- Weekly global market focus

- 10-year T-note yield consolidates below last week’s 7-1/3 year high

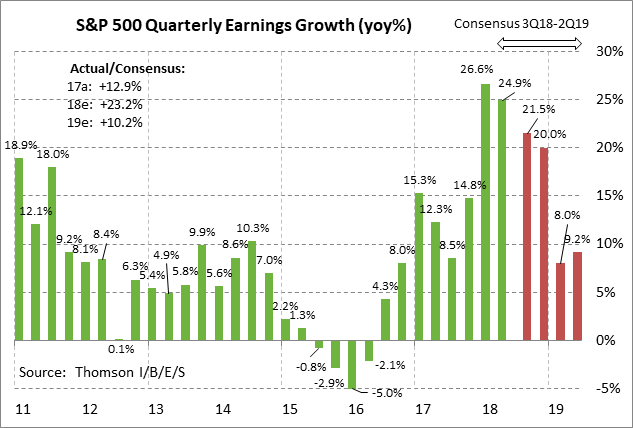

- Q3 earnings season begins with strong expectations

Weekly global market focus — The U.S. markets this week will focus on (1) last week’s surge in T-note yields and whether the market can absorb this week’s auction deluge without a further rise in yields, (2) the U.S. stock market, which now faces the challenge of the beginning of Q3 earnings season in addition to the surge in T-note yields and ongoing trade tensions, (3) the U.S. inflation situation with Wednesday’s Sep PPI report and Thursday’s Sep CPI report (expected mixed at +2.4% y/y and +2.3% core vs Aug’s +2.7% and +2.2%), (4) trade tensions as the markets remain nervous about whether President Trump may soon announce another round of tariffs on China, (5) Washington politics with only four weeks left until the Nov 6 mid-term elections, (6) oil prices, which are consolidating mildly below last week’s 4-year high as the market remains nervous about falling Iranian oil exports ahead of full U.S. sanctions on Iran on Nov 5, and (7) any developments from the Thursday-Friday G-20 meeting of finance ministers and central bankers in Bali, Indonesia.

Today is a partial U.S. holiday day for Columbus Day with the cash Treasury and forex markets closed but with the stock and futures markets open. The Japanese markets are closed today for a national holiday.

In Europe, the focus will remain on Italy as the government finalizes its budget to present to the European Commission by next Monday (Oct 15). The current proposal of a 2.4% budget deficit in 2019 is based on overly-optimistic GDP growth forecasts and is well above the level mandated by the Commission for countries such as Italy that have a national debt load far in excess of the official ceiling of 60% of GDP. The Italian 10-year bond yield last Friday of 3.42% was just 3 bp below last Tuesday’s 4-1/2 year high of 3.45%. The Italy-German 10-year yield spread last Tuesday posted a new 5-1/4 year high of 3.03% and closed the week up +17 bp at 285 bp.

The European markets will also continue to watch the Brexit drama as the UK and EU fumble around for a compromise and as Japanese Abe said over the weekend that the UK would be welcomed into the Trans-Pacific Partnership.

In Asia, the markets are nervously awaiting Monday’s reopening of the Chinese mainland markets, which were closed last week for the Golden Week holiday. The Hong Kong Hang Seng index last week fell by -4.38% during the Chinese mainland holiday, while the offshore yuan fell by -0.3%. Bearish factors for Chinese stocks last week included (1) the weak Chinese October manufacturing PMI reports released just ahead of the holiday on Sep 29 (national PMI -0.5 to 50.8 and Caixin PMI -0.6 to 50.0), (2) increased worries that President Trump may soon announce tariffs on the remaining $267 billion of Chinese goods, (3) last week’s surge in the U.S. 10-year T-note yield to a 7-1/3 year high, which put downward pressure on the yuan, and (4) increasing US/Chinese military tensions.

The Chinese stock market today will see some support from the Chinese central bank’s announcement on Sunday of a hefty one percentage point cut in the bank Required Reserve Requirement, which will free up a net 750 billion yuan ($109 bln) of bank lending. That was the fourth cut of the year as the PBOC seeks to stimulate the economy and offset trade tensions. The PBOC has avoided an interest rate cut since that would directly undercut the yuan and potentially encourage capital flight and fresh stock market weakness.

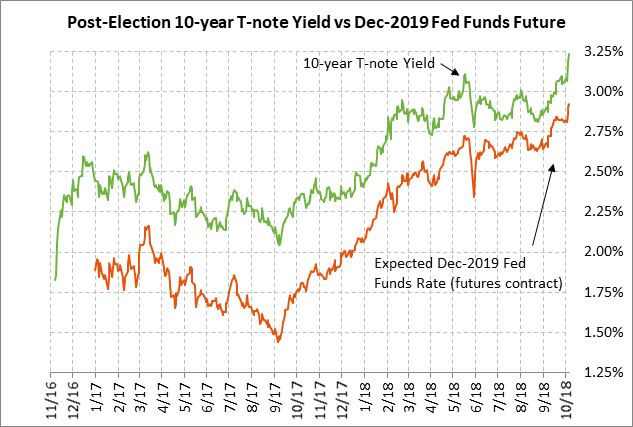

10-year T-note yield consolidates below last week’s 7-1/3 year high — The markets are waiting to see if T-note yields continue to climb even after last week’s +17 bp surge to a 7-1/3 year closing high of 3.23%. The Treasury market this week must absorb $230 billion worth of Treasury auctions. The Treasury will sell T-bills on Tuesday (due to Monday’s holiday), $36 billion of 3-year T-notes and $23 billion of reopened 10-year T-notes on Wednesday, and $15 billion of reopened 30-year bonds on Thursday.

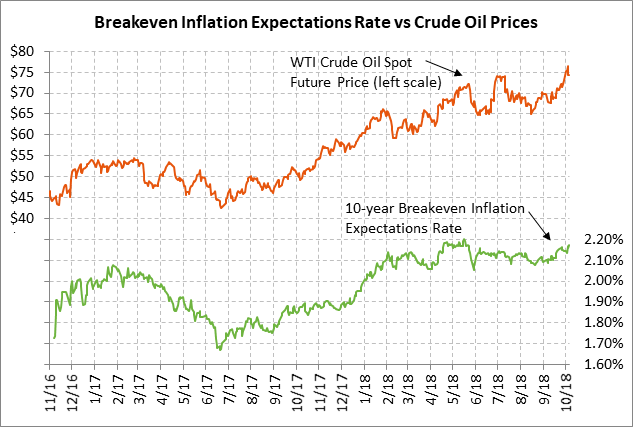

Factors causing last week’s surge in the 10-year yield include (1) last Wednesday’s strong Sep ADP report of +230,000 and last Friday’s drop in the Sep unemployment rate to a 49-year low of 3.7% (Friday’s weak payroll report of +134,000 was mostly written off due to Florence distortions), (2) stronger expectations for Fed rate hikes after Fed Chair Powell repeatedly expressed optimism about the economy and raised the possibility of raising rates to a level that would restrain the economy, (3) last Friday’s new 4-1/2 month high of 2.18% in inflation expectations, and (4) reduced safe-haven demand for T-notes after the recent NAFTA 2.0 agreement.

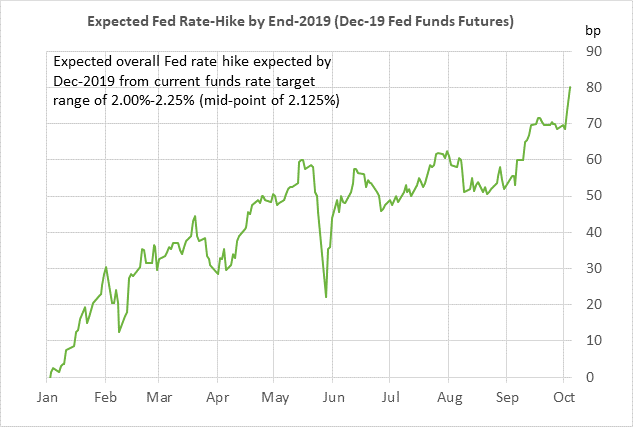

The market’s expectation for further rate hikes through the end of 2019 rose sharply by +11.5 bp last week to a new peak of 80 bp on Friday, which translates to nearly one-half of an additional rate hike. The market is now expecting another 3.2 rate hikes by the end of 2019, which is substantially more than the two rate hikes expected as recently as August. Expectations for more rate hikes have been driven by (1) strong U.S. economic data, (2) hawkish comments by Fed officials including Fed Chair Powell, and (3) rising inflation expectations. The 10-year breakeven inflation expectations rate last week rose by +2.7 bp to a new 4-1/2 month closing high of 2.17% due in part to last week’s new 4-year high in oil prices.

Q3 earnings season begins with strong expectations — Q3 earnings season begins with seven of the S&P 500 companies reporting this week and with notable reports including Citigroup and JP Morgan Chase on Friday. The consensus is for Q3 S&P 500 earnings growth of +21.5% y/y (+18.5% ex-energy), which would be down from +26.6% in Q1 and +24.9% in Q2, according to I/B/E/S. On a calendar year basis, earnings growth in 2018 is expected at +23.2% and at a weaker +10.2% in 2019.