- FOMC believes policy-hold will last through 2020

- Trump trade team reportedly meets today on China tariff

- Christine Lagarde takes the stage

- UK election tightens but betting odds remain very strong for Conservative victory

- U.S. core PPI expected slightly higher

- 30-year bond auction to yield near 2.23%

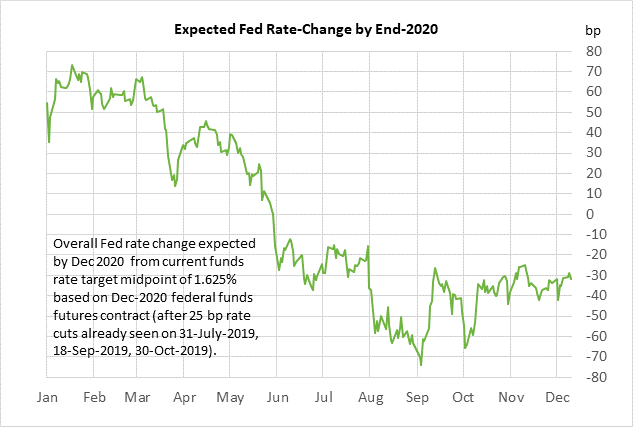

FOMC believes policy-hold will last through 2020 — The market responded to the Tue/Wed FOMC meeting with a slightly dovish tone with a small 3-4 bp dovish turn in the 2021 federal funds futures contracts and about a -2 bp drop in T-note yields. The T-note yield slipped a bit based in part on Fed Chair Powell’s comment that the Fed would be willing to extend its T-bill buying program to short-term Treasury coupons if that becomes necessary to soothe the tight short-term funding markets.

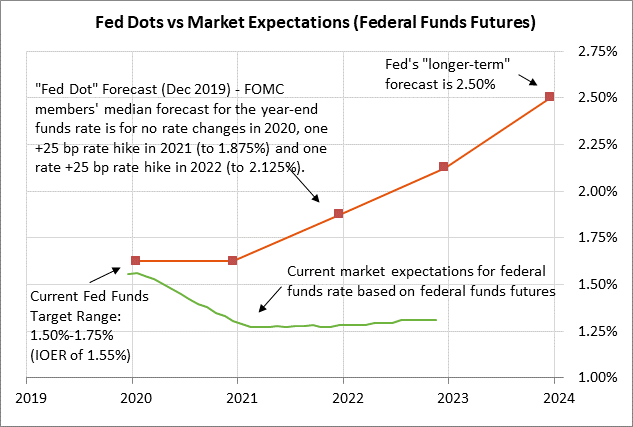

The markets were also relieved that the Fed’s dot-plot was neutral for 2020 and that the bulk of FOMC members didn’t foresee any rate hikes until 2021. Thirteen of the FOMC members forecasted an unchanged funds rate during 2020, while only four members forecasted a +25 bp rate hike. The median forecast is then for a +25 bp rate hike in 2021 and a second hike in 2022, matching the rate-hike pattern in the last set of Fed-dots from September.

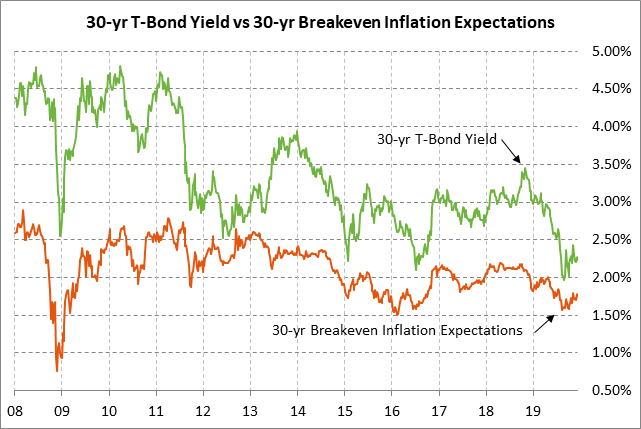

The markets were also pleased that Fed Chair Powell restated his comment from the October FOMC meeting suggesting that he has a high bar for a rate hike. Mr. Powell said, “In order to move rates up, I would want to see inflation that’s persistent and that’s significant. That’s my view.” The market sees little risk of any major increase in inflation over the near-term considering that the 10-year breakeven inflation expectations rate is currently at only 1.71%, well below the Fed’s +2.0% inflation target.

The FOMC in its post-meeting statement dropped its reference to “uncertainties” about the outlook since the Fed apparently wanted to indicate that it is now more confident about the U.S. economic outlook. Mr. Powell added, “Both the economy and monetary policy right now are in a good place.” However, the reality is that the economic outlook is actually quite uncertain since the markets don’t know whether President Trump will go ahead with Sunday’s tariff or whether there will be a phase-one trade deal.

Trump trade team reportedly meets today on China tariff — Bloomberg on Tuesday reported that President Trump and his trade advisors are scheduled to meet today ahead of Mr. Trump’s decision about whether to proceed with Sunday’s 15% tariff on the last $160 billion of Chinese goods.

Bloomberg reported on Tuesday that Chinese officials are optimistic that Mr. Trump will delay Sunday’s tariff as negotiations continue. However, White House advisors Kudlow and Navarro responded to that report by saying that as of Tuesday the tariff was still on the table.

The markets seem to be confident that Mr. Trump will delay Sunday’s tariff based on the stock markets’ buoyant tone. President Trump seems to be generally pleased with how the talks are going and he seems to want a deal ahead of next year’s campaign season. Also, Sunday’s tariff would be on a variety of U.S. consumer items that are likely to see price hikes if Mr. Trump goes through the tariff, which risks alienating U.S. consumers and voters.

However, the fact that the market seems confident about a tariff delay on Sunday also means the markets are vulnerable to a big downside surprise if Mr. Trump should unexpectedly proceed with the tariff.

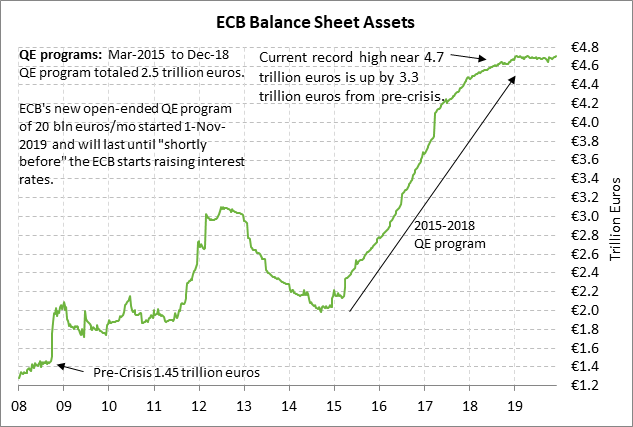

Christine Lagarde takes the stage — The ECB at its meeting today is unanimously expected to leave its interest rates and its QE program unchanged. The markets are mainly waiting to see how Ms. Lagarde handles her first press conference as ECB President and whether she indicates any shift in the ECB’s policy tone or emphasis. The ECB today is expected to launch an overall review of its long-term strategy. That multi-month review could come back with some criticism about the efficacy of negative interest rates and the ECB’s QE program.

The ECB at its Sep 12 meeting announced a -10 bp cut in the deposit rate to -0.50% and a new QE program starting November 1 involving the purchase of 20 billion euros per month of securities. Former ECB President Draghi at his last meeting on October 24 then left policy unchanged.

UK election tightens but betting odds remain very strong for Conservative victory — The polls in the past week have shifted a bit towards Labour but the Conservatives are still well ahead and polls suggest an easy Conservative victory with a majority of seats. Market reaction to the election will be on a sliding scale according to the size of the Conservative’s majority, since a larger majority would mean that Prime Minister Johnson will have an easier time coaxing his party into approving his Brexit withdrawal bill by the January 31 Brexit deadline.

Mr. Johnson claims that all the Conservative Party members standing for election support his Brexit withdrawal plan, although that seems unlikely. Sterling would plunge in the event that there is an unexpected hung Parliament, where Conservatives again do not have a majority and have difficulty passing a Brexit bill.

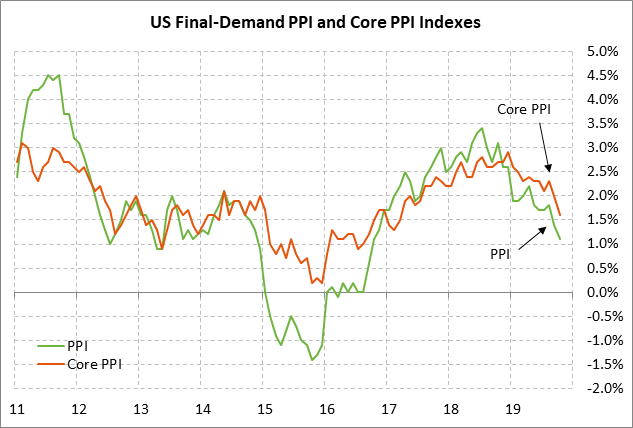

U.S. core PPI expected slightly higher — The consensus is for today’s Nov final-demand PPI to rise slightly to +1.2% y/y from Oct’s +1.1% and for the core PPI CPI to edge higher to +1.7% y/y from Oct’s +1.6%. Yesterday’s Nov CPI rose to +2.1% from Oct’s +1.8% and was slightly stronger than expectations of +2.0%, but the core CPI was in line with expectations at unchanged from Oct’s +2.3%.

30-year bond auction to yield near 2.23% — The Treasury today will sell $16 billion of reopened 30-year bonds, concluding this week’s $78 billion auction package. The 30-year bond late yesterday was trading at 2.23%, near the middle of the range seen in the past several months.