- Fed’s Beige Book will be watched for profit margin pressure

- U.S. new home sales are expected to dip but home prices are expected to continue higher

- 5-year T-note yield backs off on stock market weakness

- Italian bond yield remains below recent high despite European Commission’s rejection of Italy’s budget

- Weekly EIA report

Fed’s Beige Book will be watched for profit margin pressure — In the Fed’s last Beige Book, released on Sep 12, the staff found that “the economy expanded at a moderate pace through the end of August.” The markets will be watching today’s report for the usual factors of economic growth and wages. However, the markets will also watch for news of higher costs from tariffs, materials, and freight since the stock prices of several high-profile companies have recently plunged after profit margin warnings based on these factors. The last Beige Book said, “Businesses generally remained optimistic about the near-term outlook, though most Districts noted concern and uncertainty about trade tensions—particularly, though not only, among manufacturers. A number of Districts noted that such concerns had prompted some businesses to scale back or postpone capital investment.”

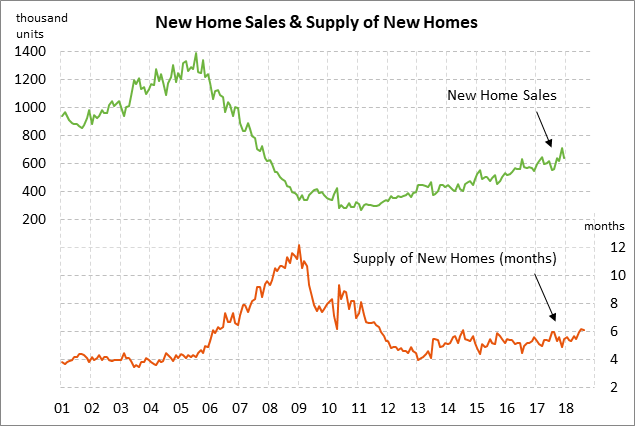

U.S. new home sales are expected to dip but home prices are expected to continue higher — The consensus is for today’s Sep new home sales report to show a -0.6% decline to 625,000, reversing part of Aug’s +3.5% increase to 629,000. New home sales this year have been bouncing around but remain in generally strong shape. However, the market is expecting a slide in sales in coming months since home affordability is at the worst level in 10 years as a result of high home prices and rising mortgage rates.

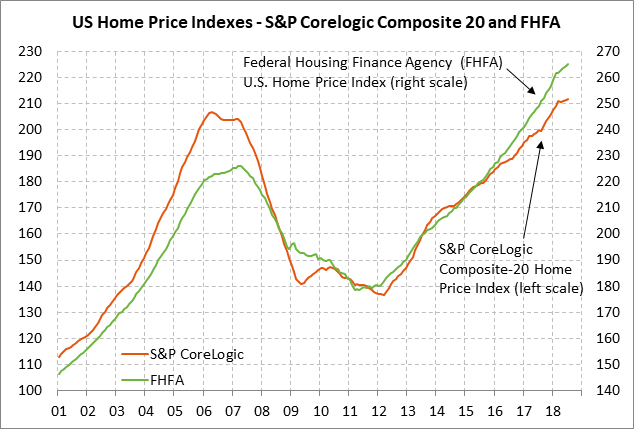

Meanwhile, today’s Aug FHFA house price index is expected to show a +0.3% m/m increase, adding to July’s increase of +0.2% m/m. The FHFA house price index hasn’t shown a decline in more than six years and has soared by a total of +48% from the post-recession low.

5-year T-note yield backs off on stock market weakness — The Treasury today will sell $39 bln of 5-year T-notes and $19 bln of 2-year floating rate notes. The $39 billion size of today’s 5-year T-note is up by $1 billion from last month’s auction and is up by $5 billion from the $34 billion size that prevailed in 2016/17. The Treasury will conclude this week’s $127 billion T-note auction package by selling $31 bln of 7-year T-notes on Thursday.

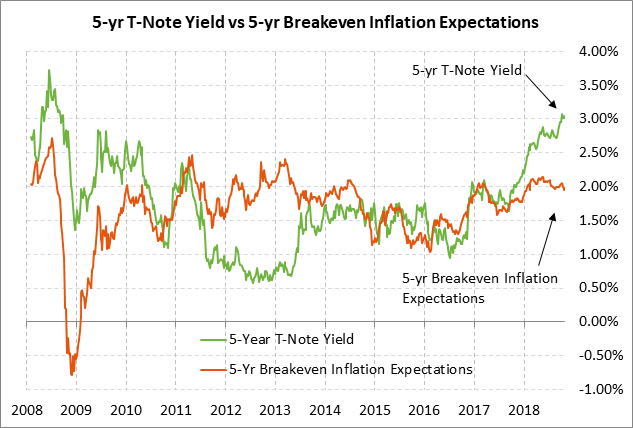

Today’s 5-year T-note issue was trading at 3.01% in when-issued trading late Tuesday afternoon. The benchmark 5-year T-note on Tuesday fell to a 3-week low of 2.96% on early stock market weakness but then rebounded higher to close the day only -4 bp lower at 3.01%. The 5-year T-note reached a 10-year high of 3.09% in early October and is currently just 8 bp below that level. The 5-year T-note yield has risen very sharply by about +135 bp over the past year mainly because of increased expectations for Fed tightening. The market is expecting another 78.5 bp of Fed rate hikes by the end of 2019 (i.e., 3.1 rate hikes), just below the peak of 80 bp posted in early October.

The 12-auction averages for the 5-year are as follows: 2.48 bid cover ratio, $49 million in non-competitive bids to mostly retail investors, 4.2 bp tail to the median yield, 19.9 bp tail to the low yield, and 50% taken at the high yield. The 5-year is mildly below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 61.8% of the last twelve 5-year T-note auctions, mildly below the median of 63.1% for all recent Treasury coupon auctions.

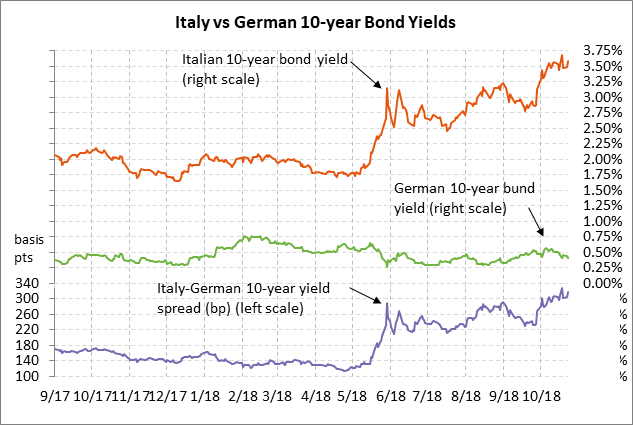

Italian bond yield remains below recent high despite European Commission’s rejection of Italy’s budget — The European Commission wasted no time in officially rejecting Italy’s budget and demanding that Italy come back with a revised budget within three weeks. Prime Minister Conte responded by saying that “There isn’t any B plan. I said that the deficit at 2.4% of GDP is the cap. I can say this will be our cap.”

The markets are waiting to see if League leader Salvini and Five Star leader Di Maio respond with a blunt refusal to compromise or whether they indicate some flexibility. The market is the only real disciplinary mechanism for Italy’s populist government since the most the Commission can do is start a dawn-out “Excessive Deficit Procedure” that might eventually result in fines for Italy.

The 10-year Italian government bond yield on Tuesday rose by +10 bp to 3.59%, but remained 9 bp below last Thursday’s 4-3/4 -year high of 3.68%. The Italian-German 10-year yield spread on Tuesday rose by +14 bp to 318, but remained 9 bp below last Thursday’s 5-1/2 year high of 327 bp.

The Italian government may try to tough it out with the current budget since the Italian-German bond yield spread on Tuesday did not soar and remained well below the 400 bp level that has become a consensus point for doom. However, if the Italian government wants the Italian bond yield to ease to more comfortable levels, it will have to come back with some type of compromise.

The markets remain nervous ahead of Friday’s release by S&P of its credit review of Italy. The markets were pleased last Friday when Moody’s reduced Italy’s credit rating by only the expected one notch and switched its outlook to “stable” from “negative,” suggesting that another downgrade is not likely soon. There is no room for another Moody’s downgrade without putting Italy’s sovereign bonds into junk territory.

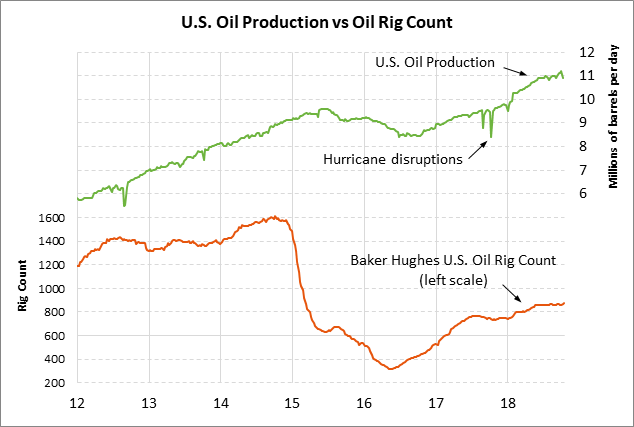

Weekly EIA report — The consensus is for today’s weekly EIA report to show a +3.0 mln bbl rise in U.S. crude oil inventories, a -1.5 mln bbl decline in gasoline inventories, a -2.0 mln decline in distillate inventories, and a +0.5 point increase in the U.S. refinery utilization rate to 89.3%. U.S. oil production in last week’s report fell by -0.3% to 10.9 mln bpd from the previous week’s record high of 11.2 mln bpd.