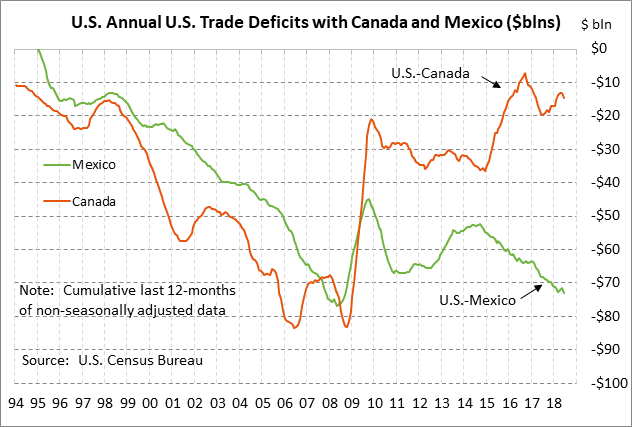

- Trade tensions ease after NAFTA agreement but China continues to pose major risks

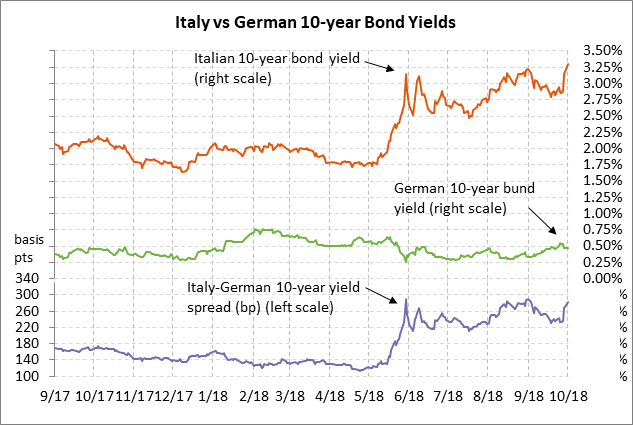

- Italian 10-year yield reaches new 4-1/2 year high as EU officials respond negatively to Italy’s budget

Trade tensions ease after NAFTA agreement but China continues to pose major risks — U.S. trade tensions eased substantially after Sunday night’s US/Canadian agreement on a NAFTA 2.0. U.S. trade tensions with the EU and Japan are also substantially lower at present since President Trump has agreed to a truce on any new tariffs as long as US/EU and US/Japan trade talks progress.

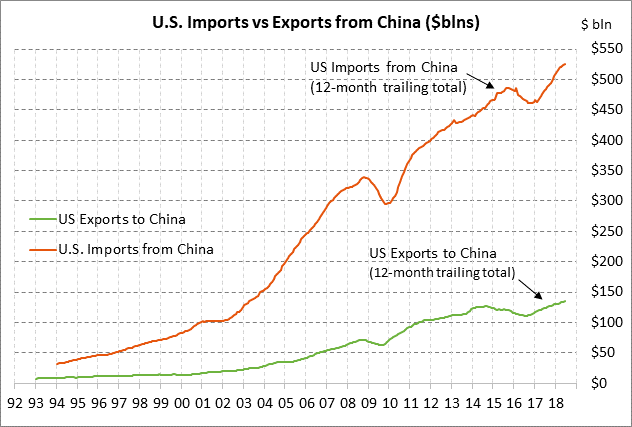

That leaves China as the main source of trade tensions, particularly since there is no prospect for any near-term resolution since the two sides are not even talking about trade. Moreover, the situation could quickly get worse since President Trump at any time could announce that his administration is going ahead with his threat to slap tariffs on another $267 billion of Chinese goods, which would leave penalty tariffs on virtually all U.S. imports from China. Chinese officials reportedly believe there is no point in talking about trade to the Trump administration until after the Nov 6 U.S. mid-term elections.

Other than US/Chinese trade tensions, the other two areas of trade strife include (1) the Trump administration’s ongoing consideration of a 25% tariff on all U.S. auto imports on national security grounds, and (2) President Trump’s threat to withdraw from the WTO if there aren’t major reforms. In addition, President Trump on Monday introduced India and Brazil as perhaps his two new targets for trade concessions. Mr. Trump said that “India charges us tremendous tariffs” and that Brazil’s trade tactics are “maybe the toughest in the world.”

Sunday night’s US/Canadian agreement on NAFTA 2.0 was very good news for the markets since a collapse of US/Canadian trade relations would have had very negative macroeconomic and supply chain effects. The NAFTA 2.0 agreement is expected to be signed by the respective leaders by Nov 30.

However, there are a number of sticking points on US/Mexican/Canadian trade relations could still cause problems for the markets. First, the NAFTA 2.0 deal (now rebranded as the US/Mexico/Canada agreement or USMCA), has to be approved by the U.S. Congress. Congressional passage of NAFTA 2.0 is far from certain, particularly if Democrats in the mid-term election take control of the House and/or Senate.

While Congress is considering the new NAFTA 2.0 deal, the old NAFTA rules will remain in place. There is concern that President Trump may still announce a NAFTA cancelation (with a 6-month notice) in order to step up pressure on Congress to approve the NAFTA 2.0 deal. If President Trump in fact canceled the old NAFTA, and Congress refused to pass the new NAFTA, then the U.S. after 6 months could be left with no NAFTA at all. Chaos would ensue with tariffs likely jumping to standard WTO levels.

Second, despite the NAFTA 2.0 agreement, the U.S. steel and aluminum tariffs on Mexico and Canada are staying in place for the time being, along with Mexican and Canadian retaliatory tariffs on U.S. products. There will be negotiations on the steel and aluminum tariffs over the next 60 days with the hope of some resolution before the NAFTA 2.0 agreement is due to be signed by Nov 30. President Trump on Monday hinted that the steel and aluminum tariffs could be resolved if Canada and Mexico would agree to quotas on the amount of steel and aluminum shipped to the U.S.

Third, the U.S. as part of the NAFTA 2.0 agreement reserved the right to slap auto tariffs on Canada and Mexico if the Commerce Department decides to implement such tariffs on national security grounds. However, the tariffs would only be imposed on imports above 2.6 million vehicles, which means that Mexico and Canada should effectively be shielded from any new U.S. auto tariffs.

Italian 10-year yield reaches new 4-1/2 year high as EU officials respond negatively to Italy’s budget — The Italian stock and bond markets on Monday continued last week’s sharp sell-off as reports emerged that the European Commission will reject Italy’s 2019 budget with its deficit of 2.4% of GDP.

European Commission President Juncker on Monday said, “After the toughest management of the Greek crisis, we have to do everything to avoid a new Greece — this time an Italy — crisis.” EU Commissioner Moscovici said that Italy’s plan for a 2.4% deficit is a “very, very significant” deviation from commitments. Meanwhile, Italian Finance Minister Tria reportedly indicated there may be some room to negotiate.

Italy must submit a formal budget to the European Commission in two weeks by October 15. The European Commission can demand changes in the budget to meet Italy’s fiscal commitments. The Eurozone’s official deficit ceiling is 3.0% of GDP but Italy is subject to much more stringent budget requirements since its national debt is massive at over 130% of GDP. Under the previous government, Italy would have had a 2019 budget deficit of only about 0.8% but the new government is proposing a deficit as high as 2.4% of GDP to satisfy campaign promises such as tax cuts and a minimum citizen income for the poor.

The iShares Italy ETF (EWI) on Monday fell by another -0.61%, adding to the -5.53% combined plunge seen last Thursday and Friday. Italy’s 10-year bond yield on Monday rose by another 15 bp to post a new 4-1/2 year high of 3.30%. The spread of the Italian 10-year bond yield over Germany rose by another +15 bp on Monday to a new 1-month high of 283 bp, which was only 8 bp below the late-Aug 5-1/4 year high of 291 bp.