- China launches new stimulus measures as Trump continues verbal pressure

- U.S. May core CPI expected to remain tame

- 10-year T-note yield remains near 1-3/4 year low ahead of today’s auction

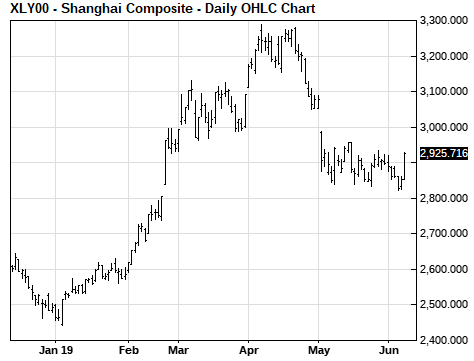

China launches new stimulus measures as Trump continues verbal pressure — China seems to be rather pessimistic about a trade deal since China continues to find ways to stimulate its economy to offset the negative effects of the trade war. China on Tuesday announced a new infrastructure initiative by allowing local governments expanded access to special bond proceeds to finance new infrastructure projects. That added to the tax cuts that China has been using to stimulate spending.

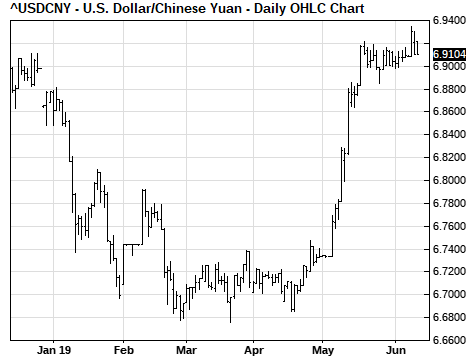

The Chinese markets were also encouraged that the PBOC on Tuesday set a daily fix for the yuan that was stronger than expected, which was a show of defense for the yuan. The Chinese yuan on Tuesday rallied by +0.28%, mostly reversing Monday’s -0.31% decline to a 6-month low. The yuan’s current level of 6.9114 yuan/USD is 1.0% above last November’s 11-year low of 6.9799 and is 1.3% above the psychological level of 7 yuan/USD. The PBOC may step up its defense of the yuan to ensure that it doesn’t breach the 7 yuan/USD level, at least not before the G-20 meeting at the end of June.

Tuesday’s combination of infrastructure stimulus and the defense of the yuan sparked a sharp rally in Chinese stocks. The Shanghai Composite Index on Tuesday rallied to a new 1-1/2 week high and closed the day sharply higher by +2.58%.

China on Tuesday seemed to needle President Trump when a Chinese Foreign Ministry official once again refused to confirm a Trump-Xi meeting. He said that the U.S. has publicly referred numerous times to a Trump-Xi meeting at the end of June but that, “If we have information we will release it in due time.”

China’s slow-walking of a confirmation of a Trump-Xi meeting has drawn some outbursts from Mr. Trump this week. Mr. Trump on Monday said that he would immediately place the 25% tariffs on $300 billion of Chinese goods if President Xi does not meet with him at the G-20 meeting. On Tuesday, Mr. Trump said that he was the one holding up a US/Chinese trade deal and that there would be no deal until China goes back to its original negotiating position.

The markets continue to hope that Presidents Trump and Xi will meet in late June and get the trade talks back on track. However, China is digging in its heels on its red lines and seems to be waiting for some movement in its direction from the U.S. Meanwhile, time is running out for the Trump administration since the presidential campaign season is coming up fast, as well as the end of Mr. Trump’s first term in January 2021. That may encourage Mr. Trump to take even more dramatic tariff and blacklisting action soon to try to force China to capitulate before time runs out.

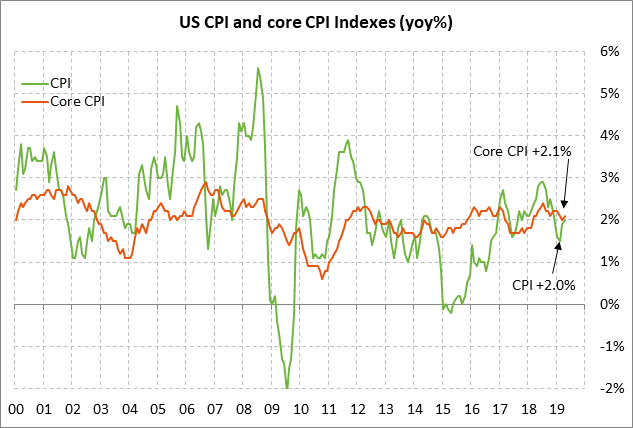

U.S. May core CPI expected to remain tame — The market consensus is for today’s May CPI to ease to +1.9% y/y from April’s +2.0% and the core CPI to be unchanged at +2.1% y/y. The CPI in the past three months has weakened a bit as seen by the fact that the April CPI was up by only +1.6% on a 3-month annualized basis. The headline CPI will be headed lower in coming months due to the 20% plunge in oil prices seen over the past five weeks, which means the markets will be focused even more than usual on the core CPI.

The markets will be closely watching the inflation statistics over the next few months since weaker-than-expected inflation figures would give the Fed a stronger pretext to execute the easing moves that the markets believe are necessary. The federal funds futures market is currently discounting the chances of a Fed rate cut at 21% for next week’s FOMC meeting (June 18-19) and at 76% for the following meeting on July 30-31.

The Fed’s preferred inflation measure, the PCE deflator, was at only +1.5% y/y in April and the core deflator was at +1.6% y/y, both comfortably below the Fed’s +2.0% inflation target.

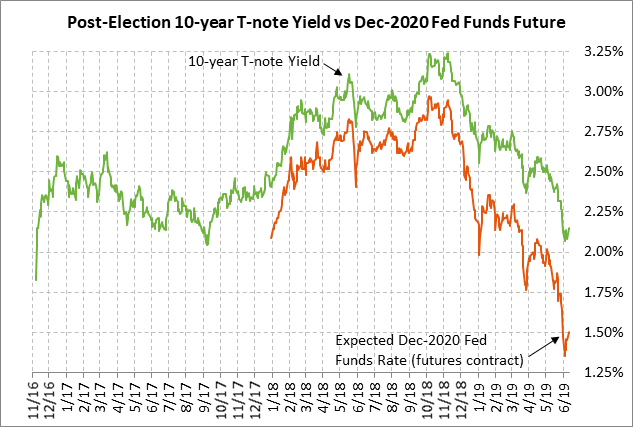

10-year T-note yield remains near 1-3/4 year low ahead of today’s auction — The Treasury today will sell $24 billion of 10-year T-notes in the first reopening of May’s 2-3/8% 10-year T-note of May 2029. The Treasury will then conclude this week’s $78 billion coupon package by selling $16 billion of reopened 30-year bonds on Thursday.

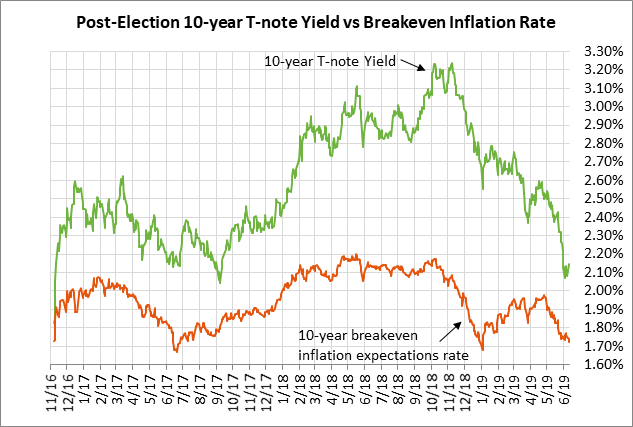

The benchmark 10-year T-note yield on Tuesday rose to a new 1-1/2 week high but then fell back to close the day slightly lower. The current 10-year T-note yield of 2.14% is just mildly above last week’s 5-month 1-3/4 year low of 2.05%.

The 10-year T-note yield has plunged by about -50 bp in the past two months due to (1) the sharp dovish turn in Fed expectations where the markets are expecting -85 bp of easing through the end of 2020, (2) expectations of weaker U.S. and global economic growth due to trade tensions, and (3) the sharp drop in inflation expectations that has been prompted mainly by the -20% sell-off in crude oil prices in the past five weeks. The 10-year breakeven inflation expectations rate has plunged by -26 bp April and is currently at 1.72%, just mildly above the late-May 5-month low.

The 12-auction averages for the 10-year are as follows: 2.48 bid cover ratio, $19 million in non-competitive bids, 4.2 bp tail to the median yield, 24.7 bp tail to the low yield, and 42% taken at the high yield. The 10-year is mildly above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.9% of the last twelve 10-year T-note auctions, which is mildly above the median of 61.0% for all recent Treasury coupons.