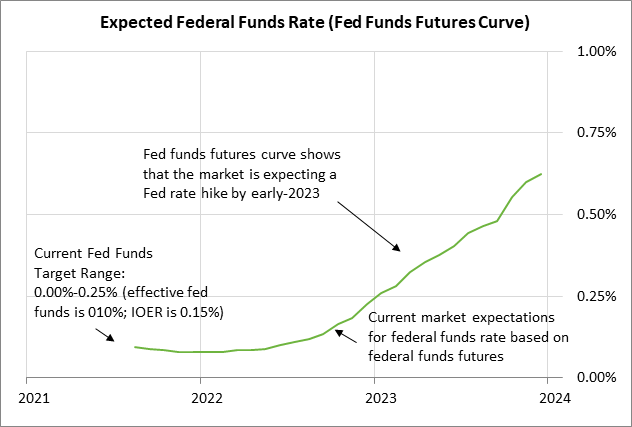

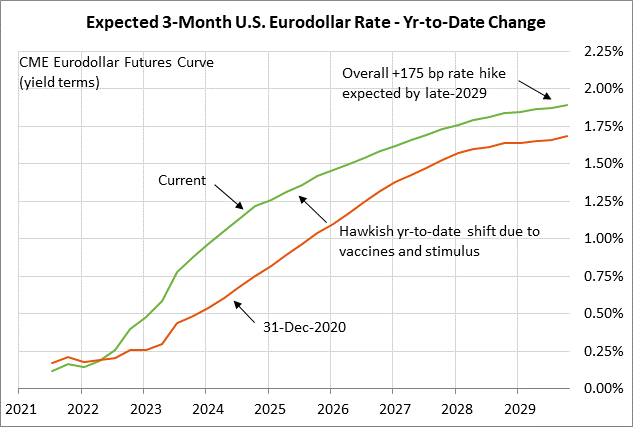

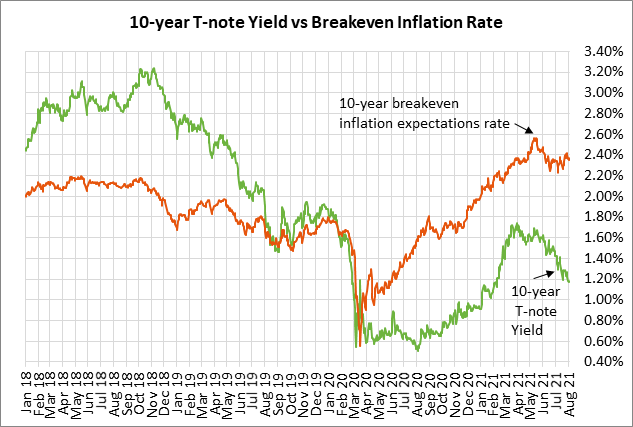

- Clarida supports the market consensus for the timing of QE tapering and first rate hike

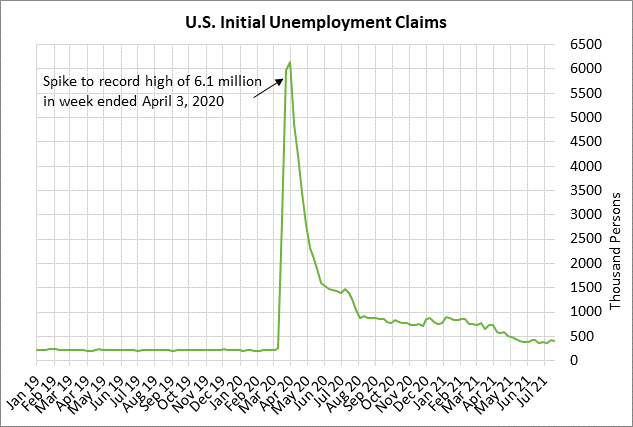

- Unemployment claims expected to show mild improvement

- U.S. trade deficit expected to widen

Clarida supports the market consensus for the timing of QE tapering and first rate hike — Fed Vice Chair Clarida yesterday, at a webinar held by the Peterson Institute for International Economics, made predictions about the timing of QE tapering and the Fed’s first rate hike that were generally in line with the market consensus.

Mr. Clarida said that the “necessary conditions for raising the target range for the federal funds rate will have been met by year-end 2022,” paving the way for the Fed’s first rate hike in 2023. That is in line with the federal funds futures market, which is fully discounting the Fed’s first rate hike in early 2023.

Mr. Clarida noted the risks from the delta variant but said that current policies should continue to support the expansion. He said, “The monetary and fiscal policies presently in place should continue to support the strong expansion in economic activity that is expected to be realized this year, although, obviously, the rapid spread of the Delta variant among the still considerable fraction of the population that is unvaccinated is clearly a downside risk for the outlook.”

However, he said that if the economy stays strong, he would favor the Fed making an announcement later this year for QE tapering. He said, “if my baseline outlook does materialize, I could certainly see supporting announcing a reduction in Fed bond purchases later this year.”

Mr. Clarida’s forecast for a QE announcement “later this year,” although a bit vague, was in line with market expectations. A recent survey by Bloomberg taken on July 16-21 found that 74% of respondents expect the Fed to provide an early warning of QE tapering at its August 26-28 Jackson Hole conference or at the next FOMC meeting on September 21-22.

The survey found that 36% of the respondents expect the Fed to formally announce its QE program somewhere between September and November, while the largest plurality of 47% expect that announcement in December.

Regarding the actual implementation date, a hefty 71% of respondents expect the tapering to begin in Q1-2022. The remaining respondents were roughly split on whether the tapering will be either before or after Q1.

Fed Chair Powell, at his press conference after last week’s FOMC meeting, successfully kept the markets calm even as the Fed took a further step towards QE tapering. Mr. Powell said that the FOMC, at its 2-day meeting that ended last Wednesday, took its “first deep dive” into exactly how QE tapering could be handled.

However, Mr. Powell said, “We’re not there. And we see ourselves as having some ground to cover to get there.” He added, “We’re making progress. We expect further progress and if things go well we will reach that goal.”

Unemployment claims expected to show mild improvement — The consensus is for today’s weekly initial unemployment claims report to show a -17,000 decline to 383,000, adding to last week’s -24,000 decline to 400,000. Today’s continuing claims report is expected to show a -14,000 decline to 3.255 million after last week’s +7,000 increase to 3.269 million.

The improvement in initial claims has stalled in the past several weeks, with initial claims rebounding mildly higher from the 16-month low of 368,000 posted in the last week of June. Initial claims are currently 184,000 above the pre-pandemic level. Continuing claims are still up by 1.6 million from the pre-pandemic level.

The markets are looking ahead to Friday’s unemployment report where July payrolls are expected to increase by +875,000, which would be slightly stronger than June’s increase of +850,000 and the 3-month average of +717,000. Payrolls have risen by +15.6 million from last year’s pandemic trough but still need to rise by another +6.8 million to match the pre-pandemic record high posted in February 2020.

However, yesterday’s ADP report was disappointing and undercut expectations for Friday’s payroll report. ADP jobs rose by only +330,000, which was substantially weaker than expectations of +65,000. The weakness in job growth is due to a bottleneck in hiring efforts, but some businesses might also be delaying their hiring plans as they assess the fallout from the delta variant.

The consensus is for Friday’s July unemployment rate to show a -0.2 point decline to 5.7% after June’s small +0.1 point rise to 5.9%. The expected decline to 5.7% would be a new 16-month low, taking out the current low of 5.8% posted in May.

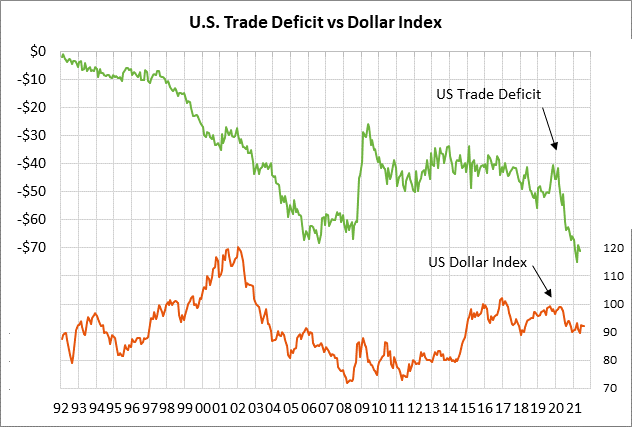

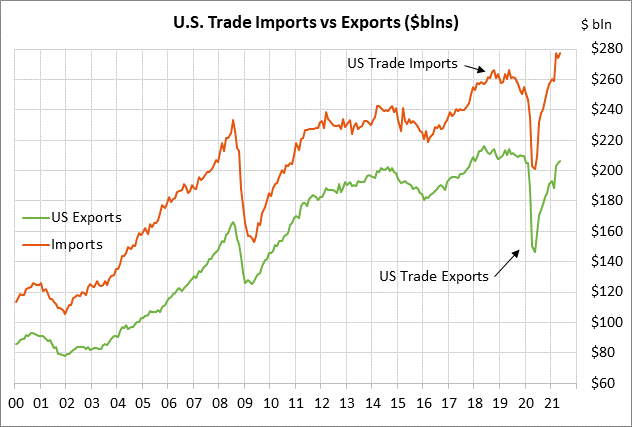

U.S. trade deficit expected to widen — The consensus is for today’s June trade deficit to expand to -$74.1 billion from -$71.2 billion in May. Today’s expected report of -$74.1 billion would be just slightly narrower than the record high of -$75.0 posted in March.

The U.S. trade deficit continues to be extremely wide as the strong U.S. economy pulls in a large amount of imports, while demand for U.S. exports lags due to weaker overseas economic growth. Imports have risen sharply over the past year and have easily posted a new record high, while exports have yet to exceed their pre-pandemic high.

The wide U.S. trade deficit is a negative factor for the U.S. GDP figures. The wide U.S. trade deficit is also a longer-term underlying bearish factor for the dollar as trade dollars flow out of the U.S.