- Weekly global market focus

- Senate infrastructure legislation to move forward this week

- Q2 earnings season begins this week

- U.S. pandemic statistics surge due to Delta variant

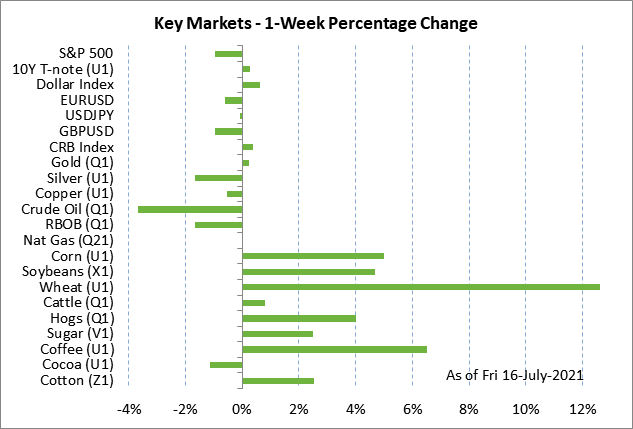

Weekly global market focus — The U.S. markets this week will focus on (1) Q2 earnings season with 87 of the S&P 500 companies reporting, (2) the Treasury’s sale of 20-year T-bonds on Tuesday and 10-year TIPS on Wednesday, (3) oil prices after OPEC+ on Sunday reached an agreement to raise oil production into 2022 after a compromise was reached with the UAE, (4) the recent rise in the U.S. Covid infection rates due to the Delta variant, and (5) this week’s U.S. economy calendar with key reports including Tuesday’s June housing starts report (expected +1.0%), and Thursday’s June existing home sales report (expected +1.7%).

Senate infrastructure legislation to move forward this week — Senate Majority Leader Schumer last week said that he intends to hold a test vote this Wednesday on the bipartisan infrastructure plan.

The Senate is only scheduled to be in session for another three weeks before leaving on August 9 for its summer recess. The Senate will then be on recess until September 13.

Mr. Schumer is pushing hard to get a vote on the bipartisan infrastructure bill and the $3.5 trillion Democratic budget resolution before leaving for the August recess. Senators this Wednesday will be called upon to vote on an infrastructure shelf bill that may not contain all the details of the $579 billion bipartisan infrastructure plan, which will make it even harder to attract the 60 votes necessary to avoid a filibuster.

In addition, the bipartisan plan ran into trouble last Thursday when Senators dropped the idea of spending $40 billion on the IRS to get $100 billion more in revenue. The bipartisan group of Senators now face the difficult problem of trying to replace a $100 billion pay-for.

Mr. Schumer is trying to get the bipartisan group to either put-up or shut-up about their bill and avoid allowing the negotiations to be drawn out any further. If the bipartisan bill cannot get past a Republican filibuster, then Democrats will roll the infrastructure measures into their $3.5 trillion social spending bill.

Meanwhile, the House today will return from its Fourth of July recess. The House passed an infrastructure bill before leaving for its Fourth of July recess, which will be introduced into the Senate early this week as a legislative vehicle for a Senate infrastructure bill.

House Speaker Pelosi has said that the House will not vote on any bipartisan Senate infrastructure bill before the Senate has also passed the $3.5 trillion social spending bill. The House is therefore in a wait-and-see mode as the legislative gears in the Senate grind slowly forward.

The debt ceiling will gain increased attention in the next few weeks since the debt ceiling will be reinstated in two weeks on July 30. The Treasury will then be forced to use emergency procedures to conserve cash. However, the Treasury will eventually run out of cash and will have no legal authority to borrow more money, meaning the Treasury will then hit its “X-Date” when it starts to default on its obligations, possibly including a sovereign default on Treasury security debt.

The Bipartisan Policy Center has warned that it will be particularly difficult to predict the X-date this time around because of “the high uncertainty of Treasury Department cash flows relating to COVID-19 relief disbursements and the pace of the economic recovery.” The BPC is predicting an X-day sometime “this fall,” after the new fiscal year begins on October 1. That means that Congress will likely include a debt ceiling hike with the new fiscal-year spending bill that will be necessary to keep the government open past Oct 1.

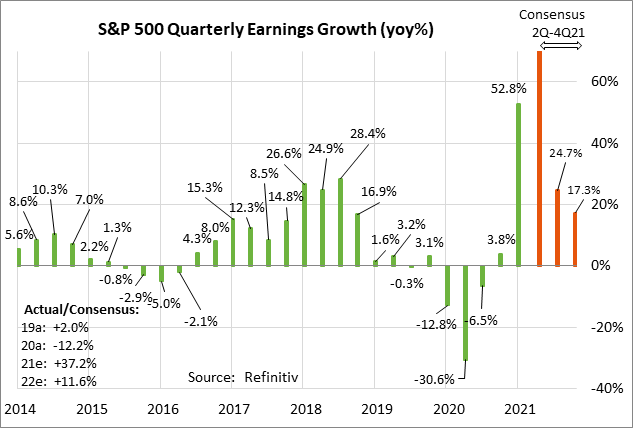

Q2 earnings season begins this week — Q2 earnings season begins in earnest this week with 87 of the S&P 500 companies releasing earnings. Earnings season then kicks into high gear with 184 of the S&P 500 companies reporting next week, and 130 companies reporting during the week of Aug 2-6.

Notable earnings reports this week include IBM today; Netflix and United Airlines on Tuesday; Johnson & Johnson, Coca-Cola, and Verizon on Wednesday; Twitter, Intel, AT&T, American Airlines, and Capital One on Thursday; and American Express and Honeywell on Friday.

The consensus is for Q2 earnings growth of +72.0% y/y for the S&P 500 companies. The year-on-year figure is, of course, inflated by the fact that earnings dropped sharply in Q2-2020 during the height of the pandemic economic shutdowns, causing a very low year-earlier base. For all of 2021, the consensus is for earnings growth of +37.2%, more than recovering from the -12.2% decline seen in 2020.

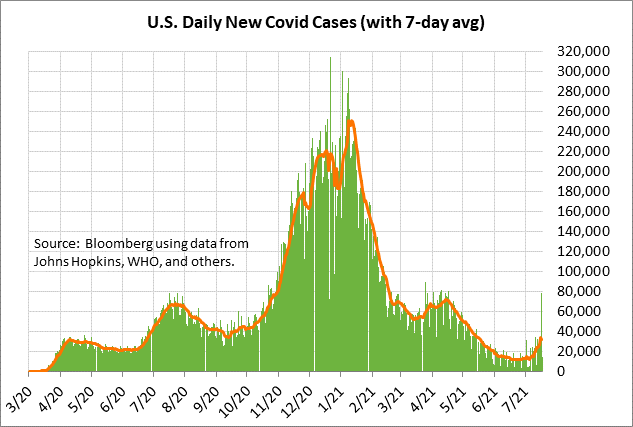

U.S. pandemic statistics surge due to Delta variant — The U.S. Covid infection rate is surging due to the spread of the highly-transmissible Delta variant, which now accounts for more than half of all new U.S. cases. The 7-day average of new U.S. Covid infections on Saturday surged to a 2-month high of 34,190, tripling from the 15-1/2 month low of 11,351 posted only four weeks ago on June 23.

The spread of the Delta variant is taking root due to the slower speed of vaccinations. The CDC reports that 48.6% of the U.S. population is now fully vaccinated and 56.0% of the U.S. population has received at least one dose. Bloomberg reports that the U.S. administered an average of only 512,673 does per day over the last week. Bloomberg estimates that it would take another 9 months to get 75% of the U.S. population vaccinated, which is a measure of herd immunity and a return to normalcy.