- Weekly market focus

- Turkish crisis continues as Erdogan remains defiant in weekend comments

- Q2 earnings season winds down

Weekly market focus — The U.S. markets this week will focus on (1) any new spillover from last week’s plunges in the Turkish and Russian markets due to U.S. sanctions, (2) any developments on trade tensions as the Trump administration considers tariffs on $200 billion of China goods in September and a 25% tariff on imported vehicles, (3) Washington politics as the Manafort trial continues this week, (4) the wind-down of Q2 earnings season with 64 of the S&P 500 companies scheduled to report, and (5) a moderately busy U.S. economic schedule with the most notable report being Wednesday’s July retail sales report (expected +0.1% and +0.4% ex-autos after June’s +0.5% and +0.4% ex-autos).

In Europe, the markets will mainly focus on the crisis in Turkey after there were spill-over effects last Friday due to a sell-off in European banks with Turkish exposure. The Turkish lira in early Asian trading on Sunday night fell by another -6% against the dollar, adding to last Friday’s -16% plunge. The European markets will also be watching the Russian ruble, which plunged by -7% last week and posted a new 2-1/4 year low against the dollar on new U.S. sanctions.

Elsewhere in Europe, the UK and EU are scheduled to hold two days of Brexit talks in Brussels on Thursday/Friday as Prime Minister May continues to push for European acceptance of her Chequers Brexit plan, which seems unlikely. UK trade secretary Liam Fox last week said that EU “intransigence” makes it “60-40 percent” likely that the UK will crash out of the EU without an agreement in March 2019.

In Asia, the markets this week will continue to focus on China where the Chinese markets on Friday suffered some spillover from Turkey and Russia and continued to be negatively impacted by US/Chinese trade tensions. The Chinese yuan closed -0.3% lower last week and consolidated just mildly above the recent 1-1/4 year low. Meanwhile, the Shanghai Composite index last week closed +2.00% on hopes for government stimulus to offset trade tensions. Tonight’s Chinese July industrial production and retail sales reports are expected to show a slight improvement from June’s reports although the risks remain mostly on the downside for China’s economic data.

In Japan, the markets will continue to assess where the BOJ wants the 10-year JGB yield to trade after its recent hike of the upper target limit to 0.20%. After trading as high as 0.14% in early August, the 10-year JGB yield eased and closed -1 bp at 0.101% last week, which is right at the BOJ’s old upper target limit.

Turkish crisis continues as Erdogan remains defiant in weekend comments — Turkish President Erdogan in weekend comments remained defiant and gave no sign that he is about to meet U.S. demands for the release of American pastor Andrew Brunson or that he is willing to raise interest rates to stem the currency crisis. The Turkish lira last week plunged by -26.6% against the dollar to a new record low.

The Turkish crisis worsened after the Trump administration recently slapped sanctions on top Turkish cabinet officials as punishment for not releasing American pastor Brunson. President Trump last Friday then poured gasoline on the fire by doubling tariffs on Turkish steel and aluminum exports to the U.S. More U.S. sanctions may well be forthcoming this week if Mr. Erdogan continues to refuse to release the American pastor.

There were spillover effects for Europe from the Turkish crisis last Friday after FT reported that the ECB is investigating the exposure of European banks to Turkish loans. Banks with particular Turkish exposure reportedly include BBVA, UniCredit, and BNP Paribas. EUR/USD fell sharply by -0.99% last Friday and posted a new 13-month low. The Euro Stoxx 50 index last Friday fell sharply by -1.94% to a new 5-week low.

Q2 earnings season winds down — Q2 earnings season is winding down with only 64 of the S&P 500 companies scheduled to report this week. Notable reports this week include Sysco on Monday; Home Depot and Agilent Technologies on Tuesday; Macy’s and Cisco on Wednesday; Walmart, Nvidia and Nordstrom on Thursday; and Deere on Friday.

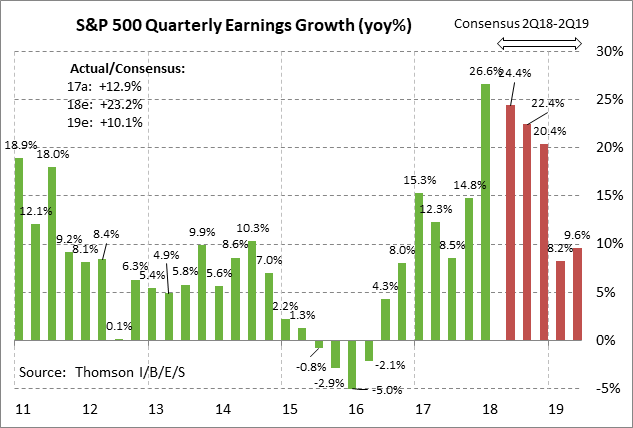

The market consensus is for very strong SPX Q2 earnings growth of +24.4% y/y, according to Thomson I/B/E/S, which would be down from Q1’s +26.6% but would still be a very strong figure. Q2 SPX revenue is expected to show a strong increase of +9.3% y/y. Q2 earnings have been stronger than market expectations. Of the 454 SPX companies that have reported, 78.9% have beaten the consensus, which is above the long-term average of 64% and the 4-quarter average of 75%, according to Thomson I/B/E/S. Of reporting companies, 71.3% have beaten revenue expectations, which is well above the long-term average of 60% but slightly below the 4-quarter average of 72%.

Looking ahead, earnings growth is expected to remain above 20% in the second half of this year at +22.4% in Q3 and +20.4% in Q4, according to Thomson I/B/E/S. On a calendar year basis, the consensus is for very strong SPX earnings growth this year of +23.2%. Earnings growth is then expected to decelerate to +10.1% in 2019 as the effects from the Jan 1 tax cut start to wear off.

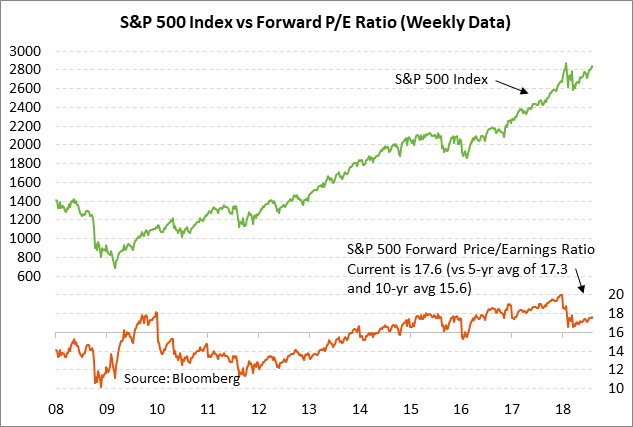

Valuation levels have become more reasonable due to the strength in earnings and the downward correction in stock prices. Still, the current forward P/E for the S&P 500 index of 17.6 is mildly above the 5-year average of 17.3 and is moderately above the 10-year average of 15.6.