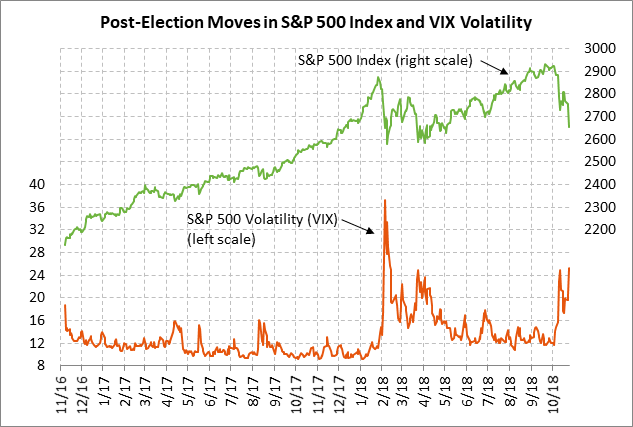

- VIX pops up to 8-1/2 month closing high while SPX falls to 6-month low

- ECB will keep moving towards normalization despite near-term threats

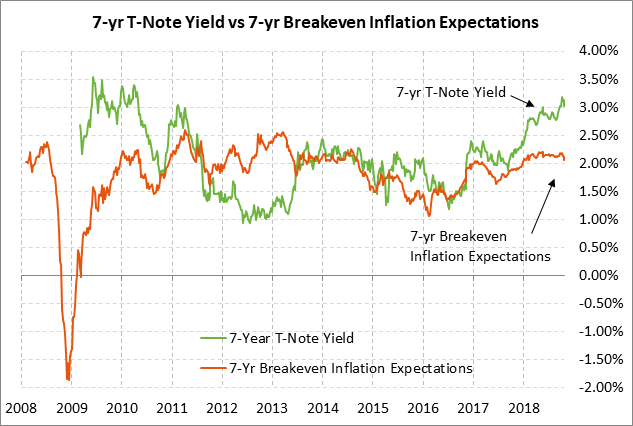

- 7-year T-note yield hovers just above 3%

VIX pops up to 8-1/2 month closing high while SPX falls to 6-month low — The S&P 500 index on Wednesday plunged to a new 6-month low and closed the day down -3.09% at 2656.10. The S&P 500 index has now fallen by a total of -9.83% from September’s record high, stopping just above the -10% correction level of 2646.82.

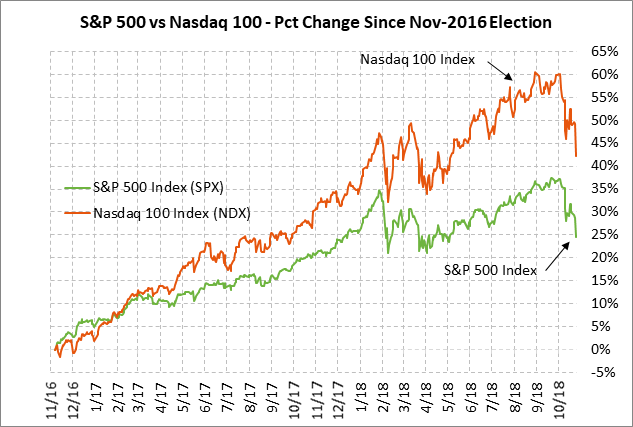

The Nasdaq 100 index was even weaker, closing the day sharply lower by -4.63% and correcting lower by a total of -11.99% from the Oct 1 record high. FANG stocks led the market lower with the Nymex FANG+ index closing the day down -5.39%.

Meanwhile, the VIX index closed +4.52 at 25.23%, which was the highest close in 8-1/2 months although below the 8-1/2 month intra-day high of 28.84% posted on Oct 11. The current VIX level is more than twice as high as the average of about 13% seen in September when stocks were making new record highs. However, the current VIX level of 25.23% remains far below the high of about 50% posted this past February when the stock market saw its first big downside correction.

Bearish factors for stocks included (1) the Fed’s recent hawkish talk about raising the funds rate above the neutral rate, which implies another +125 bp of rate hikes (versus market expectations of a little over +75 bp), (2) the sustained rise in the 10-year T-note yield above 3% seen in the past few weeks, (3) concern about peak earnings and the recent spate of profit margin warnings caused by higher tariff and freight costs and slower demand from China, and (4) concern about deteriorating US/Chinese trade relations and the slowing Chinese economy. There is also the possibility of increased Washington political strife after the Nov 6 mid-term election if Democrats gain control of the House along with its investigatory committees and if President Trump fires any top Justice Dept officials with an intent to impede the Mueller investigation.

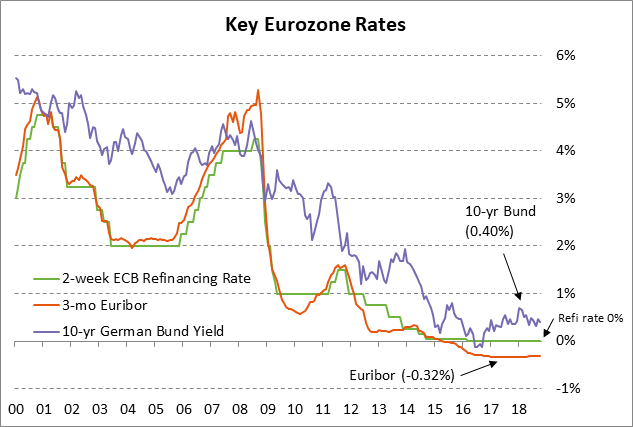

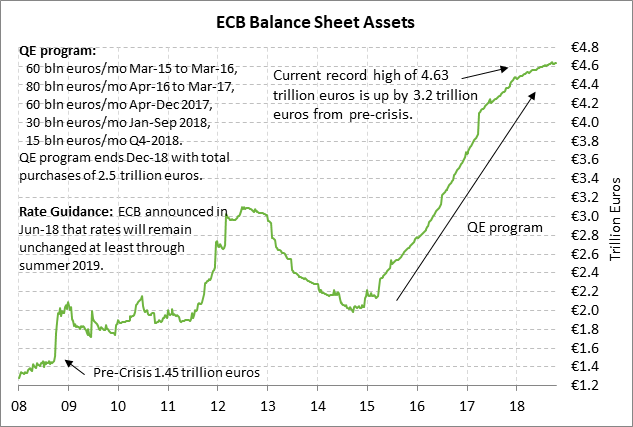

ECB will keep moving towards normalization despite near-term threats — The ECB at its meeting today is unanimously expected to leave its key policy variables unchanged. Meanwhile, ECB President Draghi in his post-meeting news conference will likely portray an air of confidence in the ECB’s plan for normalization despite the recent threats.

Those near-term threats include (1) global stock market weakness, (2) the surge in Italian bond yields and the showdown between the European Commission and the populist Italian government over Italy’s 2019 budget, (3) trade tensions with the shaky US/EU truce and with the U.S. tariffs on European steel and aluminum, and (4) increased concern about a hard Brexit as the EU and UK have been unable to agree on exit terms.

The ECB is also contending with some emerging economic weakness highlighted by Wednesday’s disappointing PMI figures. The Oct Eurozone manufacturing PMI fell by -1.1 points to a 2-1/4 year low of 52.1, showing its third consecutive monthly decline and its ninth decline in the last ten months. Meanwhile, the Oct Eurozone services PMI fell by -1.4 points to a 2-year low of 53.3. Both PMIs remained above the boom-bust level of 50.0 but nevertheless illustrated that business confidence has sagged to a 2-year low.

Yet the ECB will undoubtedly stick with its current policy course for the time being since the current threats have not yet materialized in something large enough to knock the ECB off course. The ECB ‘s current policy plan is to end its QE program at the end of 2018 and promise not to raise interest rates until after summer 2019. The market is discounting about a two-thirds chance of the ECB’s first rate hike by September 2019. The ECB’s deposit rate is currently at -0.40% and its refinancing rate is at zero.

The ECB only has two months left on its QE program, which is scheduled to end on December 31 with a balance sheet asset level near 4.66 trillion euros, up by +3.2 trillion euros from the pre-crisis level. After ending QE, the ECB will reinvest maturing portfolio proceeds, thus leaving its balance sheet asset level unchanged indefinitely. The Fed, by contrast, is not reinvesting proceeds, allowing its balance sheet to slowly decline at a maximum monthly rate of $50 billion per month. The Fed is thereby permanently draining excess reserves from the banking system.

7-year T-note yield hovers just above 3% — The Treasury today will sell $31 bln of 7-year T-notes, concluding this week’s $127 billion T-note auction package. The $31 billion size of today’s 7-year T-note auction is unchanged from the last two months but is up by $3 billion from the $28 billion size that prevailed during 2017/18.

The benchmark 7-year T-note on Wednesday fell to a 3-week low of 3.01% on continued stock market weakness but recovered a bit to close the day down -7 bp at 3.03%. The 7-year T-note yield is currently 17 bp below the early-October 8-1/2 year high of 3.20%. The 7-year T-note yield has risen very sharply by +110 bp over the past year mainly because of increased expectations for Fed tightening. The market is expecting another 78.5 bp of Fed rate hikes by the end of 2019 (i.e., 3.1 rate hikes), just below the peak of 80 bp posted in early October.

The 12-auction averages for the 7-year are as follows: 2.50 bid cover ratio, $16 million in non-competitive bids to mostly retail investors, 4.8 bp tail to the median yield, 30.8 bp tail to the low yield, and 48% taken at the high yield. The 7-year is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 63.1% of the last twelve 7-year T-note auctions, which exactly matches the median of 63.1% for all recent Treasury coupon auctions.