- Fed Chair Powell today delivers second day of testimony after first day garners mildly bullish market reaction

- U.S. manufacturing production expected to show only a modest increase

- U.S. unemployment claims expected to show a continued improvement in U.S. labor market

Fed Chair Powell today delivers second day of testimony after first day garners mildly bullish market reaction — Fed Chair Powell today will appear before the Senate Banking Committee for his second day of testimony on the Fed’s semi-annual monetary policy report to Congress.

The markets reacted dovishly to Mr. Powell’s first day of testimony on Wednesday to the House Financial Services Committee. Mr. Powell suggested that QE tapering is still “a ways off” and he continued to insist that the current inflation surge is transitory.

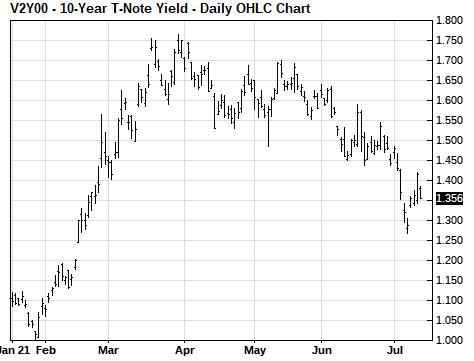

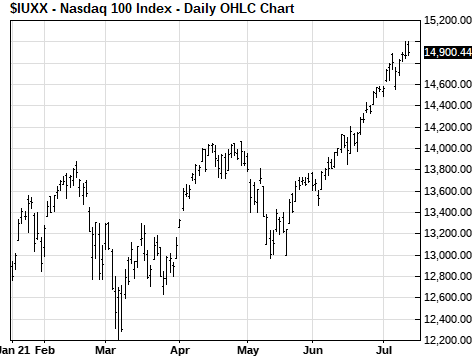

The S&P 500 index on Wednesday posted a new record high and closed mildly higher by +0.12%. The 10-year T-note yield fell -6 bp to 1.36%.

Regarding QE tapering, Mr. Powell said, “At our June meeting, the committee discussed the economy’s progress toward our goals since we adopted our asset purchase guidance last December. While reaching the standard of ‘substantial further progress’ is still a ways off, participants expect that progress will continue.”

In response to questions about the timing of QE tapering, Mr. Powell said, “It’s very difficult to be precise about it. We will provide lots of notice as we go forward on that.”

A survey taken by Bloomberg in June showed a consensus that the Fed’s early warning of QE tapering will come at either the August Jackson Hole conference or the following FOMC meeting on September 21-22. That survey showed that 33% of the respondents then expect the formal announcement of QE tapering in September, 10% in October or November, and 33% in December.

Mr. Powell said that the labor market recovery has “a long way to go.” He said, “Conditions in the labor market have continued to improve, but there is still a long way to go. Job gains should be strong in coming months as public health conditions continue to improve and as some of the other pandemic-related factors currently weighing them down diminish.”

Mr. Powell on Wednesday continued to push the Fed’s view that the current inflation surge is transitory. Mr. Powell said that the recent inflation statistics had been “higher than expected and hoped for,” but he noted that the largest inflation gains have come from a small group of goods and services tied to the reopening of the economy.

Mr. Powell said the overall inflation outlook remains consistent with the Fed’s long-term goals. He said, “Measures of longer-term inflation expectations have moved up from their pandemic lows and are in a range that is broadly consistent with the FOMC’s longer-run inflation goal.”

In a nod to the bond market, however, Mr. Powell again promised to take action if inflation were to get out of control. He said that if high inflation persisted and threatened to uproot inflation expectations, “we would absolutely change our policy as appropriate.” That comment was at least partially behind yesterday’s -6 bp decline in the 10-year T-note yield.

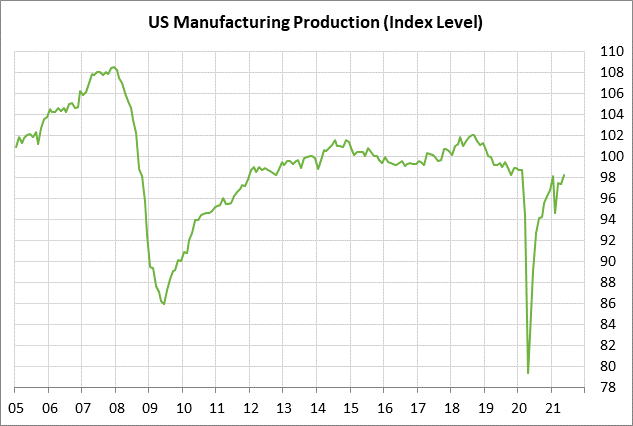

U.S. manufacturing production expected to show only a modest increase — The consensus is for today’s June manufacturing production report to show a modest increase of +0.3% m/m, weakening after May’s strong increase of +0.9% m/m. Today’s broader June industrial production report is expected to show a larger increase of +0.6% m/m, adding to May’s increase of +0.8% m/m.

U.S. manufacturing production has yet to see any major increase this year despite the economic recovery. Manufacturing production in May was up +18.3% from the year-earlier level, but that isn’t surprising due to the low year-earlier base from the pandemic shutdowns seen in May 2020. In fact, the May manufacturing production index of 98.2 in May was barely above the 98.1 level seen earlier this year in January.

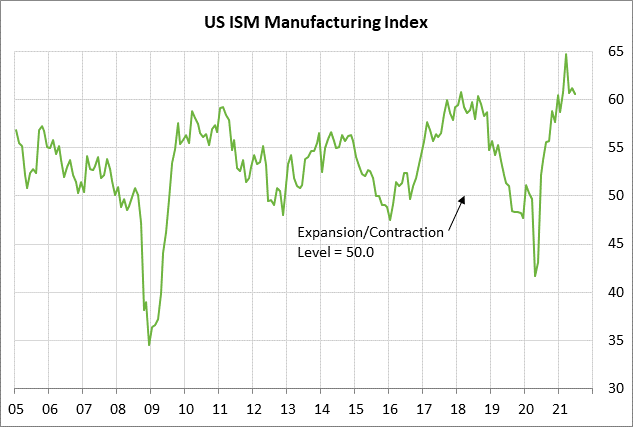

Confidence in the manufacturing sector was strong in May, with the ISM manufacturing index at 60.6. However, that was down from the 37-year high of 64.7 seen in March when there was near euphoria as the Covid infection levels plunged.

While the manufacturing sector is seeing strong order flow, production levels have been hampered by the chip shortage, various supply chain bottlenecks, and reports of labor shortages. The production situation should improve in coming months as companies overcome their various obstacles and respond to the strong order flow.

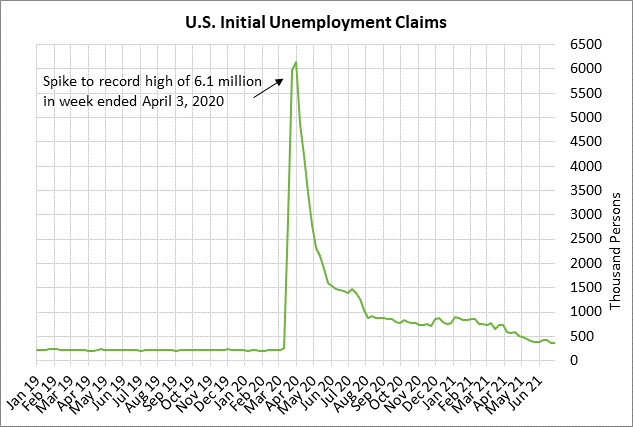

U.S. unemployment claims expected to show a continued improvement in U.S. labor market — Today’s unemployment claims report is expected to show a continued improvement in the U.S. labor market, with a decline in both initial and continuing claims to new 16-month lows.

The consensus is for today’s initial unemployment claims report to show a decline of -23,000 to 350,000, more than reversing last week’s small +2,000 increase to 373,000. Continuing claims are expected to show a -39,000 decline to 3.300 million, adding to last week’s -130,000 decline to 3.339 million.

Initial claims are now only 157,000 above the pre-pandemic level seen in February 2020. However, continuing claims are still 1.776 million above the pre-pandemic level, meaning there are still about 1.8 million more people on the unemployment rolls now than there were before the pandemic.