- Friday’s self-imposed deadline for a pandemic bill approaches

- Treasury bets the market can handle its deluge of longer-term debt

- U.S. unemployment claims expected to show some improvementÂ

Friday’s self-imposed deadline for a pandemic bill approaches — Friday’s self-imposed deadline for a deal on a pandemic bill is rapidly approaching for both Republican and Democratic negotiators.

White House Chief of Staff Meadows said yesterday, “I think at this point we’re either going to get serious about negotiating and get an agreement in principle or I’ve become extremely doubtful that we’ll be able to make a deal if it goes well beyond Friday.” If there is no deal soon, President Trump is threatening to proceed with executive action on extending the unemployment bonus and the eviction shield, and also on suspending the payroll tax.

Meanwhile, the number two Senate Republican leader, John Thune, said on Wednesday that if no deal is reached by Friday, Senators will likely leave for their August recess as scheduled and then be called back if necessary for a vote. The House is already on recess and will be called back if there is a bill to approve.

After another Mnuchin-Meadows-Pelosi-Schumer meeting Wednesday afternoon, Speaker Pelosi said, “I feel optimistic that there is light at the end of the tunnel. But how long the tunnel is remains to be seen.”

Bloomberg reported that Republicans have offered to extend the unemployment bonus at $400 per week but that Democrats are still insisting on $600. Republicans have reportedly agreed to extend the eviction moratorium until the end of the year. Democrats have lowered their demand for Post Office money to $10 billion from $25 billion over three years. Republicans are offering $200 billion in education and state-local aid, which is substantially less than Democrats are demanding. Ms. Pelosi said yesterday, “We still have a distance apart in terms of state and local.”

The markets seem optimistic that a deal will be finalized by this weekend or early next week, possibly allowing a vote next week. Up to 30 million Americans are in the process of missing their second week of unemployment bonus payments, which is putting a substantial dent in consumer income and spending.

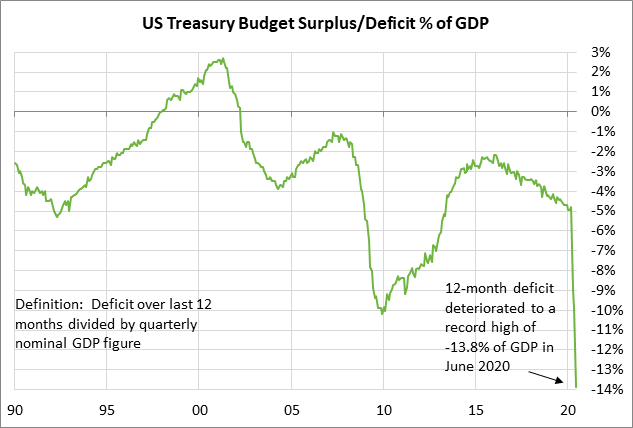

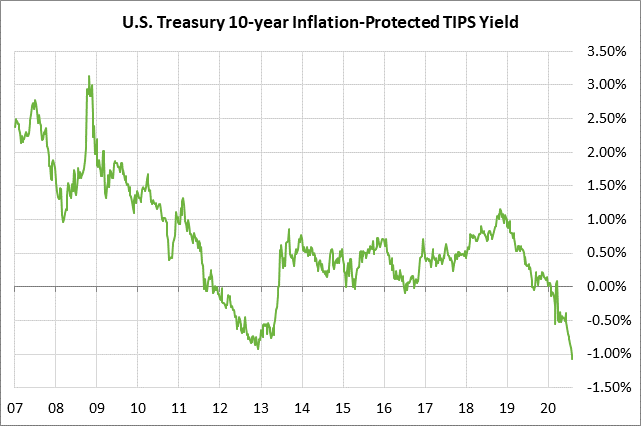

reasury bets the market can handle its deluge of longer-term debt — The Treasury yesterday announced its Q3 auction plans with much larger-than-expected auction sizes for its longer-term debt. A statement said, “Treasury will continue to shift financing from T-bills to longer-dated tenors over the coming quarters, using long-term issuance as a prudent means of managing its maturity profile and limiting potential future issuance volatility.”

The Treasury announced it would issue a record $112 billion in T-notes and T-bonds in next week’s quarterly refunding, higher than the consensus for an increase to $108 billion. The Treasury will increase new and reopened 10-year note auction sizes by $6 billion and increase the new and reopened 30-year bond auction sizes by $4 billion starting in August. The Treasury will also boost the size of its 7-year T-note auctions by $3 billion and increase the new and reopened 20-year T-bond auction sizes by $5 billion starting in August.

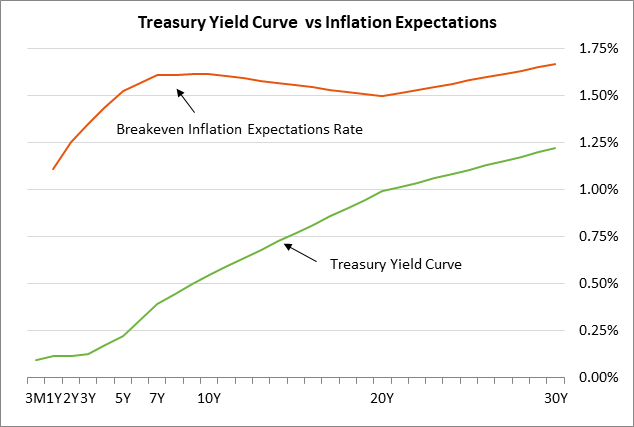

The Treasury’s shift to more financing on the longer end of the yield curve is driven in large part by the sheer cost savings with yields currently near or below 1%, depending on the maturity. Moreover, the Treasury is actually making money on its auctions on an inflation-adjusted basis since real interest rates are currently negative. That means that the Treasury is taking in cash now and paying it back at nominal yields that are below expected inflation rates.

The Treasury clearly believes that the market will be able to easily absorb the increased amount of longer-term debt because of (1) strong safe-haven demand for Treasury securities due to the massive hit to the global economy and financial system from the pandemic, (2) expectations for the Fed to keep its funds-rate target near zero for at least the next two years, (3) the Fed’s $120 billion per month QE program that includes $80 billion per month of Treasury security purchases, and (4) strong demand from foreign investors looking for a positive yield and fleeing from the $15 trillion of negative-yielding global debt.

However, the massive increase in longer-dated Treasury supply could still force yields substantially higher if market conditions should suddenly turn more bearish due to such outside possibilities of (1) a vaccine that enables the U.S. economy to return to normal sooner-than-expected, or (2) an unexpected increase in inflation.

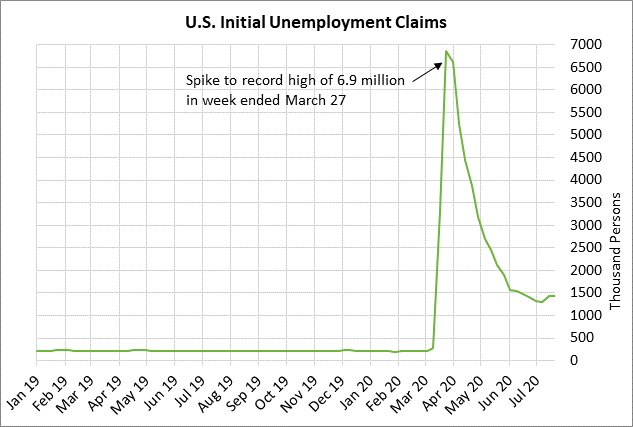

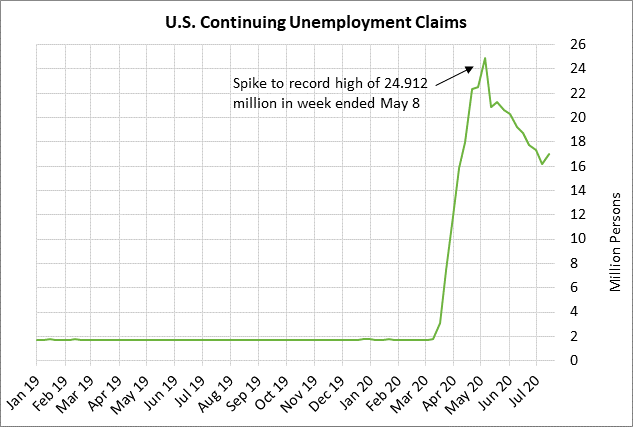

U.S. unemployment claims expected to show some improvement — Today’s initial unemployment claims report is expected to show a modest improvement with a decline of -34,000 after two weeks of rising claims and backsliding in the labor market. Meanwhile, continuing claims are expected to fall -118,000, showing a slightly better labor market after last week’s increase of +867,000. While the labor market has generally improved in the last four months, there are still 15.3 million more people on the unemployment rolls than there were before the pandemic in February.

The consensus is for tomorrow’s July payroll report to show an increase of +1.5 million jobs, adding to June’s +4.8 million job rise. Even the expected rise, however, would leave jobs down by 13.2 million from February’s record high. Yesterday’s ADP report of +167,000 was disappointing and was much weaker than market expectations of +1.2 million. The consensus is for tomorrow’s July unemployment rate to fall by -0.6 points to 10.5%, which would be down from April’s record high of 14.7% but still above the worst level of 10.0% seen during the Great Recession.