- 10-year T-note yield tests 7-1/4 year high as Fed rate-hike expectations through 2019 are near the highest yet

- USTR Lighthizer gives up on Canadian NAFTA agreement by Sep 30 deadline, which could spark Trump retaliation

- Japan may agree to bilateral trade talks at Trump-Abe meeting today

10-year T-note yield tests 7-1/4 year high as Fed rate-hike expectations through 2019 are near the highest yet — The market is looking past the outcome of the 2-day FOMC meeting that ends today since there are unanimous market expectations for a +25 bp rate hike today to 2.00%/2.25%. The main question is whether the Fed today might signal a more hawkish tone with its post-meeting statement, Fed-dot projections, and/or Fed Chair Powell’s post-meeting press conference.

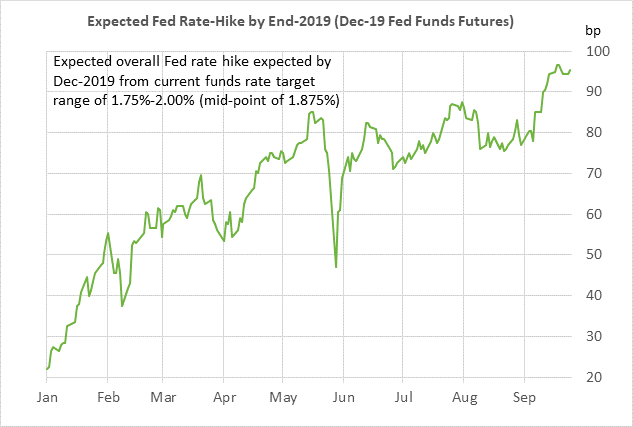

The market is now discounting a total of 95.5 bp of rate hikes through the end of 2019, or 70 bp of rate hikes following today’s +25 bp rate hike, according to the federal funds futures market. After today’s rate hike, the market is fully expecting another Fed rate hike at its last meeting of the year in December. The market is then expecting two rate hikes in 2019, with the funds rate thereafter moving sideways near 2.85%.

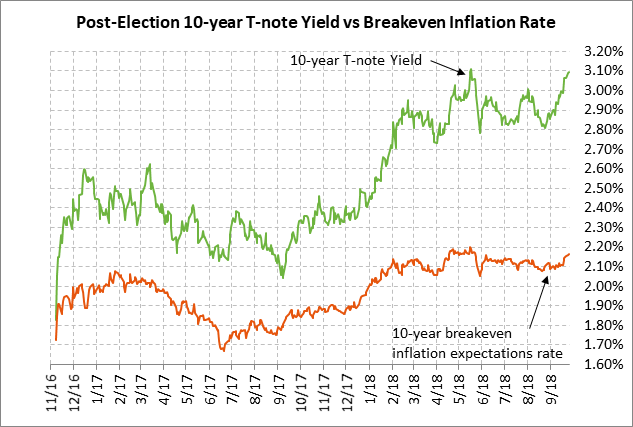

The market expectation for another 95.5 bp worth of rate hikes through 2019 is just 1 bp below last week’s record of 96.5 bp. Rate-hike expectations have risen sharply by about +15 bp just in the past three weeks due to the continued strength in the U.S. economy and due to rising inflation expectations with yesterday’s rally in Brent crude oil prices to a new 3-3/4 year high of $82.55. The 10-year breakeven inflation expectations rate on Tuesday rose to a 4-month high of 2.17% and are now only 4 bp below May’s 4-year high of 2.21%.

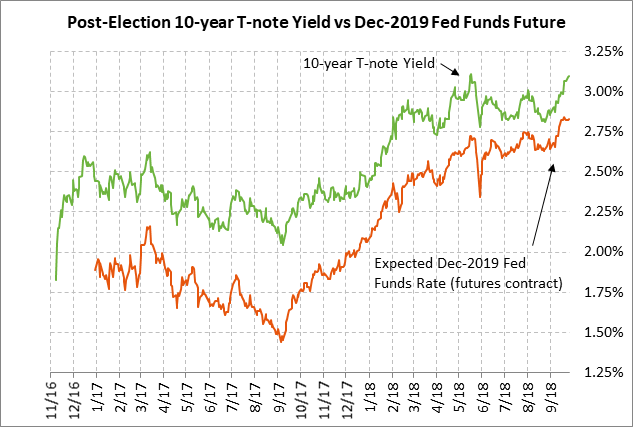

The rise in both rate-hike and inflation expectations has pushed the 10-year T-note yield higher. The 10-year T-note yield on Tuesday rose to a 4-month high of 3.111%, which was only 1.5 bp below May’s 7-1/4 year high of 3.126%. A breakout in the 10-year T-note yield to a new high seems to be only a matter of time given the Fed’s hawkish stance and the possibility of even higher oil prices as full U.S. sanctions on Iran near in November.

The only good news is that the Fed may have only three more rate hikes left after today’s hike. The federal funds futures market is discounting a funds rate of 2.82% by the end of 2019, which would be very close to the Fed’s estimate of a long-term neutral rate of 2.9%. However, the Fed-dots indicate that the Fed expects to push the funds rate 50 bp above the neutral rate, for an overall rate hike of about 150 bp from the current level.

The Fed seems to believe that the U.S. economy will continue to run hot over the next two years due in part to fiscal stimulus, thus requiring an above-neutral funds rate. The Fed doesn’t appear to be worried about the negative effects on the economy that could pile up next year from the Fed’s steady rate-hike regime, trade tensions, and a potential spike in oil prices from the loss of Iranian oil.

USTR Lighthizer gives up on Canadian NAFTA agreement by Sep 30 deadline, which could spark Trump retaliation — U.S. Trade Representative Lighthizer yesterday said that there are still “very large issues” between the U.S. and Canada on NAFTA, suggesting that there is virtually no chance of an agreement before Sunday’s (Sep 30) deadline. The Trump administration by Sunday must submit to Congress the final language of whatever NAFTA agreement it has. Mr. Lighthizer said “We’re going to go ahead with Mexico. If Canada comes along now, that would be the best. If Canada comes along later, then that’s what will happen.”

Mr. Lighthizer’s comment suggested that the U.S. and Canada will keep talking about a NAFTA agreement even as the U.S. and Mexico move ahead with signing a US/Mexico trade agreement by Dec 1. Instead of more talks, however, President Trump may force the issue by delivering the 6-month notice that the U.S. will withdraw from NAFTA and/or announcing that the U.S. is imposing the 25% tariff on Canadian vehicles that he has been threatening.

The most likely outcome seems to be that the whole NAFTA process will be dragged out into 2019. There seems to be a low chance that Congress will approve the US/Mexico trade agreement without the participation of Canada. That doesn’t even take into account whether the Trump administration will even be allowed to substitute the US/Mexican trade agreement for NAFTA and still qualify for the fast-track rules. If Congress refuses to approve the Mexican deal, then the U.S. would have to restart negotiations with Mexico because President-elect Obrador (who takes power on Dec 1) may have his own ideas about what he wants to see in the US/Mexican agreement. That would give more time to bring Canada back on board with a trilateral NAFTA agreement.

The bottom line is that Canada’s refusal to agree to NAFTA terms by Sep 30 raises the risks for retaliation by President Trump and also raises the odds that NAFTA negotiations will now bleed into 2019.

Japan may agree to bilateral trade talks at Trump-Abe meeting today — Japan may agree to bilateral trade talks with the U.S. if the U.S. agrees not to impose auto tariffs on Japan, according to a Tuesday Bloomberg report citing sources close to the Japanese government. That agreement could come today during a scheduled meeting between President Trump and Prime Minister Abe on the sidelines of the UN meetings in New York.

The markets would be pleased with such an agreement since that would at least remove the immediate Trump threat to slap a 25% duty on Japanese autos. Up until now, Japan has resisted the U.S. demand for bilateral negotiations and has insisted that the U.S. needs to return to the terms of the TransPacific Partnership.