- Weekly market focus

- Fed news and outlook

- Expectations are low for tonight’s U.S./China virtual summit

- Empire manufacturing survey expected to tick higher

- U.S. Covid infections are down by -60% from September’s high

Weekly market focus — The markets this week will focus on (1) this evening’s virtual summit between President Biden and Chinese President Xi Jinping, (2) U.S. Oct retail sales data and if consumer spending held up especially after last Friday’s University of Michigan U.S. Nov consumer sentiment unexpectedly sank to a 10-year low, (3) U.S. Oct manufacturing and industrial production data, (4) oil prices and whether President Biden will authorize the release of crude from the Strategic Petroleum Reserve or halt U.S. crude exports in an attempt to knock prices lower, and (5) several Fed speakers and their views on the economy and monetary policy in the light of U.S. consumer prices in October surging to a three decade high.

Fed news and outlook — The markets will look to Fed speakers this week to see if the recent surge in U.S. consumer prices spurs a more hawkish Fed. If inflation pressures remain sticky, the Fed may be prompted to increase the pace of tapering in order to raise interest rates earlier than anticipated. At the current $15 billion a month pace of tapering, the market expects the Fed to finish tapering by mid-2022. However, an acceleration of price pressures may push the Fed to increase that pace of tapering.

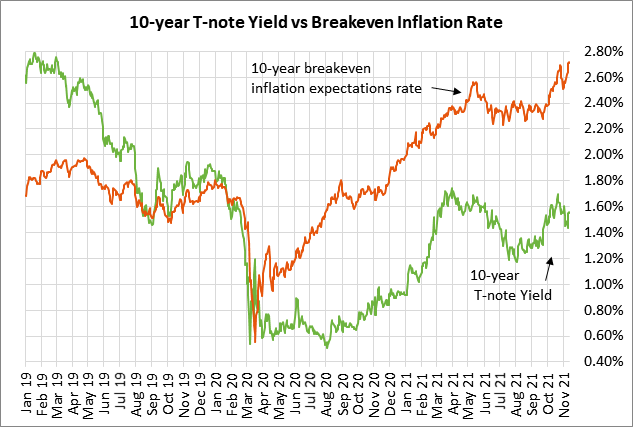

The 10-year breakeven inflation rate jumped to a 16-1/2 year high Friday of 2.76%. It remains to be seen if the increase in inflation expectations will take hold. The University of Michigan’s 1-year inflation expectations rate for November last Friday rose to 4.9%, the highest since 2008, although the 5-10 year inflation projection remained unchanged at 2.9%, just below September’s 10-1/2 year high of 3.0%.

After the stronger-than-expected U.S. CPI data last Wednesday, rate hike expectations were again brought forward. Current pricing anticipates the first 25 bp rate increase in July of 2022 with a second hike priced by the end of next year. Before the U.S. CPI data on Wednesday, the first rate hike was priced in for September 2022 and a second by February 2023.

Expectations are low for tonight’s U.S./China virtual summit — President Biden will meet virtually with Chinese President Xi Jinping this evening. A senior U.S. administration official said the meeting was designed to prevent a misunderstanding that could lead to a military conflict. The two leaders will discuss issues of concern to the U.S., including Taiwan and China’s economic practices, though a discussion about lifting tariffs is not expected and the two sides are not expected to issue a joint statement.

Biden and Xi have spoken on the phone twice this year, but this is the first time the conversation is being billed as a summit. According to a senior U.S. official, the main topic for the talks are the need for both sides to establish guardrails that ensure competition does not become conflict.

Reducing tariffs is one of the top demands China has put forward to the U.S. It may be too optimistic to expect any tariff relief from the summit as the White House has said the meeting is “not about seeking specific deliverables.”

Empire manufacturing survey expected to tick higher — Today’s November Empire manufacturing survey of business conditions is expected to climb by +2.2 points to 22.0. The survey in October tumbled -14.5 points to 19.8 as supply-chain problems curbed manufacturing output in the New York area. The Empire Oct new orders sub-index fell -9.4 points to 24.3 as delivery times in October rose to a record high of 38.0.

The Empire survey is moderately below the record high of 43.0 in July as pandemic restrictions eased and economic activity picked up. The survey had plunged to a record low of -78.2 in April of 2020 during thr height of the pandemic. The Empire survey is a monthly survey with data from 2001 that targets 200 manufacturing executives in the state of New York.

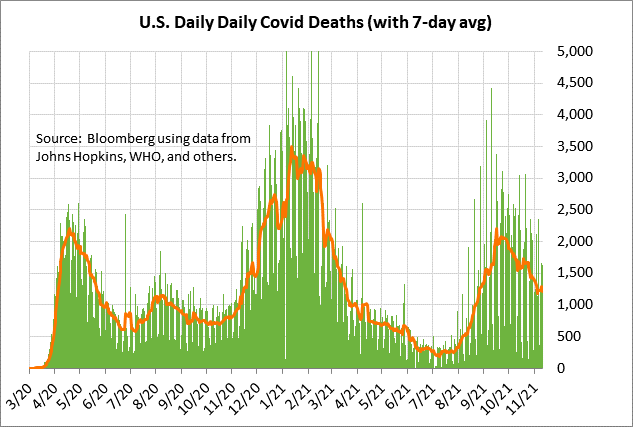

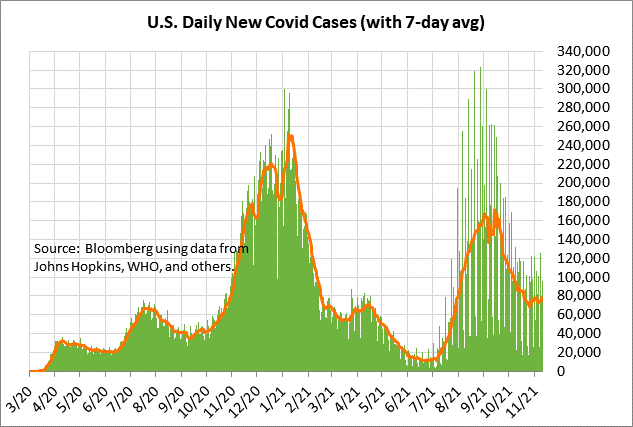

U.S. Covid infections are down by -60% from September’s high — U.S. Covid infections have fallen sharply by -60% in the past 2-months from mid-September’s peak of 171,850, but are still more than six times higher than June’s temporary trough of 11,299. The 7-day average of new daily U.S. Covid infections in late-October fell to a 3-1/2 month low of 68,274, but then bounced back up to a 3-week high of 78,398 on November 4.

The U.S. has administered a daily average of 1.51 million doses over the past week, according to Bloomberg. That figure has risen in the past several weeks due to booster shots. Bloomberg reports that 58.5% of the total U.S. population has now been fully vaccinated.