- More attractive valuation provides some stock market support

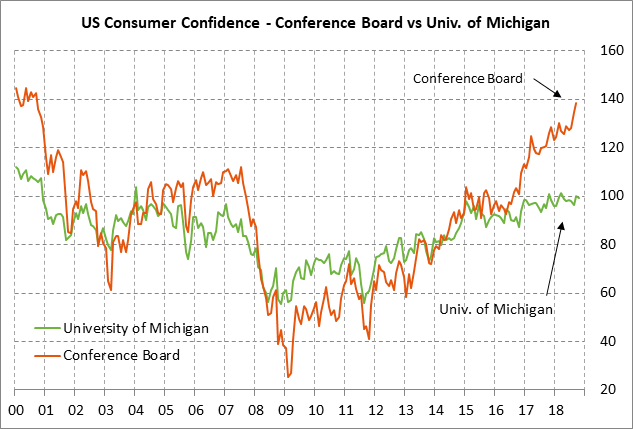

- U.S. consumer sentiment expected steady despite potential clouds

More attractive valuation provides some stock market support — The S&P 500 index on Thursday rebounded higher from Wednesday’s 6-month low and closed the day up +1.86%. While the index remains near the lower end of its sharp 3-week sell-off, Thursday’s recovery rally gave the market at least a temporary respite.

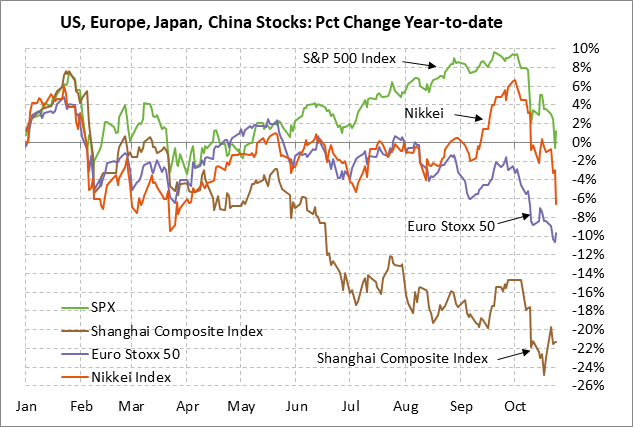

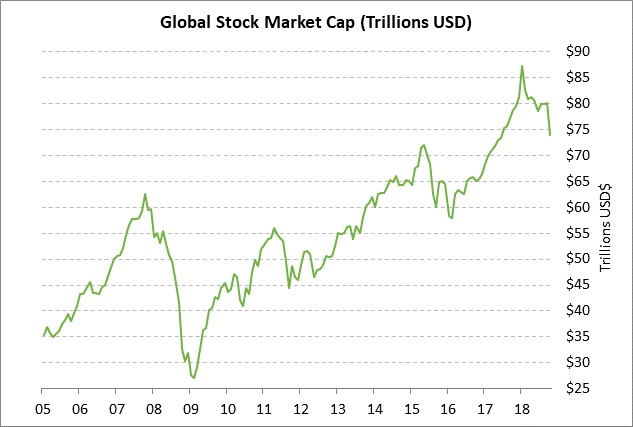

This week’s gyrations have left the global markets mixed on the week through Thursday: S&P 500 -2.1%, Euro Stoxx 50 -1.4%, Nikkei -5.6%, and Shanghai Composite +2.1%. In recent weeks, the world’s main stock markets have all shown sharp sell-offs from their recent respective highs totaling: S&P 500 index -9.8%, Euro Stoxx 50 -16.2%, Nikkei -13.3%, Shanghai Composite -31.7%. Total world stock market capitalization has plunged by -$6.2 trillion (-8%) just in the past three weeks and by an overall -$13.4 trillion (-15%) since the record high in January.

Bearish factors for U.S. stocks include (1) the Fed’s current intent for another 125 bp of rate hikes (based on the Fed dot forecasts), which is 50 bp more than market expectations of about +75 bp, (2) expectations for U.S. earnings growth to ease in coming quarters as the tax-cut effects dissipate, (3) concern about the recent spate of profit margin warnings due to weaker Chinese sales and higher costs from tariffs, materials and freight, (4) the slowing Chinese economy and worries about worsening US/Chinese trade relations, (5) ongoing strength in the dollar, and (6) the vitriolic U.S. political climate and uncertainty about the upcoming Nov 6 mid-term election.

However, there are some positives that are providing some underlying support for stocks that include (1) more attractive valuation levels, and (2) reduced trade tensions after the recent NAFTA 2.0 agreement and after the US/EU and US/Japan agreed to negotiations and a ceasefire on any new tariffs.

US/Chinese trade relations continue to be a major sore spot for the global markets since there aren’t even any negotiations at present. In addition, the U.S. is scheduled to ratchet up its tariffs on $200 billion of Chinese goods on Jan 1 to 25% from 10%, and President Trump at any time could announce tariffs on the remaining $267 billion of Chinese goods. However, there is some hope that the U.S. and China might engage in serious negotiations after the Nov 6 mid-term elections. It would be highly supportive for the global markets if the U.S. and China could get past the acrimony and agree on an overarching trade deal that includes dropping the current penalty tariffs. While a near-term agreement is unlikely, President Trump may be feeling some pressure from the recent weakness in the U.S. stock market and he might be more amenable to a US/Chinese trade deal after the mid-term elections.

U.S. stocks are also seeing some support from more attractive valuation levels and the fact that the market is still expecting strong earnings growth in coming quarters. The SPX forward P/E (based on 2018 earnings) has fallen to 16.6 from 20 early this year. The current forward P/E is well below the 5-year average of 17.5, although it is still above the 10-year average of 15.7.

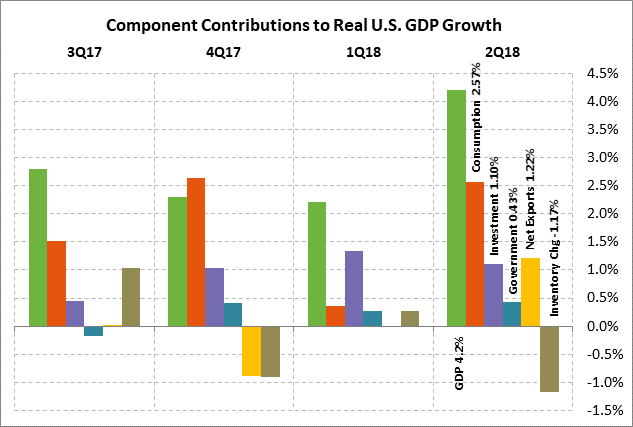

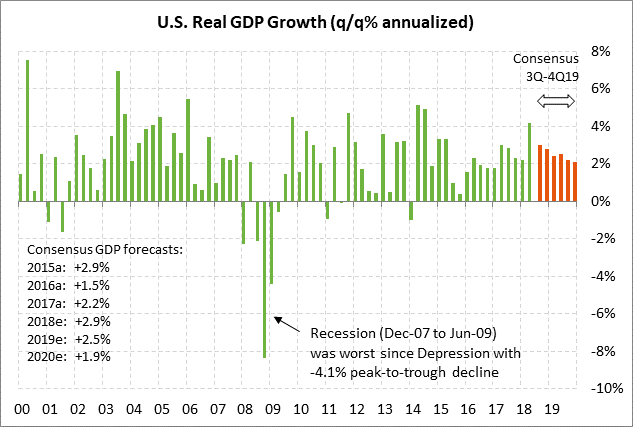

U.S. Q3 GDP expected to remain strong at +3.3% — The market consensus is for today’s Q3 GDP to downshift to +3.3% (q/q annualized) from Q2’s stellar pace of +4.2%. The Q2 GDP pace of +4.2% is clearly unsustainable and was artificially boosted by a recovery from Q1’s weak report of +2.2%. Nevertheless, today’s expected Q3 GDP report of +3.3% would be an impressive growth figure that is well above the Fed’s estimate of long-term growth potential near +1.8%.

U.S. GDP in Q3 continued to receive a strong fiscal stimulus boost from the massive Jan 1 tax cuts and increased government spending. Consumers have been spending their tax-cut money and businesses are using at least some of their tax cut money for investment and expansion.

However, the tax cuts are expected to fade in coming quarters, thus leading to more realistic GDP figures. In fact, the market consensus is for U.S. GDP to downshift to +2.7% in Q4 and +2.4% in Q1. On a calendar basis, the consensus is for U.S. GDP to downshift from +2.9% in 2018 to +2.5% in 2019 and +1.9% in 2020.

In any case, personal spending is expected to again be a big contributor to Q3 GDP with a +3.3% increase in personal consumption, down from Q2’s +3.8% but still a very strong figure. Personal spending contributed 2.57 points of Q2’s GDP figure of +4.2%, accounting for more than half of overall growth. Still, the U.S. economy was firing on all cylinders in Q2 with investment contributing 1.10 points to GDP, government contributing 0.43 points, and net exports contributing 1.2 points. The only negative category was inventories, which subtracted 1.17 points from Q2 GDP.

U.S. consumer sentiment expected steady despite potential clouds — The market consensus is for today’s final-Oct University of Michigan U.S. consumer sentiment index to be unchanged from the preliminary-Oct level of 99.0, leaving the index down by -1.1 from September. U.S. consumer sentiment remains in strong shape at only 2.4 points below March’s 15-year high of 101.4.

U.S. consumer sentiment is seeing support from (1) the strong U.S. economy, (2) the strong U.S. labor market and confidence about the job outlook, and (3) the continued rise in home prices, which is boosting household wealth. However, there are some clouds on the horizon that include (1) the downside correction in stocks that could be taken by some consumers as a negative indicator for the economy, (2) rising interest rates and mortgage rates, and (3) the vitriolic political climate in Washington and uncertainty about the upcoming Nov 6 mid-term elections.