- Congress appears headed for tax bill passage by Wednesday

- CR remains in flux but shutdown seems unlikely

- U.S. housing starts expected to fall back after Oct’s surge

- U.S. current account balance expected to narrow mildly

Congress appears headed for tax bill passage by Wednesday — The House today is expected to vote to approve the compromise tax reform bill released last Friday, then forward the bill over to the Senate. The Senate is expected to vote on the bill either late today or on Wednesday. As long as there are no changes to the bill in the Senate that become necessary to meet reconciliation rules, for example, then Senate passage of the bill will mean that Congress is done with the bill and it will be forwarded to President Trump for his certain signature. That would allow the tax bill to go into effect in less than two weeks on January 1, 2018.

Senate Majority Leader McConnell appears to have enough votes to approve the bill in the Senate. Senator Jeff Flake is the only Republican Senator that remains undecided on the bill, according to Bloomberg News. Other Senators who were undecided, or who were previously opposed, have now said they will vote in the favor of the bill, including Senators Corker, Rubio, Lee, and Collins.

Senator John McCain this past weekend went back to Arizona for health reasons and is not planning on being present in the Senate for this week’s tax vote. That means that even if Senator Flake comes out against the bill, the bill can still pass even with John McCain’s absence as long as Vice President Pence is present to cast the deciding vote.

VP Pence has postponed this week’s trip to the Middle East until the week of Jan 14, according to Washington Post, which means that Mr. Pence will be available all this week for any Senate votes that are needed. Moreover, President Trump said on Sunday that Mr. McCain could come back to Washington vote on the tax bill if it becomes necessary. As a result, it appears that Mr. McConnell already has a tax-bill victory in hand.

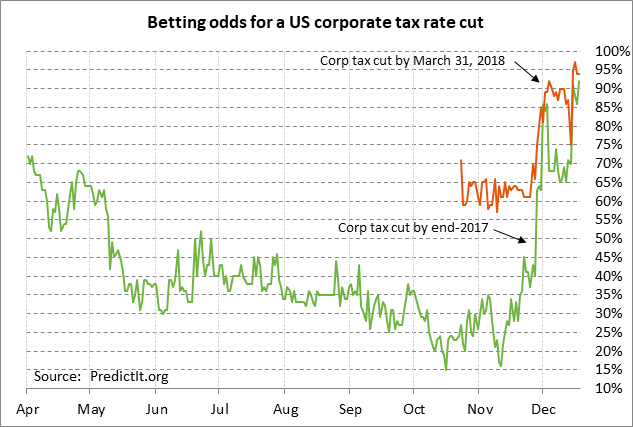

The betting odds for a corporate tax cut by year-end are currently at 92% and at 94% for that tax cut by March 31, 2018, according to PredictIt.org.

CR remains in flux but shutdown seems unlikely — Republican leaders have not had much time to focus on a new continuing resolution (CR) since they want to first get the tax reform bill approved in both the House and Senate. After that, they must quickly get a new CR approved to prevent a government shutdown this Friday night at midnight.

There has been no meeting of the minds as yet between Republicans and Democrats on topline spending numbers for the remainder of the fiscal year or whether the spending bill will cover children’s health insurance, dreamers, disaster relief, a bipartisan Obamacare fix, or other issues. House Republicans today or Wednesday plan to approve a CR lasting through Jan 19, but that proposed CR will be dead on arrival among Senate Democrats because it will contain defense spending authorization for the remainder of the fiscal year with no assurance that non-defense spending will be increased to match the defense spending hike.

Due to the wide differences between Republicans and Democrats, a full agreement on a new CR will be very difficult on such short notice. If that is the case, then Congressional leaders may approve just a simple roll-over of the current CR into January and deal with the difficult issues then.

It is hard to imagine Congress letting the government shut down on Friday night and then leaving Washington for the Christmas holiday weekend while U.S. government employees are temporarily out of a job. Plus that would mean that Congress would have to return to Washington next week after the Christmas weekend to deal with a new CR, which also seems unlikely. A Congressional punt into January seems to be the likely bet at this point.

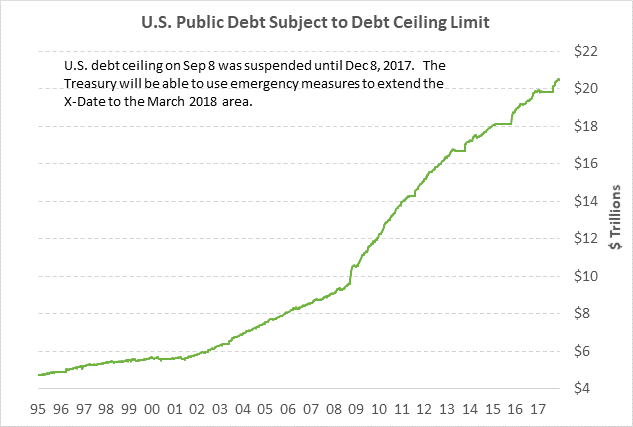

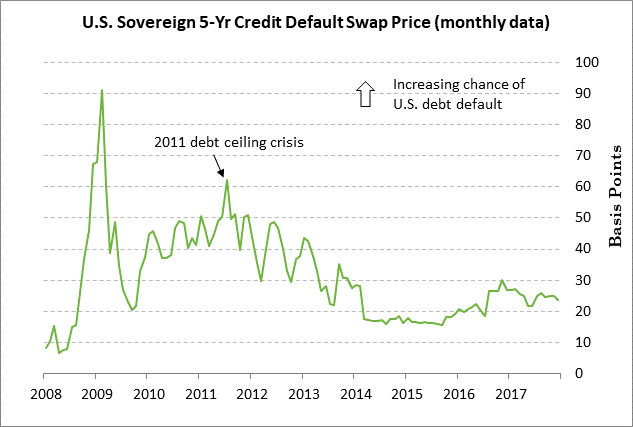

The markets remain relatively unconcerned at this point about the possibility of a U.S. government shut-down. A brief government shutdown would have little impact on the economy and would not threaten the full faith and credit of the U.S. government. The debt ceiling, by contrast, does threaten the full faith and credit of the U.S. government due to the possibility of Treasury default. However, the Treasury does not need a debt ceiling hike until around March 2018. The 5-year credit default swap price (the price of insuring against a Treasury default) is currently moving sideways in a subdued fashion and is not indicating any concern about a Treasury default.

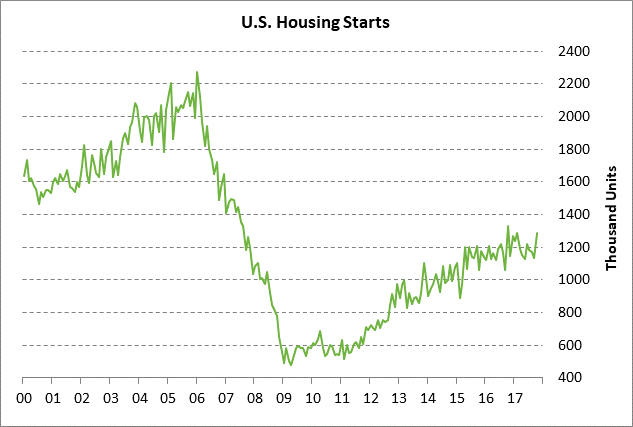

U.S. housing starts expected to fall back after Oct’s surge — The market consensus is for today’s Nov housing starts report to fall back by -3.2% to 1.249 million after October’s +13.7% surge to 1.29 million. Housing starts surged in October due to home rebuilding in the wake of the Aug/Sep hurricanes. The Oct housing starts level of 1.290 million was only -2.9% below the 10-year high of 1.328 million units posted in Oct 2016. The increased home building that will be taking place as a result of hurricane damage will give GDP a boost in Q4. The Atlanta Fed’s GDPNow forecast for Q4 GDP growth is currently at +3.3%, even stronger than the growth rates seen in the last two quarters of +3.1% in Q2 and +3.0% in Q3.

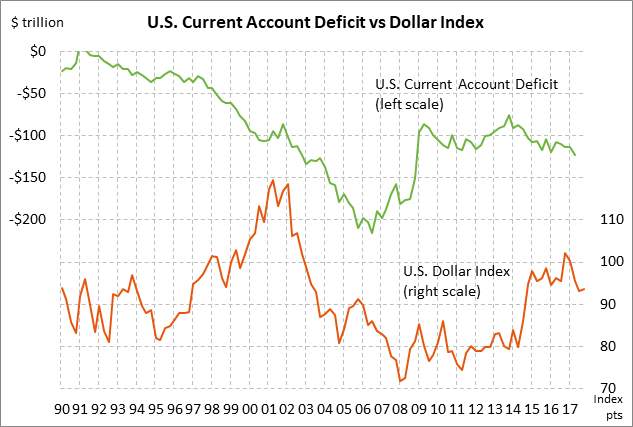

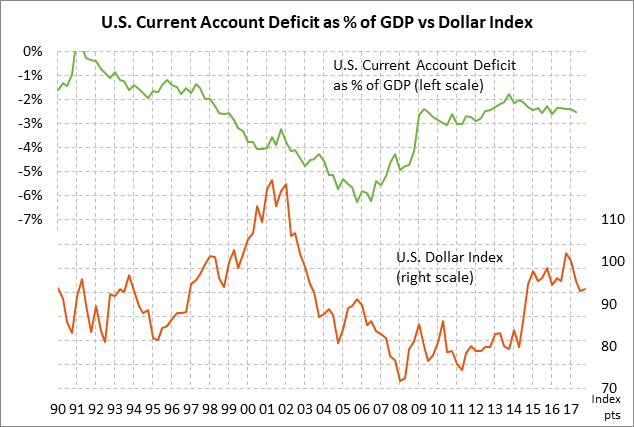

U.S. current account balance expected to narrow mildly — The market consensus is for today’s Q3 current account deficit to narrow moderately to -$116.0 billion from -$123.1 billion in Q2, which was the widest deficit in 8-1/2 years. Today’s expected deficit of -$116.0 billion would be just mildly wider than the 8-quarter trend average of -$113.6 billion. The wide U.S. current account deficit continues to be a mildly bearish long-term factor for the dollar since about $1.4 billion worth of dollars are flowing out of the U.S. every calendar day. However, that is miniscule compared to the daily volume of FX trading.

Congress appears headed for tax bill passage by Wednesday — The House today is expected to vote to approve the compromise tax reform bill released last Friday, then forward the bill over to the Senate. The Senate is expected to vote on the bill either late today or on Wednesday. As long as there are no changes to the bill in the Senate that become necessary to meet reconciliation rules, for example, then Senate passage of the bill will mean that Congress is done with the bill and it will be forwarded to President Trump for his certain signature. That would allow the tax bill to go into effect in less than two weeks on January 1, 2018.

Senate Majority Leader McConnell appears to have enough votes to approve the bill in the Senate. Senator Jeff Flake is the only Republican Senator that remains undecided on the bill, according to Bloomberg News. Other Senators who were undecided, or who were previously opposed, have now said they will vote in the favor of the bill, including Senators Corker, Rubio, Lee, and Collins.

Senator John McCain this past weekend went back to Arizona for health reasons and is not planning on being present in the Senate for this week’s tax vote. That means that even if Senator Flake comes out against the bill, the bill can still pass even with John McCain’s absence as long as Vice President Pence is present to cast the deciding vote.

VP Pence has postponed this week’s trip to the Middle East until the week of Jan 14, according to Washington Post, which means that Mr. Pence will be available all this week for any Senate votes that are needed. Moreover, President Trump said on Sunday that Mr. McCain could come back to Washington vote on the tax bill if it becomes necessary. As a result, it appears that Mr. McConnell already has a tax-bill victory in hand.

The betting odds for a corporate tax cut by year-end are currently at 92% and at 94% for that tax cut by March 31, 2018, according to PredictIt.org.

CR remains in flux but shutdown seems unlikely — Republican leaders have not had much time to focus on a new continuing resolution (CR) since they want to first get the tax reform bill approved in both the House and Senate. After that, they must quickly get a new CR approved to prevent a government shutdown this Friday night at midnight.

There has been no meeting of the minds as yet between Republicans and Democrats on topline spending numbers for the remainder of the fiscal year or whether the spending bill will cover children’s health insurance, dreamers, disaster relief, a bipartisan Obamacare fix, or other issues. House Republicans today or Wednesday plan to approve a CR lasting through Jan 19, but that proposed CR will be dead on arrival among Senate Democrats because it will contain defense spending authorization for the remainder of the fiscal year with no assurance that non-defense spending will be increased to match the defense spending hike.

Due to the wide differences between Republicans and Democrats, a full agreement on a new CR will be very difficult on such short notice. If that is the case, then Congressional leaders may approve just a simple roll-over of the current CR into January and deal with the difficult issues then.

It is hard to imagine Congress letting the government shut down on Friday night and then leaving Washington for the Christmas holiday weekend while U.S. government employees are temporarily out of a job. Plus that would mean that Congress would have to return to Washington next week after the Christmas weekend to deal with a new CR, which also seems unlikely. A Congressional punt into January seems to be the likely bet at this point.

The markets remain relatively unconcerned at this point about the possibility of a U.S. government shut-down. A brief government shutdown would have little impact on the economy and would not threaten the full faith and credit of the U.S. government. The debt ceiling, by contrast, does threaten the full faith and credit of the U.S. government due to the possibility of Treasury default. However, the Treasury does not need a debt ceiling hike until around March 2018. The 5-year credit default swap price (the price of insuring against a Treasury default) is currently moving sideways in a subdued fashion and is not indicating any concern about a Treasury default.

U.S. housing starts expected to fall back after Oct’s surge — The market consensus is for today’s Nov housing starts report to fall back by -3.2% to 1.249 million after October’s +13.7% surge to 1.29 million. Housing starts surged in October due to home rebuilding in the wake of the Aug/Sep hurricanes. The Oct housing starts level of 1.290 million was only -2.9% below the 10-year high of 1.328 million units posted in Oct 2016. The increased home building that will be taking place as a result of hurricane damage will give GDP a boost in Q4. The Atlanta Fed’s GDPNow forecast for Q4 GDP growth is currently at +3.3%, even stronger than the growth rates seen in the last two quarters of +3.1% in Q2 and +3.0% in Q3.

U.S. current account balance expected to narrow mildly — The market consensus is for today’s Q3 current account deficit to narrow moderately to -$116.0 billion from -$123.1 billion in Q2, which was the widest deficit in 8-1/2 years. Today’s expected deficit of -$116.0 billion would be just mildly wider than the 8-quarter trend average of -$113.6 billion. The wide U.S. current account deficit continues to be a mildly bearish long-term factor for the dollar since about $1.4 billion worth of dollars are flowing out of the U.S. every calendar day. However, that is miniscule compared to the daily volume of FX trading.