment for the theft of intellectual property. The markets are also worried that Mr. Trump might make good on his threat to slap tariffs on European cars if Europe retaliates for the U.S. steel and aluminum tariffs.

Fed Beige Book expected to find continued solid U.S. economic growth — The Fed today will release its Beige Book survey of the U.S. regional economies ahead of the FOMC meeting in about two weeks on March 20-21. The Fed’s last Beige Book, released on Jan 17, found a fairly optimistic picture where 11 of the districts reported “modest to moderate gains” and the Dallas district reported a “robust” increase. The report added that, “The outlook for 2018 remains optimistic for a majority of contacts across the country.”

The market is looking for strong GDP growth in 2018 of +2.7% (up from +2.3% in 2017) due to tax cuts, continued strong consumer spending, improved business investment, and the synchronized global economic expansion.

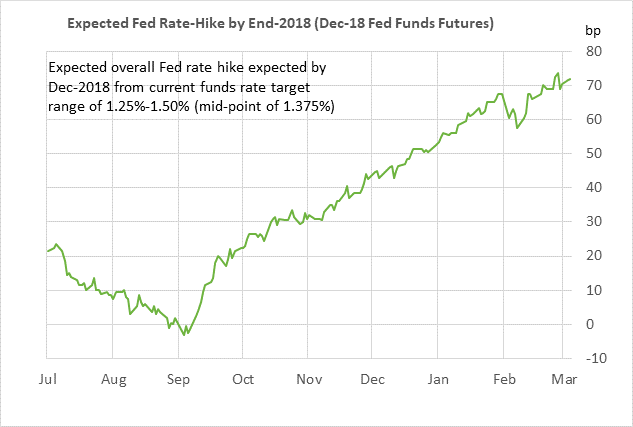

The market is discounting a 100% chance of a Fed rate hike at the upcoming FOMC meeting on March 20-21, according to the federal funds futures market. For all of 2018, the market is discounting a total of +72.0 bp worth of rate hikes, which would translate to 2.9 rate hikes and would be very close to the Fed-dot forecast for 3 rate hikes. Expectations for the overall 2018 rate hike peaked at 73.5 bp last Wednesday but then fell back when the stock market plunged on President Trump’s announcement on Thursday of his steel and aluminum tariffs.

Since a rate hike is essentially a done deal for the FOMC meeting in two weeks, the markets are mainly waiting to see if FOMC members at that meeting will boost their Fed-dot forecasts for the funds rate target for the next 1-3 years. Fed Chair Powell in his recent Congressional testimony said that the U.S. economic and inflation outlooks are stronger now than they were at the December FOMC meeting when the Fed issued its last forecasts. That led to some speculation that FOMC members might boost their median expectation for rate hikes this year above the current level of three rate hikes.

U.S. ADP report is expected to show a solid increase — The market consensus is for today’s Feb ADP report to show a solid increase of +200,000 following the Jan report of +234,000. Today’s expected report of +200,000 would be slightly below the 12-month trend average of +213,000. On the labor front, the markets are mainly looking ahead to Friday’s Feb payroll report, which is expected to be solid at +200,000 as well. The consensus is for the Feb unemployment rate to fall by -0.1 point to a new 17-year low of 4.0%.

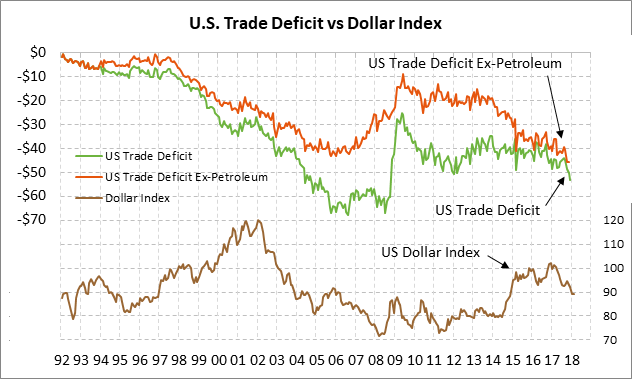

U.S. trade deficit expected to expand to a 9-year high — The market consensus is for today’s Jan trade deficit to expand to -$55.1 billion from Dec’s -$53.1 billion. The deficit in December already widened to the highest level in more than nine years and today’s expected report would represent another new 9-year high. Today’s expected 9-year high in the U.S. deficit could cause President Trump to lash out even more on trade since the deficit is now widening on his watch.

The good news on trade is that U.S. exports in December reached a new record high and were up sharply by +7.3% y/y. However, the bad news for the trade deficit was that the strong U.S. economy sucked in even more imports. Import growth in December of +9.5% y/y easily outstripped the export growth of +7.3% y/y, leading to the wider deficit.

The U.S. trade deficit with China in December fell to -$30.8 billion from the 2-1/4 year high of -$35.4 billion seen in November. However, the 12-month moving average of the U.S. trade deficit with China rose to a new record high of -$31.3 billion in December, which can only increase President Trump’s ire.

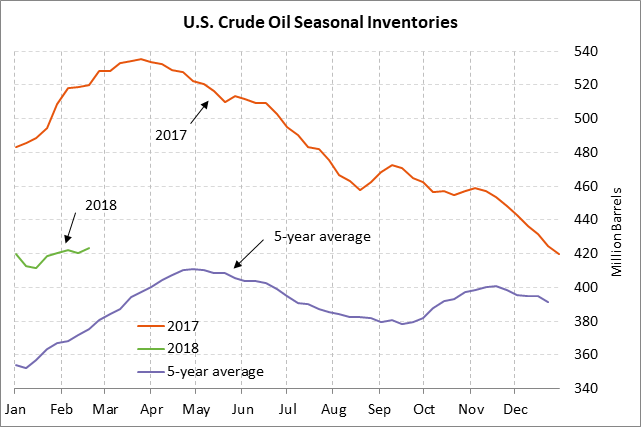

Weekly EIA report — The consensus for today’s weekly EIA report is for a +3.0 million bbl rise in U.S. crude oil inventories, a +1.75 million bbl rise in gasoline inventories, a -750,000 bbl decline in distillate inventories, and a -0.4 point decline in the refinery utilization rate to 87.4%. Crude oil prices fell on Tuesday after the API report that U.S. crude oil inventories last week rose by a hefty +5.66 million bbls. U.S. crude oil inventories are currently only +2.0% above the 5-year average, the tightest level in more than 3 years.