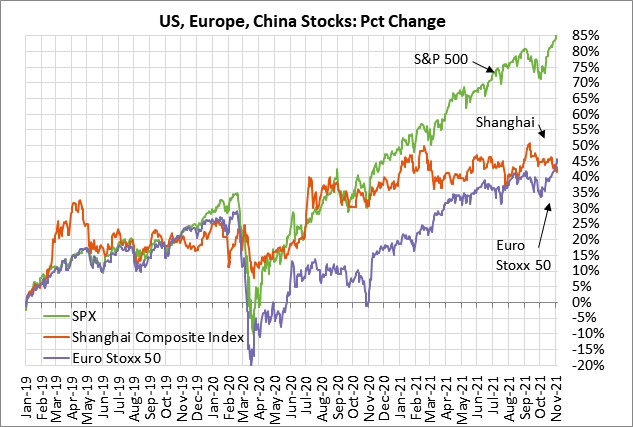

- Weekly market focusÂ

- Fed news and outlook

- House Passes $550 billion infrastructure bill and delays vote on reconciliation bill

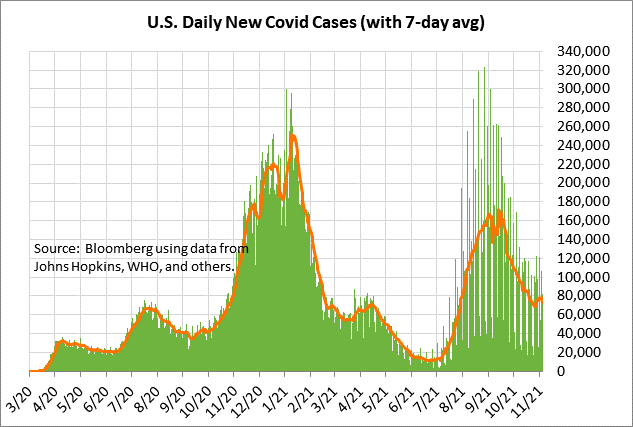

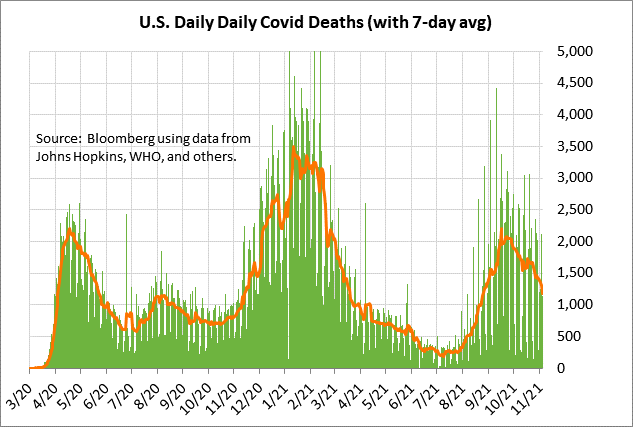

- U.S. Covid infections are down by -56% from September’s high

- Q3 earnings season winds down

- 3-year T-note auction

Weekly market focus — The markets this week will focus on (1) several Fed speakers and their views on the economy and monetary policy, (2) the U.S. producer and consumer price reports for October and whether price pressures are continuing to climb, (3) the winding down of Q3 earnings reporting season with 12 of the S&P 500 companies reporting this week, (4) oil prices and whether President Biden will authorize the release of crude from the Strategic Petroleum Reserve in an attempt to knock prices lower, and (5) the quarterly refunding where the Treasury will sell $120 billion of T-notes and T-bonds.

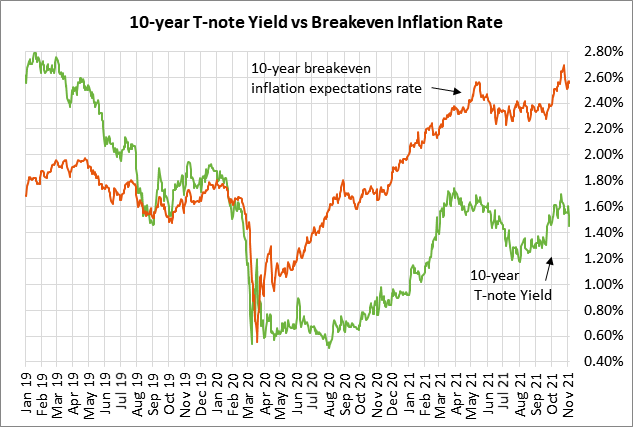

Fed news and outlook — The FOMC as expected last Wednesday announced that it will begin QE tapering this month. The Fed will taper its asset purchases by $15 billion monthly by cutting $10 billion of Treasuries and $5 billion of mortgage-backed securities (MBS). Fed Chair Powell kept a dovish tilt to his post-FOMC comments last Wednesday when he said that the FOMC’s tapering decision “doesn’t imply anything” about raising the federal funds rate, and the Fed “can be patient” when it comes to rate hike timing.

After the BOE last Thursday surprised the markets by not tightening monetary policy, 10-year gilt yields tumbled to a 6-week low and fueled rallies in German bunds and T-notes. Despite last Friday’s stronger-than-expected U.S. Oct nonfarm payrolls report, the market is now pricing in a slower pace of Fed rate hikes. Current pricing anticipates the first 25 bp rate increase in September 2022 and a second by February 2023. Previously, two rate increases were priced in for 2022 with the first hike in July 2022.

House Passes $550 billion infrastructure bill and delays vote on reconciliation bill — The House late Friday night passed the $550 billion infrastructure bill by a vote of 228-206. Democrats, however, were unable to land a House vote on the larger reconciliation bill involving $1.75 trillion of spending and $2 trillion of revenue. The House instead approved a procedural measure that will allow for a vote on the bill the week of November 15 after lawmakers return from a week-long break and the Congressional Budget Office (CBO) delivers a cost analysis of the bill.

Progressive Democrats in the House had effectively blocked the infrastructure bill for months to gain sway over party moderates in the fight over the bigger, Democrats-only reconciliation bill. There was a last-minute concession to a small group of moderates who refused to vote for the reconciliation bill without the CBO score. Progressives also made a concession by supporting the infrastructure legislation before a vote on the larger reconciliation bill.

House Majority Leader Hoyer said he hopes the reconciliation bill could be passed before the November 25 Thanksgiving holiday. However, the vote could be delayed into early December, when Congress must grapple withe a December 3 government funding deadline and raising the debt ceiling. The Senate is all but certain to change the legislation, meaning the House will have to vote again.

U.S. Covid infections are down by -56% from September’s high — U.S. Covid infections have fallen sharply by -56% in the past 7-weeks from mid-September’s peak of 171,850, but are still more than six times higher than June’s temporary trough of 11,299. The 7-day average of new daily U.S. Covid infections on October 26 fell to a 3-1/4 month low of 68,274, but then bounced back up to a 3-week high of 78,398 last Wednesday.

The U.S. has administered a daily average of 1.1 million doses over the past week, according to Bloomberg. That figure has risen in the past several weeks due to booster shots. Bloomberg reports that 58.2% of the total U.S. population has now been fully vaccinated.

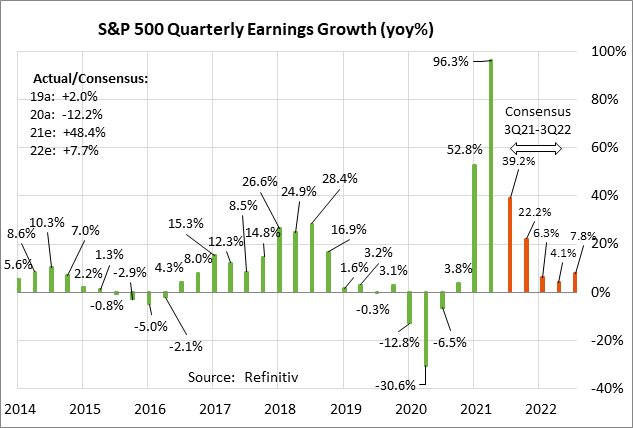

Q3 earnings season winds down — The peak of Q3 earnings season is now past and there are only 12 of the S&P 500 companies reporting. Notable reports include PayPal on Monday; Norwegian Cruise Line on Tuesday; and Disney on Wednesday.

The consensus is for Q3 earnings growth of +39.2% y/y for the S&P 500 companies, according to Refinitiv. Earnings season has been very positive, with 82% of reporting S&P companies having beaten the consensus, higher than the long-term average of 65.8% although below the 4-quarter average of 84.7%, according to Refinitiv. On a calendar year basis, S&P earnings growth in 2021 is expected to be stellar at +48.4%, but is then expected to fade to +7.7% in 2022.

3-year T-note auction — The Treasury today will sell $56 billion of 3-year T-notes to kick off the quarterly refunding operation. The Treasury will then continue this week’s refunding by selling 10-year T-notes on Tuesday and 30-year T-bonds on Wednesday. The benchmark 3-year T-note yield last Friday closed at 0.657%.

The 12-auction averages for the 3-year are as follows: 2.36 bid cover ratio, $38 million in non-competitive bids, 3.3 bp tail to the median yield, 20.3 bp tail to the low yield, and 44% taken at the high yield. The 3-year is least popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of only 50.4% of the last twelve 3-year T-note auctions, which is well below the median of 63.7% for all recent Treasury coupon auctions.