- China’s focus on personal tax cuts helps spark big stock rally

- European markets wait to see if the European Commission forces a showdown over the Italian budget

- 2-year T-note auction yield is at a 10-1/4 year high

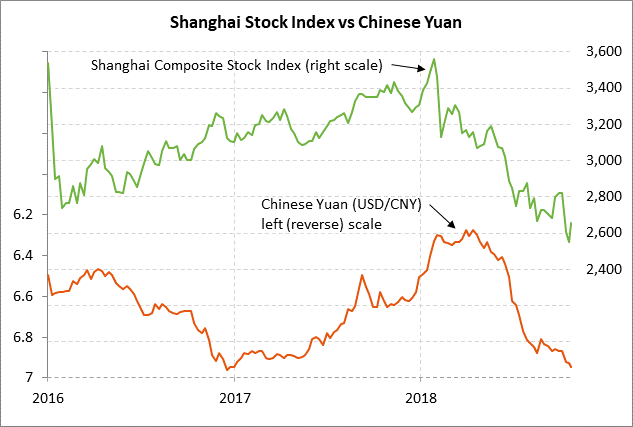

China’s focus on personal tax cuts helps spark big stock rally — The Shanghai Composite index on Monday soared by +4.09% and extended its upward rebound from last Friday’s 4-year low. Chinese stocks continued to react favorably to the Chinese government’s concerted effort last Friday to provide reassurances to the markets, particularly with the PBOC saying that it will study measures to ease financing difficulties for companies and will support bank-credit expansion. Stocks also rallied on short-covering and reports of continued buying by the national team.

But a key factor leading to Monday’s huge gain was the Chinese government’s announcement on Saturday of a plan for broad personal tax cuts, likely starting Jan 1, 2019. The markets were encouraged that the government is focusing more heavily on boosting consumer consumption and moving away from its old model of debt-driven infrastructure projects. China’s massive debt level means there isn’t room for a new surge in infrastructure spending, which isn’t even needed given the massive amount of infrastructure building that has already been seen in recent years.

The personal tax cuts will boost consumer income, confidence, and spending, and will stimulate the economy with a limited rise in the government’s budget deficit. Tax cuts will promote China’s goal of forcing consumer spending to play a bigger role in economy, thus reducing China’s traditional dependence on investment and exports. Personal tax cuts on Jan 1 would also help soften the blow if the Trump administration goes ahead with its current plan of raising the U.S. tariff to 25% from 10% on $200 billion of Chinese products. The first $50 billion batch of Chinese projects already have a 25% tariff.

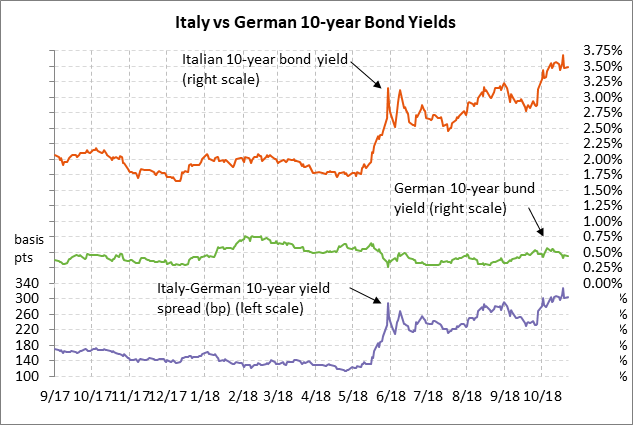

European markets wait to see if the European Commission forces a showdown over the Italian budget — EU Commissioners will meet today in Strasbourg to discuss how to respond to Italy’s budget proposal. The European Commission has until next Monday (Oct 29) to announce whether it will reject the budget as non-compliant, but the Commission could announce its decision sooner.

The European Commission clearly views Italy’s 2019 budget as non-compliant with the EU’s fiscal rules, which are tighter for Italy since its national debt of 130% of GDP is already far above the limit of 60%. However, the Commission may try to find a way to avoid an ugly showdown, which it can’t really win. The Commission has no real mechanism to force Italy to comply with its fiscal rules, except to start the drawn-out “Excessive Deficit Procedure” that might eventually result in fines for Italy. Meanwhile, Italy’s populist government has shown no sign of backing down and indeed could actually gain domestic political support if its goes to war with the EU’s bureaucrats.

Italy’s Finance Minister Tria on Monday tried to sound constructive by saying that, “We can still reassess during the budget implementation whether to contain the target so that we don’t necessarily need to reach that 2.4%.” He added that, “For sure, we won’t exceed” the deficit target of 2.4% of GDP.

The 10-year Italian government bond yield on Monday was little changed at 3.49%, which was 19 bp below last Thursday’s 4-3/4 -year high of 3.68%. The Italian-German 10-year yield spread on Monday was little changed at 304 bp, which was 23 bp below last Thursday’s 5-1/2 year high of 327 bp.

The Italian bond yield and Italian-German spread have fallen back after last Friday’s news that Moody’s switched its outlook for Italy to “stable” from “negative” after its expected one-notch downgrade to Baa3. The fact that Moody’s switched to a “stable” outlook suggested that Moody’s is not expecting another downgrade over the near-term even if Italy adopts its proposed budget. Italy’s credit rating from Moody’s is now only one notch above junk, which means there is no room for another downgrade without putting Italy’s sovereign bonds into junk territory. S&P is scheduled to release the results of its Italian credit review this Friday (Oct 26).

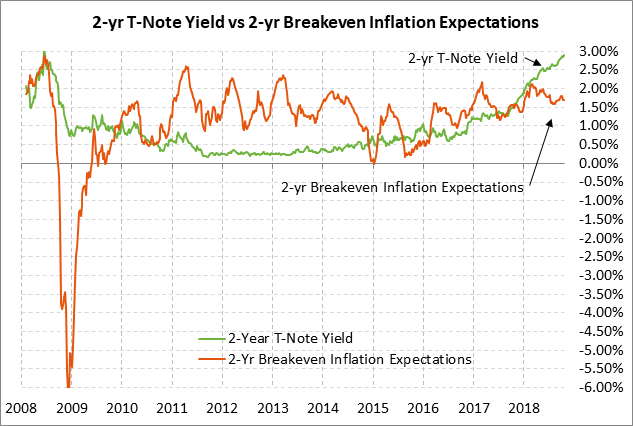

2-year T-note auction yield is at a 10-1/4 year high — The Treasury today will sell $38 billion of 2-year T-notes. The Treasury will then continue this week’s $127 billion T-note auction package by selling $39 bln of 5-year T-notes and $19 bln of 2-year floating rate notes on Wednesday, and $31 bln of 7-year T-notes on Wednesday. Today’s 2-year T-note issue was trading at 2.93% in when-issued trading late Monday afternoon.

The benchmark 2-year T-note yield on Monday edged to a new 10-1/4 year high of 2.9123% and closed the day up +0.4 bp at 2.91%. The 2-year T-note yield on Monday reached a new 10-1/4 year high as global stocks stabilized and as the market expects additional hawkish comments by Fed officials this week. The 2-year T-note yield has risen very sharply by about +160 bp over the past year mainly because of increased expectations for Fed tightening. The market is expecting another 78.5 bp of Fed rate hikes by the end of 2019 (i.e., 3.1 rate hikes), just below the peak of 80 bp posted in early October.

The 12-auction averages for the 2-year are as follows: 2.78 bid cover ratio, $310 million in non-competitive bids, 3.4 bp tail to the median yield, 27.0 bp tail to the low yield, and 68% taken at the high yield. The 2-year is the least popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of only 44.3% of the last twelve 2-year T-note auctions, which is well below the median of 63.1% for all recent Treasury coupon auctions.